Adaptive SMI Ergodic StrategyThe Adaptive SMI Ergodic Strategy aims to capture the momentum and direction of a financial asset by leveraging the Stochastic Momentum Index Indicator (SMI) in an ergodic form. The strategy uses two lengths for the SMI, a shorter and a longer one, and an Exponential Moving Average (EMA) to serve as the signal line. Additionally, the strategy incorporates customizable overbought and oversold thresholds to improve the probability of successful trade execution.

How It Works:

Long Entry: A long position is taken when the ergodic SMI crosses over the EMA signal line, and both the SMI and EMA are below the oversold threshold.

Short Entry: A short position is initiated when the ergodic SMI crosses under the EMA signal line, and both the SMI and EMA are above the overbought threshold.

The strategy plots the SMI in yellow and the EMA signal line in purple. Horizontal lines indicate the overbought and oversold thresholds, and a colored background helps in visually identifying these zones.

Parameters:

Long Length: The length of the long EMA in SMI calculation.

Short Length: The length of the short EMA in SMI calculation.

Signal Line Length: The length for the EMA serving as the signal line.

Oversold: Customizable threshold for the oversold condition.

Overbought: Customizable threshold for the overbought condition.

Historical Context: The SMI Indicator

The Stochastic Momentum Index (SMI) was developed by William Blau in the early 1990s as an enhancement to traditional stochastic oscillators. The SMI provides a range of values like a traditional stochastic, but it differs in that it calculates the distance of the current close relative to the median of the high/low range, as opposed to the close relative to the low. As a result, the SMI is less erratic and more responsive, offering a clearer picture of market trends.

In recent years, the SMI has been adapted into ergodic forms to facilitate smoother data analysis, reduce lag, and improve trading accuracy. The Adaptive SMI Ergodic Strategy leverages these modern enhancements to offer a more robust, customizable trading strategy that aligns with various market conditions.

M-oscillator

Strategy Gaussian Anomaly DerivativeConcept behind this Strategy :

Considering a normal "buy/sell" situation, an asset would be bought in average at the median price following a Gaussian like concept. A higher or lower average trend would significate that the current perceived value is respectively higher or lower than the current median price, which mean that the buyers are evaluating the price underpriced or overpriced.

This behaviour would be even more relevent depending on its derivative evolution.

Therefore, this Strategy setup is based on this Gaussian like concept anomaly of average close positionning compare to high-low average derivative, such as the derivative of the following ploted basic signal : 1-(high+low)/(2*close).

This Strategy can actually be used like a trend change and continuation strength indicator aswell.

In the Setup Signal part :

You can define the filtering of the basis signal "1-(high+low)/(2*close)" on EMA or SMA as you wish.

You can define the corresponding period and the threathold as a mutiply of the average 1/3 of all time value of the basis signal.

You can define the SMA filtering period of the Derivative signal and the corresponding threathold on the same mutiply of the average 1/3 of all time value of the derivative.

In the Setup Strategy part :

You can set up your strategy assesment based on Long and/or Short. You can also define the considered period.

The most successful tuned strategies I did were based on the derivative indicator with periods on the basis signal and the derivative under 30, can be 1 to 3 of te derivative and 7 to 21 for the basis signal. The threathold depends on the asset volatility aswell, 1 is usually the most efficient but 0 to 10 can be relevent depending on the situation I met. You can find an example of tuning for this strategy based on Kering's case hereafter.

I hoping that you will enjoy using this Strategy, don't hesitate to comment, to question, to correct or complete it ! I would be very curious about similar famous approaches that would have already been made.

Thank to you !

Golden Transform The Golden Transform Oscillator contains multiple technical indicators and conditions for making buy and sell decisions. Here's a breakdown of its components and what it's trying to achieve:

Strategy Setup:

The GT is designed to be plotted on the chart without overlaying other indicators.

Rate of Change (ROC) Calculation:

The Rate of Change (ROC) indicator is calculated with a specified period ("Rate of Change Length").

The ROC measures the percentage change in price over the specified period.

Hull Modified TRIX Calculation:

The Hull Modified TRIX indicator is calculated with a specified period ("Hull TRIX Length").

The Hull MA (Moving Average) formula, a modified WMA, is used to calculate a modified TRIX indicator, which is a momentum oscillator.

Hull MA Calculation:

A Hull Moving Average (Hull MA) is calculated as an entry filter.

Fisher Transform Calculation:

The Fisher Transform indicator is calculated to serve as a preemptive exit filter.

It involves mathematical transformations of price data to create an oscillator that can help identify potential reversals. The Fisher Transform is further smoothed using a Hull Moving Average (HMA).

Conditions and Signals:

Long conditions are determined based on crossovers between ROC and TRIX, as well as price relative the the MA. Short conditions are inversed.

Exit Conditions:

Exit conditions are defined for both long and short positions.

For long positions, the strategy exits if ROC crosses under TRIX, or if the smoothed Fisher Transform crosses above a threshold and declines. Once again, short conditions are the inverse.

Visualization and Plotting:

The script uses background colors for entry and shapes for exits to highlight different levels and conditions for the ROC/TRIX correlation.

It plots the Fisher Transform values and a lag trigger on the chart.

Overall, this script is a complex algorithm that combines multiple technical indicators and conditions to generate trading signals and manage positions in the financial markets. It aims to identify potential entry and exit points based on the interplay of the mentioned indicators and conditions.

Gaussian Detrended ReversionThis strategy, titled "Gaussian Detrended Reversion Strategy," aims to identify potential price reversals using the customized Gaussian Detrended Price Oscillator (GDPO) in combination with smoothed price cycles.

Key Elements of the Strategy:

GDPO Calculation: The strategy first calculates the Detrended Price Oscillator (DPO) by comparing the close price to an Exponential Moving Average (EMA) of a specified period. This calculation helps identify short-term price cycles by detrending the price data.

Gaussian Smoothing: The DPO values are then smoothed using the Arnaud Legoux Moving Average (ALMA), applying a Gaussian smoothing technique. This smoothed version of the DPO is intended to filter out noise and provide a clearer picture of price trends.

Entry and Exit Conditions: The strategy defines conditions for both long and short entry points as well as exit points. It looks for specific crossover events between the smoothed GDPO and its lagged version. The strategy enters a long position when the smoothed GDPO crosses above the lag and is negative, and exits the long position when the smoothed GDPO crosses below the lag or the zero line. Similarly, the strategy enters a short position when the smoothed GDPO crosses below the lag and is positive, and exits the short position when the smoothed GDPO crosses above the lag or the zero line.

Visualization: The smoothed GDPO and its lag are plotted on the chart using distinct colors. The zero line is also displayed as a reference point. Additionally, the chart background changes color when the strategy enters a long or short position. Cross markers are also plotted at the crossover points as exit cues.

Overall, this strategy aims to capture potential price reversals using the GDPO and Gaussian smoothing, with specific entry and exit conditions to guide trading decisions.

TRAX Detrended Price StrategyIn this script, the "TRAX" (TRIX) indicator is calculated using the Volume Weighted Moving Average (VWMA) instead of Exponential Moving Average (EMA) like the standard TRIX. The Detrended Price is used to identify short term cycles with a rate of change verses the rate of change from a triple smoothed TRAX VWMA . The strategy is intended for counter-trend trading, meaning it tries to capture potential reversals.

1. Indicators Used:

TRAX is calculated using the Volume Weighted Moving Average (VWMA) of the logarithm of the closing price.

DPO (Detrended Price Oscillator) is calculated by taking the closing price and subtracting a simple moving average (SMA) of the closing price shifted back.

2. Crossover Conditions:

Longs occur when DPO crosses above the TRAX, with the TRAX trending below 0, and the stock is trading above an adjustable simple moving average. Shorts occur due to the inverse conditions.

3. Visualization:

This script plots the SMA and the TRAX-DPO Combined Oscillator.

It highlights the periods of zero-line crossover using a green background for potential long positions and a red background for potential short positions. However, it will trigger verified entries/exits in accordance with the SMA.

In conclusion, this fun prototype underwent a unique alteration using the Volume Weighted Moving Average and focuses on capturing shorter counter-trend cycles. You have the freedom to fine-tune the strategy by adjusting parameters and incorporating other analysis methods that resonate with your trading style and risk tolerance.

3-Signal Directional Trend Strategy for E-MinisThis is a conceptual strategy intended for E-mini S&P 500 futures with hourly bars.

It uses three signals, going long or short when two or more change in the same direction.

First is MACD. A positive oscillator is considered a bullish signal and a falling oscillator is interpreted bearishly.

Next, stochastics are used as an overbought/oversold indicator. Overbought conditions are considered bearish and oversold readings are viewed as bullish.

Third is a custom indicator based on our Moving Average Speed script. It takes the rate of change of the 50-hour simple moving average (SMA), and then smooths it using a 10-period average. This provides a directional signal.

Traders may want to experiment with different settings for moving average speed.

Note: This is intended for use with stock index futures, which have round-the clock price data to populate the data in the indicators. It may not yield good results with stocks or ETFs.

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options, futures and cryptocurrencies. See our Overview for more.

Important Information

TradeStation Securities, Inc., TradeStation Crypto, Inc., and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., all operating, and providing products and services, under the TradeStation brand and trademark. TradeStation Crypto, Inc. offers to self-directed investors and traders cryptocurrency brokerage services. It is neither licensed with the SEC or the CFTC nor is it a Member of NFA. When applying for, or purchasing, accounts, subscriptions, products, and services, it is important that you know which company you will be dealing with. Please click here for further important information explaining what this means.

This content is for informational and educational purposes only. This is not a recommendation regarding any investment or investment strategy. Any opinions expressed herein are those of the author and do not represent the views or opinions of TradeStation or any of its affiliates.

Investing involves risks. Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options, futures, or digital assets); therefore, you should not invest or risk money that you cannot afford to lose. Before trading any asset class, first read the relevant risk disclosure statements on the Important Documents page, found here: www.tradestation.com .

Heikin Ashi ROC Percentile Strategy**User Guide for the "Heikin Ashi ROC Percentile Strategy"**

This strategy, "Heikin Ashi ROC Percentile Strategy", is designed to provide an easy-to-use framework for trading based on the Heikin Ashi Rate of Change (ROC) and its percentiles.

Here's how you can use it:

1. **Setting the Start Date**: You can set the start date for the strategy in the user inputs at the top of the script. The variable `startDate` defines the point from which the script begins executing trades. Simply input the desired date in the format "YYYY MM DD". For example, to start the strategy from March 3, 2023, you would enter `startDate = timestamp("2023 03 03")`.

2. **Adjusting the Midline, Lookback Period, and Stop Loss Level**: The `zerohLine`, `rocLength`, and `stopLossLevel` inputs allow you to adjust the baseline for ROC, the lookback period for the SMA and ROC, and the level at which the strategy stops the loss, respectively. By tweaking these parameters, you can fine-tune the strategy to better suit your trading style or the particular characteristics of the asset you are trading.

3. **Understanding the Trade Conditions**: The script defines conditions for entering and exiting long and short positions based on crossovers and crossunders of the ROC and the upper and lower "kill lines". These lines are defined as certain percentiles of the ROC's highest and lowest values over a specified lookback period. When the ROC crosses above the lower kill line, the script enters a long position; when it crosses below the upper kill line, it exits the position. Similarly, when the ROC crosses below the upper kill line, the script enters a short position; when it crosses above the lower kill line, it exits the position.

In my testing, this strategy performed best on a day and hour basis. However, I encourage you to experiment with different timeframes and settings to see how the strategy performs under various conditions. Remember, there's no one-size-fits-all approach to trading; what works best will depend on your specific circumstances, goals, and risk tolerance.

If you find other useful applications for this strategy, please let me know in the comments. Your feedback is invaluable in helping to refine and improve this tool. Happy trading!

D-BoT Alpha 'Short' SMA and RSI StrategyDostlar selamlar,

İşte son derece basit ama etkili ve hızlı, HTF de çok iyi sonuçlar veren bir strateji daha, hepinize bol kazançlar dilerim ...

Nedir, Nasıl Çalışır:

Strateji, iki ana girdiye dayanır: SMA ve RSI. SMA hesaplama aralığı 200 olarak, RSI ise 14 olarak ayarlanmıştır. Bu değerler, kullanıcı tercihlerine veya geriye dönük test sonuçlarına göre ayarlanabilir.

Strateji, iki koşul karşılandığında bir short sinyali oluşturur: RSI değeri, belirlenen bir giriş seviyesini (burada 51 olarak belirlenmiş) aşar ve kapanış fiyatı SMA değerinin altındadır.

Strateji, kısa pozisyonu üç durumda kapatır: Kapanış fiyatı, takip eden durdurma seviyesinden (pozisyon açıldığından beri en düşük kapanış olarak belirlenmiştir) büyükse, RSI değeri belirlenen bir durdurma seviyesini (bu durumda 54) aşarsa veya RSI değeri belirli bir kar al seviyesinin (bu durumda 32) altına düşerse.

Güçlü Yönleri:

İki farklı gösterge (SMA ve RSI) kullanımı, yalnızca birini kullanmaktan daha sağlam bir sinyal sağlayabilir.

Strateji, karları korumaya ve fiyat dalgalanmalarında kayıpları sınırlamaya yardımcı olabilecek bir iz süren durdurma seviyesi içerir.

Script oldukça anlaşılır ve değiştirmesi nispeten kolaydır.

Zayıf Yönleri:

Strateji, hacim, oynaklık veya daha geniş piyasa eğilimleri gibi diğer potansiyel önemli faktörleri göz önünde bulundurmaz.

RSI seviyeleri ve SMA süresi için belirli parametreler sabittir ve tüm piyasa koşulları veya zaman aralıkları için optimal olmayabilir.

Strateji oldukça basittir. Trade maliyetini (kayma veya komisyonlar gibi) hesaba katmaz, bu da trade performansını önemli ölçüde etkileyebilir.

Bu Stratejiyle Nasıl İşlem Yapılır:

Strateji, short işlemler için tasarlanmıştır. RSI, 51'in üzerine çıktığında ve kapanış fiyatı 200 periyotluk SMA'nın altında olduğunda işleme girer. RSI, 54'ün üzerine çıktığında veya 32'nin altına düştüğünde veya fiyat, pozisyon açıldığından beri en düşük kapanış fiyatının üzerine çıktığında işlemi kapatır.

Lütfen Dikkat, bu strateji veya herhangi bir strateji izole bir şekilde kullanılmamalıdır. Tüm bu çalışmalar eğitsel amaçlıdır. Yatırım tavsiyesi içermez.

This script defines a trading strategy based on Simple Moving Average (SMA) and the Relative Strength Index (RSI) indicators. Here's an overview of how it works, along with its strengths and weaknesses, and how to trade using this strategy:

How it works:

The strategy involves two key inputs: SMA and RSI. The SMA length is set to 200, and the RSI length is set to 14. These values can be adjusted based on user preferences or back-testing results.

The strategy generates a short signal when two conditions are met: The RSI value crosses over a defined entry level (set at 51 here), and the closing price is below the SMA value.

When a short signal is generated, the strategy opens a short position.

The strategy closes the short position under three conditions: If the close price is greater than the trailing stop (which is set as the lowest close since the position opened), if the RSI value exceeds a defined stop level (54 in this case), or if the RSI value drops below a certain take-profit level (32 in this case).

Strengths:

The use of two different indicators (SMA and RSI) can provide a more robust signal than using just one.

The strategy includes a trailing stop, which can help to protect profits and limit losses as the price fluctuates.

The script is straightforward and relatively easy to understand and modify.

Weaknesses:

The strategy doesn't consider other potentially important factors, such as volume, volatility, or broader market trends.

The specific parameters for the RSI levels and SMA length are hard-coded, and may not be optimal for all market conditions or timeframes.

The strategy is very simplistic. It doesn't take into account the cost of trading (like slippage or commissions), which can significantly impact trading performance.

How to trade with this strategy:

The strategy is designed for short trades. It enters a trade when the RSI crosses above 51 and the closing price is below the 200-period SMA. It will exit the trade when the RSI goes above 54 or falls below 32, or when the price rises above the lowest closing price since the position was opened.

Please note, this strategy or any strategy should not be used in isolation. It's important to consider other aspects of trading such as risk management, capital allocation, and combining different strategies to diversify. Back-testing the strategy on historical data and demo trading before going live is also a recommended practice.

D-Bot Alpha RSI Breakout StrategyHello dear Traders,

Here is a simple yet effective strategy to use, for best profit higher time frame, such as daily.

Structure of the code

The code defines inputs for SMA (simple moving average) length, RSI (relative strength index) length, RSI entry level, RSI stop loss level, and RSI take profit level. The default values of these variables can be customized as per the user's preferences.

The script calculates SMA and RSI based on the input parameters and the closing price of the asset.

Trading logic

This strategy allows the placement of a long position when:

The RSI crosses above the RSI entry level and

The close price is above the SMA value.

After entering a long position, it applies a trailing stop mechanism. The stop price is updated to the close price if the close price is lower than the last close price.

The script closes the long position when:

RSI falls below the stop loss level.

RSI reaches or exceeds the take profit level.

If the trailing stop is activated (once RSI reaches or exceeds the take profit level), the closing price falls below the trailing stop level.

Strengths

The strategy includes mechanisms for entering a position, taking profit, and stopping losses, which are fundamental aspects of a trading strategy.

It applies a trailing stop mechanism that allows to capture further gains if the price keeps increasing while protecting from losses if the price starts to decrease.

Weaknesses

This strategy only contemplates long positions. Depending on the market situation, the strategy may miss opportunities for short selling when the market is on a downward trend.

The choice of the fixed RSI entry, stop loss, and take profit levels may not be ideal for all market conditions or assets. It might benefit from a more adaptive mechanism that adjusts these levels according to market volatility or trend.

The strategy doesn't factor in trading costs (such as spread or commission), which could have a significant impact on the net profit, especially if the user is trading with a high frequency or in a low liquidity market.

How to trade with this strategy

Given these parameters and the strategy outlined by the code, the trader would enter a long position when the RSI crosses above the RSI entry level (default 34) and the closing price is above the SMA value (SMA calculated with default period of 200). The trader would exit the position when either the RSI falls below the RSI stop loss level (default 30), or RSI rises above the RSI take profit level (default 50), or when the trailing stop is hit.

Remember "The strategies I have prepared are entirely for educational purposes and should not be considered as investment advice. Support your trades using other tools. Wishing everyone profitable trades..."

Ultimate Balance StrategyThe Ultimate Balance Oscillator Strategy harnesses the power of the Ultimate Balance Oscillator to deliver a comprehensive and disciplined approach to trading. By combining the insights of the Rate of Change (ROC), Relative Strength Index (RSI), Commodity Channel Index (CCI), Williams Percent Range, and Average Directional Index (ADX) from TradingView, this strategy offers traders a systematic way to navigate the markets with precision.

The core principle of this strategy lies in its ability to identify optimal entry and exit points based on the movement of the Ultimate Balance Oscillator. When the oscillator line crosses below the 0.75 level, a buy signal is generated, indicating a potential opportunity for a bullish trend reversal. Conversely, when the oscillator line crosses above the 0.25 level, it triggers an exit signal, suggesting a possible end to a bullish trend.

Key Features:

1. Objective Market Analysis: The Ultimate Balance Oscillator Strategy provides a disciplined and objective approach to market analysis. By relying on the quantified insights of multiple indicators, it helps traders cut through market noise and focus on key signals, improving decision-making and reducing emotional biases.

2. Enhanced Timing and Precision: This strategy's entry and exit signals are based on the specific thresholds of the Ultimate Balance Oscillator. By waiting for confirmation through the crossing of these levels, traders can potentially enter trades at opportune moments and exit with greater precision, maximizing profit potential and minimizing risk exposure.

3. Customizability and Adaptability: The strategy offers flexibility, allowing traders to customize the parameters to fit their preferred trading style and timeframes. Whether you're a short-term trader or a long-term investor, the Ultimate Balance Oscillator Strategy can be adjusted to suit your specific needs, making it adaptable to various market conditions.

4. Real-time Alerts: Stay informed and never miss a potential trade opportunity with the strategy's built-in alert system. Set personalized alerts for buy and exit signals to receive timely notifications, ensuring you're always aware of the latest developments in the market.

5. Backtesting and Optimization: Before applying the strategy to live trading, it's recommended to conduct thorough backtesting and optimization. By testing the strategy's performance over historical data and fine-tuning the parameters, you can gain insights into its strengths and weaknesses, enabling you to make informed adjustments and increase its effectiveness.

Trading involves risk. Use the Ultimate Balance Oscillator Strategy at your own discretion. Past performance is not indicative of future results.

Williams %R Strategy

The Williams %R Strategy is a trading approach that is based on the Williams Percent Range indicator, available on the TradingView platform.

This strategy aims to identify potential overbought and oversold conditions in the market, providing clear buy and sell signals for entry and exit.

The strategy utilizes the Williams %R indicator, which measures the momentum of the market by comparing the current close price with the highest high and lowest low over a specified period. When the Williams %R crosses above the oversold level, a buy signal is generated, indicating a potential upward price movement. Conversely, when the indicator crosses below the overbought level, a sell signal is generated, suggesting a possible downward price movement.

Position management is straightforward with this strategy. Upon receiving a buy signal, a long position is initiated, and the position is closed when a sell signal is generated. This strategy allows traders to capture potential price reversals and take advantage of short-term market movements.

To manage risk, it is recommended to adjust the position size based on the available capital. In this strategy, the position size is set to 10% of the initial capital, ensuring proper risk allocation and capital preservation.

It is important to note that the Williams %R Strategy should be used in conjunction with other technical analysis tools and risk management techniques. Backtesting and paper trading can help evaluate the strategy's performance and fine-tune the parameters before deploying it with real funds.

Remember, trading involves risks, and past performance is not indicative of future results. It is always advised to do thorough research, seek professional advice, and carefully consider your financial goals and risk tolerance before making any investment decisions.

HK Percentile Interpolation One

This script is designed to execute a trading strategy based on Heikin Ashi candlesticks, moving averages, and percentile levels.

Please note that you should keep your original chart in normal candlestick mode and not switch it to Heikin Ashi mode. The script itself calculates Heikin Ashi values from regular candlesticks. If your chart is already in Heikin Ashi mode, the script would be calculating Heikin Ashi values based on Heikin Ashi values, which would produce incorrect results.

The strategy begins trading from a start date that you can specify by modifying the `startDate` parameter. The format of the date is "YYYY MM DD". So, for example, to start the strategy from January 1, 2022, you would set `startDate = timestamp("2022 01 01")`.

The script uses Heikin Ashi candlesticks, which are plotted in the chart. This approach can be useful for spotting trends and reversals more easily than with regular candlestick charts. This is particularly useful when backtesting in TradingView's "Rewind" mode, as you can see how the Heikin Ashi candles behaved at each step of the strategy.

Buy and sell signals are generated based on two factors:

1. The crossing over or under of the Heikin Ashi close price and the 75th percentile price level.

2. The Heikin Ashi close price being above certain moving averages.

You have the flexibility to adjust several parameters in the script, including:

1. The stop loss and trailing stop percentages (`stopLossPercentage` and `trailStopPercentage`). These parameters allow the strategy to exit trades if the price moves against you by a certain percentage.

2. The lookback period (`lookback`) used to calculate percentile levels. This determines the range of past bars used in the percentile calculation.

3. The lengths of the two moving averages (`yellowLine_length` and `purplLine_length`). These determine how sensitive the moving averages are to recent price changes.

4. The minimum holding period (`holdPeriod`). This sets the minimum number of bars that a trade must be kept open before it can be closed.

Please adjust these parameters according to your trading preferences and risk tolerance. Happy trading!

Stochastic RSI Strategy (with SMA and VWAP Filters)The strategy is designed to trade on the Stochastic RSI indicator crossover signals.

Below are all of the trading conditions:

-When the Stochastic RSI crosses above 30, a long position is entered.

-When the Stochastic RSI crosses below 70, a short position is entered.

-The strategy also includes two additional conditions for entry:

-Long entries must have a positive spread value between the 9 period simple moving average and the 21 period simple moving average.

-Short entries must have a negative spread value between the 9 period simple moving average and the 21 period simple moving average.

-Long entries must also be below the volume-weighted average price.

-Short entries must also be above the volume-weighted average price.

-The strategy includes stop loss and take profit orders for risk management:

-A stop loss of 20 ticks is placed for both long and short trades.

-A take profit of 25 ticks is placed for both long and short trades.

The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)

Are you tired of manually analyzing charts and trying to find profitable trading opportunities? Look no further! Our algorithmic trading strategy, "Flash," is here to simplify your trading process and maximize your profits.

Flash is an advanced trading algorithm that combines three powerful indicators to generate highly selective and accurate trading signals. The Momentum-RSI, Super-Trend Analysis and EMA-Strategy indicators are used to identify the strength and direction of the underlying trend.

The Momentum-RSI signals the strength of the trend and only generates trading signals in confirmed upward or downward trends. The Super-Trend Analysis confirms the trend direction and generates signals when the price breaks through the super-trend line. The EMA-Strategy is used as a qualifier for the generation of trading signals, where buy signals are generated when the EMA crosses relevant trend lines.

Flash is highly selective, as it only generates trading signals when all three indicators align. This ensures that only the highest probability trades are taken, resulting in maximum profits.

Our trading strategy also comes with two profit management options. Option 1 uses the so-called supertrend-indicator which uses the dynamic ATR as a key input, while option 2 applies pre-defined, fixed SL and TP levels.

The settings for each indicator can be customized, allowing you to adjust the length, limit value, factor, and source value to suit your preferences. You can also set the time period in which you want to run the backtest and how many dollar trades you want to open in each position for fully automated trading.

Choose your preferred trade direction and stop-loss/take-profit settings, and let Flash do the rest. Say goodbye to manual chart analysis and hello to consistent profits with Flash. Try it now!

General Comments

This Flash Strategy has been developed in cooperation between Baby_whale_to_moon and JS-TechTrading. Cudos to Baby_whale_to_moon for doing a great job in transforming sophisticated trading ideas into pine scripts.

Detailed Description

The “Flash” script considers the following indicators for the generation of trading signals:

1. Momentum-RSI

2. ‘Super-Trend’-Analysis

3. EMA-Strategy

1. Momentum-RSI

• This indicator signals the strength of the underlying upward- or downward-trend.

• The signal range of this indicator is from 0 to 100. Values > 60 indicate a confirmed upward- or downward-trend.

• The strategy will only generate trading signals in case the stock (or any other financial security) is in a confirmed upward- (long entry signals) or downward-trend (short entry signals).

• This indicator provides information with regards to the strength of the underlying trend and it does not give any insight with regard to the direction of the trend. Therefore, this strategy also considers other indicators which provide technical confirmation with regards to the direction of the underlying trend.

Graph 1 shows this concept:

• The Momentum-RSI indicator gives lower readings during consolidation phases and no trading signals are generated during these periods.

Example (graph 2):

2. Super-Trend Analysis

• The red line in the graph below represents the so-called super-trend-line. Trading signals are only generated in case the price action breaks through this super-trend-line indicating a new confirmed upward-trend (or downward-trend, respectively).

• If that happens, the super trend-line changes its color from red to green, giving confirmation that the trend changed from bearish to bullish and long-entries can be considered.

• The vice-versa approach can be considered for short entries.

Graph 3 explains this concept:

3. Exponential Moving Average / EMA-Strategy

The functionality of this EMA-element of the strategy has been programmed as follows:

• The exponential moving average and two other trend lines are being used as qualifiers for the generation of trading-signals.

• Buy-signals for long-entries are only considered in case the EMA (yellow line in the graph below) crosses the red line.

• Sell-signals for short-entries are only considered in case the EMA (yellow line in the graph below) crosses the green line.

An example is shown in graph 4 below:

We use this indicator to determine the new trend direction that may occur by using the data of the price's past movement.

4. Bringing it all together

This section describes in detail, how this strategy combines the Momentum-RSI, the super-trend analysis and the EMA-strategy.

The strategy only generates trading-signals in case all of the following conditions and qualifiers are being met:

1. Momentum-RSI is higher than the set value of this strategy. The standard and recommended value is 60 (graph 5):

2. The super-trend analysis needs to indicate a confirmed upward-trend (for long-entry signals) or a confirmed downward-trend (for short-entry signals), respectively.

3. The EMA-strategy needs to indicate that the stock or financial security is in a confirmed upward-trend (long-entries) or downward-trend (short-entries), respectively.

The strategy will only generate trading signals if all three qualifiers are being met. This makes this strategy highly selective and is the key secret for its success.

Example for Long-Entry (graph 6):

When these conditions are met, our Long position is opened.

Example for Short-Entry (graph 7):

Trade Management Options (graph 8)

Option 1

In this dynamic version, the so-called supertrend-indicator is being used for the trade exit management. This supertrend-indicator is a sophisticated and optimized methodology which uses the dynamic ATR as one of its key input parameters.

The following settings of the supertrend-indicator can be changed and optimized (graph 9):

The dynamic SL/TP-lines of the supertrend-indicator are shown in the charts. The ATR-length and the supertrend-factor result in a multiplier value which can be used to fine-tune and optimize this strategy based on the financial security, timeframe and overall market environment.

Option 2 (graph 10):

Option 2 applies pre-defined, fixed SL and TP levels which will appear as straight horizontal lines in the chart.

Settings options (graph 11):

The following settings can be changed for the three elements of this strategy:

1. (Length Mom-Rsi): Length of our Mom-RSI indicator.

2. Mom-RSI Limit Val: the higher this number, the more momentum of the underlying trend is required before the strategy will start creating trading signals.

3. The length and factor values of the super trend indicator can be adjusted:ATR Length SuperTrend and Factor Super Trend

4. You can set the source value used by the ema trend indicator to determine the ema line: Source Ema Ind

5. You can set the EMA length and the percentage value to follow the price: Length Ema Ind and Percent Ema Ind

6. The backtesting period can be adjusted: Start and End time of BackTest

7. Dollar cost per position: this is relevant for 100% fully automated trading.

8. Trade direction can be adjusted: LONG, SHORT or BOTH

9. As we explained above, we can determine our stop-loss and take-profit levels dynamically or statically. (Version 1 or Version 2 )

Display options on the charts graph 12):

1. Show horizontal lines for the Stop-Loss and Take-profit levels on the charts.

2. Display relevant Trend Lines, including color setting options for the supertrend functionality. In the example below, green lines indicate a confirmed uptrend, red lines indicate a confirmed downtrend.

Other comments

• This indicator has been optimized to be applied for 1 hour-charts. However, the underlying principles of this strategy are supply and demand in the financial markets and the strategy can be applied to all timeframes. Daytraders can use the 1min- or 5min charts, swing-traders can use the daily charts.

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The combination of the qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

Fair Value Strategy - ekmllThis is a strategy using SPX's Fair Value derived from Net Liquidity.

The main difference between this one and calebsandfort's one is net liquidity values in this one are calculated in TradingView and doesn't need author's daily library updates to function.

Net Liquidity function is simply: Fed Balance Sheet - Treasury General Account - Reverse Repo Balance

Formula for calculating the fair value of and Index using Net Liquidity looks like this: (WALCL - WTREGEN - RRPONTSYD)/1000000000/scalar - subtractor

The Index Fair Value is then subtracted from the Index value which creates an oscillating diff value.

When diff is greater than the overbought threshold, Index is considered overbought and we go short/sell.

When diff is less than the oversold signal, Index is considered oversold and we cover/buy.

Parameters:

Index: SPX, NDX, RUT

Strategy: Short Only, Long Only, Long/Short

Inverse (bool): check if using an inverse ETF to go long instead of short.

Scalar (float)

Subtractor (int)

Overbought Threshold (int)

Oversold Threshold (int)

Start After Date: When the strategy should start trading

Close Date: Day to close open trades. I just like it to get complete results rather than the strategy ending with open trades.

I've optimized the parameters for SPX.

Divergence for Many [Dimkud - v5]Strategy is based on "Divergence for Many Indicators v4 ST" strategy by CannyTolany01

which is based on "Divergence for Many Indicator" indicator by LonesomeTheBlue

This strategy is searching for divergences on 18 indicators which you can select and optimise one by one.

Additionally you can connect any other External Indicator value. (just add this indicator the the chart and select option in settings)

To the original indicator/strategy I have added 9 additional indicators:

( Money Flow Index, Williams_Vix, Stochastic RSI , SMI Ergodic Oscillator, Volume Weighted MACD , Bull Bear Power, Balance of Power , Relative Volatility Index , Logistic Settings).

Converted strategy to v5 of Pine Script.

Added Static SL/TP in percents (%).

Added filters to filter enters:

1. Volume Weighted MACD - Multi-TimeFrame Filter

(It checks for histogram to falling or rising for a set periods of bars)

2. Money Flow Index - Multi-TimeFrame Filter

(It checks if MFI Oscillator is in the set diapason.

Also It checks if MFI is falling or rising for a set periods of bars )

3. ATR filter

(check changes in fast ATR to slow ATR )

Strategy shows good backtest results on many crypto tokens on 45m - 1h periods. (with parameters optimisation for every indicator)

To find best parameters - you can enable indicators one-by one, and optimise best parameters for each of them.

Then enable all indicators with successful results.

Optimise SL/TP.

Then try to enable and optimise filters (channels etc.)

The better is to optimise parameters separately for Short and Long trading. And run two separate bots (in settings enable only Long or only Short.)

Updates:

- Added visualisation for open trades (SL/TP)

- Added Volatility filter by ATR with many options for tests.

- Fixed some small bugs.

- Added second RSI filter (you can use two RSIs with different TF or settings)

- Updated ATR volatility and MFI filter. Removed non-effective options

- Added CCI filter

- Added option to Enable/Disable visualisation of TP/SL on chart

- Fixed one small quick bug. ("ATR filter short" was not working)

- Added Super Trend filter

- Added Momentum filter

- Added Volume Filter

- All "request.security" MultiTimeFrame calls changed to 100% non-repait function "f_security()"

MVRV Z Score and MVRV Free Float Z-ScoreIMPORTANT: This script needs as much historic data as possible. Please run it on INDEX:BTCUSD , BNC:BLX or another chart of sufficient length.

MVRV

The MVRV (Market Value to Realised Value Ratio) simply divides bitcoins market cap by bitcoins realized market cap. This was previously impossible on Tradingview but has now been made possible thanks to Coinmetrics providing us with the realized market cap data.

In the free float version, the free float market cap is used instead of the regular market cap.

Z-Score

The MVRV Z-score divides the difference between Market cap and realized market cap by the historic standard deviation of the market cap.

Historically, this has been insanely accurate at detecting bitcoin tops and bottoms:

A Z-Score above 7 means bitcoin is vastly overpriced and at a local top.

A Z-Score below 0.1 means bitcoin is underpriced and at a local bottom.

In the free float version, the free float market cap is used instead of the regular market cap.

The Z-Score, also known as the standard score is hugely popular in a wide range of mathematical and statistical fields and is usually used to measure the number of standard deviations by which the value of a raw score is above or below the mean value of what is being observed or measured.

Credits

MVRV Z Score initially created by aweandwonder

MVRV initially created by Murad Mahmudov and David Puell

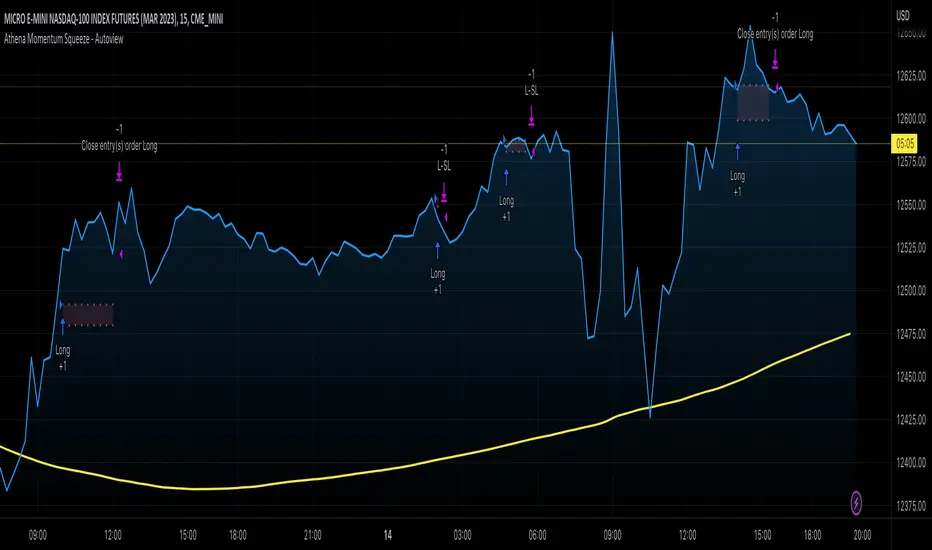

Athena Momentum Squeeze - Short, Lean, and Mean This is a very profitable strategy focusing on 15 minute intervals on the Micro Nasdaq Futures contracts. CME_MINI:MNQH2023

As this contract only keeps positions for on average about an hour risk is managed. At a profit factor of 3.382 with a max drawdown of $123 from January 1st to February 15. Looking back to Dec 2019 still maintains a profit factor of 1.3.

See backtesting: www.screencast.com

2019 backtesting: www.screencast.com

Based on the classic Lazy Bear Oscillator Squeeze with a number of modifications from ADX, MAs and adding fibonacci levels.

We like keeping strategies simple yet powerful, no completely where you can't understand your own trades.

Our team is always modifying and improving the strategy. Always open to collaborating on improving as there is no perfect strategy. www.screencast.com

Exponential Stochastic Strategywhat is Exponential Stochastic?

it is a modified version of the stochastic indicator. This strategy does not include pyramiding, repaint, trailing stop or take profit.

what it does?

It contains an extra input in addition to the stochastic indicator. Thanks to this input, different exponential weights can be given to the outputs and the indicator can be made more sensitive or insensitive. The strategy buys when the indicator leaves the overbought zone, sells when it leaves the oversold zone and always stays in the trade.

how it does it?

it uses this formula: i.hizliresim.com

Thanks to this formula, even if the weights given to the outputs change, the indicator always continues to take a value between 0 and 100.

how to use it ?

With the input named "exp", you can change the sensitivity of the indicator and develop different strategies. other inputs are the same as the stochastic indicator. Increasing the exp value causes the indicator to signal less, decreasing it makes it much more sensitive.

Fair Value Strategy UltimateThis is a strategy using an index's (SPX, NDX, RUT) Fair Value derived from Net Liquidity.

Net Liquidity function is simply: Fed Balance Sheet - Treasury General Account - Reverse Repo Balance

Formula for calculating the fair value of and Index using Net Liquidity looks like this: net_liquidity/1000000000/scalar - subtractor

The Index Fair Value is then subtracted from the Index value which creates an oscillating diff value.

When diff is greater than the overbought threshold, Index is considered overbought and we go short/sell.

When diff is less than the oversold signal, Index is considered oversold and we cover/buy.

The net liquidity values I calculate outside of TradingView. If you'd like the strategy to work for future dates, you'll need to update the reference to my NetLiquidityLibrary , which I update daily.

Parameters:

Index: SPX, NDX, RUT

Strategy: Short Only, Long Only, Long/Short

Inverse (bool): check if using an inverse ETF to go long instead of short.

Scalar (float)

Subtractor (int)

Overbought Threshold (int)

Oversold Threshold (int)

Start After Date: When the strategy should start trading

Close Date: Day to close open trades. I just like it to get complete results rather than the strategy ending with open trades.

Optimal Parameters:

I've optimized the parameters for each index using the python backtesting library and they are as follows =>

SPX

Scalar: 1.1

Subtractor: 1425

OB Threshold: 0

OS Threshold: -175

NDX

Scalar: 0.5

Subtractor: 250

OB Threshold: 0

OS Threshold: -25

RUT

Scalar: 3.2

Subtractor: 50

OB Threshold: 25

OS Threshold: -25

PSAR BBPT ZLSMA BTC 1minLong entry:

PSAR gives buy signal

BBPT prints green histogram

ZLSMA is below the price

ZLSMA has uptrend

SL is smaller than the max SL

Optional Sessions and EMA filters

Short entry

PSAR gives sell signal

BBPT prints red histogram

ZLSMA is above the price

ZLSMA has downtrend

SL is smaller than the max SL

Optional Sessions and EMA filters

SL:

Placed below ZLSMA + offset on long

Placed above ZLSMA + offset on short

TP1:

1x the SL by default

Takes no profit by default, 50% is also a good setting

TP2:

2x the SL by default

Take out all remaining position size.

If price reaches TP1, the SL is set to the entry price.

Super 8 - 30M BTCWelcome to Super 8, the ultimate automatic trading script for Pine!

This bad boy is designed to go both long and short, and it's equipped with all the tools you need to maximize your profits. Whether you're looking to take profit, set a trailing stop, or protect yourself with a stop loss, Super 8 has you covered.

But that's not all! Super 8 is also loaded with 8 powerful indicators to help you make informed decisions. We've got the EMA, ADX, SAR, MACD, VOLUME, BOLLINGER BANDS, DONCHIAN, and ATR all working together to give you the best possible trading experience.

And if you want to take it to the next level, Super 8 also has a feature that lets you use stepped entries in normal mode or incremental 1,2,3,... to improve your average price. Plus, if you're using trailing stop, you can activate the Backtest precision to use lower timeframes.

But what's in a name? Super 8 is called that because it's just that... super! It's tailored specifically for the OKX:BTCUSDT.P pair, so you know you're getting the best possible results. it's highly adjustable and can be used with any other pair. So no matter what market you're trading in, Super 8 has got you covered.

So if you want to level up your trading game, give Super 8 a try. You won't be disappointed.

Certain Risks of Live Algorithmic Trading:

Backtesting Cannot Assure Actual Results.

The relevant market might fail or behave unexpectedly.

Your broker may experience failures in its infrastructure, fail to execute your orders in a correct or timely fashion or reject your orders.

The system you use for generating trading orders, communicating those orders to your broker, and receiving queries and trading results from your broker may fail.

Time lag at various point in live trading might cause unexpected behavior.

The systems of third parties in addition to those of the provider from which we obtain various services, your broker, and the applicable securities market may fail or malfunction.

DRM StrategyOne of the ways I go when I develop strategies is by reducing the number of parameters and removing fixed parameters and levels.

In this strategy, I'm trying to create an RSI indicator with a dynamic length.

Length is computed based on the correlation between Price and its momentum.

You can set min and max values for the RSI, and if the correlation is close to 1, we'll be at a min RSI value. When it's -1, we'll be at the max level.

I got this idea from Sofien Kaabar's book.

The strategy is super simple, and there might be much room for improvement.

Performance on the deep backtesting is not excellent, so I think the strategy needs some filters for regimes, etc.

Thanks to @MUQWISHI for helping me code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.