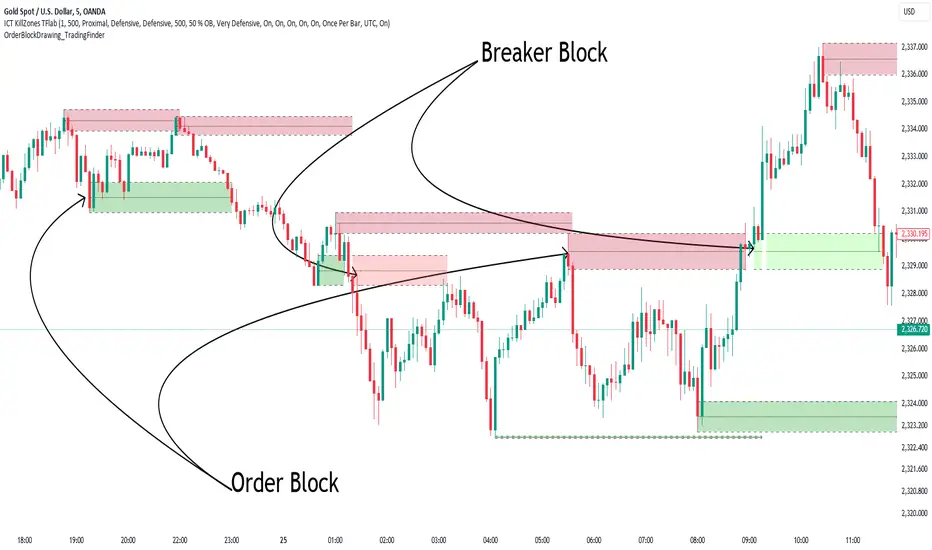

Order Block Drawing [TradingFinder]🔵 Introduction

Perhaps one of the most challenging tasks for Pine script developers (especially beginners) is properly drawing order blocks. While utilizing the latest technical analysis methods for "Price Action," beginners heavily rely on accurately plotting "Supply" and "Demand" zones, following concepts like "Smart Money Concept" and "ICT".

However, drawing "Order Blocks" may pose a challenge for developers. Therefore, to minimize bugs, increase accuracy, and speed up the process of coding order blocks, we have released the "Order Block Drawing" library.

Below, you can read more details about how to use this library.

Important :

This library has direct and indirect outputs. The indirect output includes the ranges of order blocks plotted on the chart. However, the direct output is a "Boolean" value that becomes "true" only when the price touches an order block, colloquially termed as "Mitigate." You can use this output for setting up alerts.

🔵 How to Use

First, you can add the library to your code as shown in the example below.

import TFlab/OrderBlockDrawing_TradingFinder/1

🟣Parameters

OBDrawing(OBType, TriggerCondition, DistalPrice, ProximalPrice, Index, OBValidDis, Show, ColorZone) =>

Parameters:

• OBType (string)

• TriggerCondition (bool)

• DistalPrice (float)

• ProximalPrice (float)

• Index (int)

• OBValidDis (int)

• Show (bool)

• ColorZone (color)

OBType : All order blocks are summarized into two types: "Supply" and "Demand." You should input your order block type in this parameter. Enter "Demand" for drawing demand zones and "Supply" for drawing supply zones.

TriggerCondition : Input the condition under which you want the order block to be drawn in this parameter.

DistalPrice : Generally, if each zone is formed by two lines, the farthest line from the price is termed "Distal." This input receives the price of the "Distal" line.

ProximalPrice : Generally, if each zone is formed by two lines, the nearest line to the price is termed "Proximal" line.

Index : This input receives the value of the "bar_index" at the beginning of the order block. You should store the "bar_index" value at the occurrence of the condition for the order block to be drawn and input it here.

OBValidDis : Order blocks continue to be drawn until a new order block is drawn or the order block is "Mitigate." You can specify how many candles after their initiation order blocks should continue. If you want no limitation, enter the number 4998.

Show : You may need to manage whether to display or hide order blocks. When this input is "On", order blocks are displayed, and when it's "Off", order blocks are not displayed.

ColorZone : You can input your preferred color for drawing order blocks.

🔵 Function Outputs

This function has only one output. This output is of type "Boolean" and becomes "true" only when the price touches an order block. Each order block can be touched only once and then loses its validity. You can use this output for alerts.

= Drawing.OBDrawing('Demand', Condition, Distal, Proximal, Index, 4998, true, Color)

指標和策略

mathLibrary "math"

It's a library of discrete aproximations of a price or Series float it uses Fourier Discrete transform, Laplace Discrete Original and Modified transform and Euler's Theoreum for Homogenus White noice operations. Calling functions without source value it automatically take close as the default source value.

Here is a picture of Laplace and Fourier approximated close prices from this library:

Copy this indicator and try it yourself:

import AutomatedTradingAlgorithms/math/1 as math

//@version=5

indicator("Close Price with Aproximations", shorttitle="Close and Aproximations", overlay=false)

// Sample input data (replace this with your own data)

inputData = close

// Plot Close Price

plot(inputData, color=color.blue, title="Close Price")

ltf32_result = math.LTF32(a=0.01)

plot(ltf32_result, color=color.green, title="LTF32 Aproximation")

fft_result = math.FFT()

plot(fft_result, color=color.red, title="Fourier Aproximation")

wavelet_result = math.Wavelet()

plot(wavelet_result, color=color.orange, title="Wavelet Aproximation")

wavelet_std_result = math.Wavelet_std()

plot(wavelet_std_result, color=color.yellow, title="Wavelet_std Aproximation")

DFT3(xval, _dir)

Discrete Fourier Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

DFT2(xval, _dir)

Discrete Fourier Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

FFT(xval)

Fast Fourier Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DFT32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DTF32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

LFT3(xval, _dir, a)

Discrete Laplace Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT2(xval, _dir, a)

Discrete Laplace Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT(xval, a)

Fast Laplace Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LTF32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

whitenoise(indic_, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise, without extra aproximated src.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

whitenoise(indic_, dft1, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise and DFT1.

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

dft1 (float) : Aproximated src value for white noice calculation

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

smooth(dft1, indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series and aproximated source value

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

dft1 (float) : Value to be smoothed.

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed source (src) series

smooth(indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed src series

vzo_ema(src, len)

Volume Zone Oscillator with EMA smoothing

Parameters:

src (float) : Source series

len (simple int) : Length parameter for EMA

Returns: VZO value

vzo_sma(src, len)

Volume Zone Oscillator with SMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for SMA

Returns: VZO value

vzo_wma(src, len)

Volume Zone Oscillator with WMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for WMA

Returns: VZO value

alma2(series, windowsize, offset, sigma)

Arnaud Legoux Moving Average 2 accepts sigma as series float

Parameters:

series (float) : Input series

windowsize (int) : Size of the moving average window

offset (float) : Offset parameter

sigma (float) : Sigma parameter

Returns: ALMA value

Wavelet(src, len, offset, sigma)

Aproxiates srt using Discrete wavelet transform.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (simple float)

sigma (simple float)

Returns: Wavelet-transformed series

Wavelet_std(src, len, offset, mag)

Aproxiates srt using Discrete wavelet transform with standard deviation as a magnitude.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (float) : Offset parameter for ALMA

mag (int) : Magnitude parameter for standard deviation

Returns: Wavelet-transformed series

LaplaceTransform(xval, N, a)

Original Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

Returns: Aproxiated source value

NLaplaceTransform(xval, N, a, repeat)

Y repetirions on Original Laplace Transform over N set of close prices, each time N-k set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformsum(xval, N, a, b)

Sum of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiff(xval, N, a, b, repeat)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiff(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, with dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiff(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor, dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiffFrom2(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

time_and_sessionA library that provides utilities for working with trading sessions and time-based conditions. Functions include session checks, date range checks, day-of-week matching, and session high/low calculations for daily, weekly, monthly, and yearly timeframes. This library streamlines time-related calculations and enhances time-based strategies and indicators.

Library "time_and_session"

Provides functions for checking time and session-based conditions and retrieving session-specific high and low values.

is_session(session, timeframe, timezone)

Checks if the current time is within the specified trading session

Parameters:

session (string) : The trading session, defined using input.session()

timeframe (string) : The timeframe to use, defaults to the current chart's timeframe

timezone (string) : The timezone to use, defaults to the symbol's timezone

Returns: A boolean indicating whether the current time is within the specified trading session

is_date_range(start_time, end_time)

Checks if the current time is within a specified date range

Parameters:

start_time (int) : The start time, defined using input.time()

end_time (int) : The end time, defined using input.time()

Returns: A boolean indicating whether the current time is within the specified date range

is_day_of_week(sunday, monday, tuesday, wednesday, thursday, friday, saturday)

Checks if the current day of the week matches any of the specified days

Parameters:

sunday (bool) : A boolean indicating whether to check for Sunday

monday (bool) : A boolean indicating whether to check for Monday

tuesday (bool) : A boolean indicating whether to check for Tuesday

wednesday (bool) : A boolean indicating whether to check for Wednesday

thursday (bool) : A boolean indicating whether to check for Thursday

friday (bool) : A boolean indicating whether to check for Friday

saturday (bool) : A boolean indicating whether to check for Saturday

Returns: A boolean indicating whether the current day of the week matches any of the specified days

daily_high(source)

Returns the highest value of the specified source during the current daily session

Parameters:

source (float) : The data series to evaluate, defaults to high

Returns: The highest value during the current daily session, or na if the timeframe is not suitable

daily_low(source)

Returns the lowest value of the specified source during the current daily session

Parameters:

source (float) : The data series to evaluate, defaults to low

Returns: The lowest value during the current daily session, or na if the timeframe is not suitable

regular_session_high(source, persist)

Returns the highest value of the specified source during the current regular trading session

Parameters:

source (float) : The data series to evaluate, defaults to high

persist (bool) : A boolean indicating whether to retain the last value outside of regular market hours, defaults to true

Returns: The highest value during the current regular trading session, or na if the timeframe is not suitable

regular_session_low(source, persist)

Returns the lowest value of the specified source during the current regular trading session

Parameters:

source (float) : The data series to evaluate, defaults to low

persist (bool) : A boolean indicating whether to retain the last value outside of regular market hours, defaults to true

Returns: The lowest value during the current regular trading session, or na if the timeframe is not suitable

premarket_session_high(source, persist)

Returns the highest value of the specified source during the current premarket trading session

Parameters:

source (float) : The data series to evaluate, defaults to high

persist (bool) : A boolean indicating whether to retain the last value outside of premarket hours, defaults to true

Returns: The highest value during the current premarket trading session, or na if the timeframe is not suitable

premarket_session_low(source, persist)

Returns the lowest value of the specified source during the current premarket trading session

Parameters:

source (float) : The data series to evaluate, defaults to low

persist (bool) : A boolean indicating whether to retain the last value outside of premarket hours, defaults to true

Returns: The lowest value during the current premarket trading session, or na if the timeframe is not suitable

postmarket_session_high(source, persist)

Returns the highest value of the specified source during the current postmarket trading session

Parameters:

source (float) : The data series to evaluate, defaults to high

persist (bool) : A boolean indicating whether to retain the last value outside of postmarket hours, defaults to true

Returns: The highest value during the current postmarket trading session, or na if the timeframe is not suitable

postmarket_session_low(source, persist)

Returns the lowest value of the specified source during the current postmarket trading session

Parameters:

source (float) : The data series to evaluate, defaults to low

persist (bool) : A boolean indicating whether to retain the last value outside of postmarket hours, defaults to true

Returns: The lowest value during the current postmarket trading session, or na if the timeframe is not suitable

weekly_high(source)

Returns the highest value of the specified source during the current weekly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to high

Returns: The highest value during the current weekly session, or na if the timeframe is not suitable

weekly_low(source)

Returns the lowest value of the specified source during the current weekly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to low

Returns: The lowest value during the current weekly session, or na if the timeframe is not suitable

monthly_high(source)

Returns the highest value of the specified source during the current monthly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to high

Returns: The highest value during the current monthly session, or na if the timeframe is not suitable

monthly_low(source)

Returns the lowest value of the specified source during the current monthly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to low

Returns: The lowest value during the current monthly session, or na if the timeframe is not suitable

yearly_high(source)

Returns the highest value of the specified source during the current yearly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to high

Returns: The highest value during the current yearly session, or na if the timeframe is not suitable

yearly_low(source)

Returns the lowest value of the specified source during the current yearly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to low

Returns: The lowest value during the current yearly session, or na if the timeframe is not suitable

garbage_collection_and_utilitiesGarbage Collection and Utilities is a library that offers a set of functions designed for efficient management of various types of arrays. This library provides garbage collection utilities to remove and delete excess elements, and also includes utilities for checking the size of arrays. It's particularly useful for developers who want to manage labels, lines, polylines, boxes, linefills, chart points, floats, integers, booleans, and strings efficiently within their scripts.

Both dump and trim act on the array backwards . This means that for trim , the elements that will be left start from 0. If you want the most recent element to be left after trim, you must use unshift().

Garbage Collection:

Functions to remove and delete excess elements from various types of arrays.

Useful for freeing up memory and keeping the arrays within desired size limits.

Size Checking:

Functions to check if arrays are larger than a specified size.

Helps in ensuring that arrays have enough elements before performing operations.

Supported Types:

Compatible with a wide range of array types, including labels, lines, polylines, boxes, linefills, chart points, floats, integers, booleans, and strings.

Usage:

The dump methods are ideal for clearing out unwanted elements from arrays, while the trim methods allow for more refined control over the size of arrays.

The ready methods enable you to verify if arrays have the required number of elements before proceeding with further operations.

Library "garbage_collection_and_utilities"

Provides garbage collection utilities for managing and trimming various types of arrays, and utilities to check if an array is of a specific size. Included types are: labels, lines, polylines, boxes, linefills, chart points, floats, integers, booleans, and strings.

method ready(self, size)

Checks if an array of labels is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method ready(self, size)

Checks if an array of lines is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method ready(self, size)

Checks if an array of polylines is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method ready(self, size)

Checks if an array of boxes is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method ready(self, size)

Checks if an array of linefills is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method ready(self, size)

Checks if an array of chart points is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method ready(self, size)

Checks if an array of floats is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method ready(self, size)

Checks if an array of integers is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method ready(self, size)

Checks if an array of booleans is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method ready(self, size)

Checks if an array of strings is larger than a specified size

Namespace types: array

Parameters:

self (array)

size (int) : The minimum size of the array

Returns: A boolean indicating whether the array is ready

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of labels

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of lines

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of polylines

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of boxes

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of linefills

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of chart points

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of floats

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of integers

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of booleans

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method dump(self, max_size, trigger)

Removes and deletes excess elements from an array of strings

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

trigger (bool) : A condition to trigger the dumping process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of labels

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of lines

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of polylines

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of boxes

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of linefills

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of chart points

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of floats

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of integers

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of booleans

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

method trim(self, max_size, min_size, trigger)

Removes excess elements and trims an array of strings

Namespace types: array

Parameters:

self (array)

max_size (int) : The maximum size of the array

min_size (int) : The minimum size of the array

trigger (bool) : A condition to trigger the trimming process

Returns: void

AminioLibraryLibrary "AminioLibrary"

: this is my personal library that is being used in different indicators and strategies

calculateMA(source, len, maType)

This fuction returns a moving average value based on the type

Parameters:

source (float) : Is the time series source to calculate average from

len (simple int) : The length of the moving average, this should be integer

maType (string) : The type of moving average, acceptable types are : SMA, HMA, EMA, RMA, WMA, VWMA

Returns: value of moving average

atr(source, len)

This fuction returns atr value for a given source

Parameters:

source (float) : Is the time series source to calculate atr from

len (simple int) : The length of the atr, this should be integer

Returns: value of atr from source

superTrend(source, factor, len)

This fuction returns value of super trend indicator and the trend direction as a tupple

Parameters:

source (float) : Is the time series source to calculate super trend from

factor (simple float) : The multiplication factor for upper and lower band calcualtion, this can be a float

len (simple int) : The length of the super trend, this should be integer

Returns: value of atr from source

halfTrend(am, chdev)

This fuction returns a hTrend type carrying different values for half trend indicator

Parameters:

am (int) : This is the amplitude used for calcucating the half trend, use integers

chdev (float) : This is the Channel Deviation value used for calculating upper and lower atr channel boundaries, you can use floats

Returns: hTrend data type

hTrend

Fields:

halfTrend (series__float)

trend (series__integer)

atrHigh (series__float)

atrLow (series__float)

arrowUp (series__float)

arrowDown (series__float)

Order Block Refiner [TradingFinder]🔵 Introduction

The "Refinement" feature allows you to adjust the width of the order block according to your strategy. There are two modes, "Aggressive" and "Defensive," in the "Order Block Refine". The difference between "Aggressive" and "Defensive" lies in the width of the order block.

For risk-averse traders, the "Defensive" mode is suitable as it provides a lower loss limit and a greater reward-to-risk ratio. For risk-taking traders, the "Aggressive" mode is more appropriate. These traders prefer to enter trades at higher prices, and this mode, which has a wider order block width, is more suitable for this group of individuals.

Important :

One of the advantages of using this library is increased code accuracy. Not only does it have the capability to create order blocks, but you can also simply define the condition for order block creation (true/false) and "bar_index," and you'll find the primary range without applying any filters.

🟣 Order Block Refinement Algorithm

The order block ranges are filtered in two stages. In the first stage, the "Open," "High," "Low," and "Close" of the current order block candle, its two or three previous candles, and one subsequent candle (if available) are examined. In this stage, minimum and maximum distances are calculated, and logical range filters are applied.

In the second stage, two modes, "Aggressive" and "Defensive," are calculated.

For the "Defensive" mode, the width of these ranges is compared with the "ATR" (Average True Range) of period 55, and if they are smaller than "ATR" or 1 to more than 4 times "ATR," the width of the range is reduced from 0 to 80 percent.

For the "Aggressive" mode, you get the same output as the first filter, which usually has a wider width than the "Defensive" mode.

• Order Block Refiner : Off

• Order Block Refiner : On / "Aggressive Mode"

• Order Block Refiner : On / "Defensive Mode"

🔵 How to Use

OBRefiner(string OBType, string OBRefine, string RefineMethod, bool TriggerCondition, int Index) =>

Parameters:

• OBType (string)

• OBRefine (string)

• RefineMethod (string)

• TriggerCondition (bool)

• Index (int)

To add "Order Block Refiner Library", you must first add the following code to your script.

import TFlab/OrderBlockRefiner_TradingFinder/1

OBType : This parameter receives 2 inputs. If the order block you want to "Refine" is of type demand, you should enter "Demand," and if it's of type supply, you should enter "Supply."

OBRefine : Set to "On" if you want the "Refine" operation to be performed. Otherwise, set to "Off."

RefineMethod : This input receives 2 modes, "Aggressive" and "Defensive." You can switch between these modes according to your needs.

TriggerCondition : Enter the condition with which the order block is formed in this parameter.

Index : Enter the "bar_index" of the candle where the order block is formed in this parameter.

🟣 Function Outputs

This function has 6 outputs: "bar_index" at the beginning of the "Distal" line, "bar_index+1" at the end of the "Distal" line, "Price" at the "Distal" line, "bar_index" at the beginning of the "Proximal" line, "bar_index+1" at the end of the "Proximal" line, and "Price" at the "Proximal" line, which can be used to draw order blocks.

Sample :

= Refiner.OBRefiner('Demand', 'Off', 'Aggressive',BuMChMain_Trigger, BuMChMain_Index)

if BuMChMain_Trigger

BuMChHlineMain := line.new(BuMChMain_Xp1 , BuMChMain_Yp12 , bar_index , BuMChMain_Yp12, color = color.black , style = line.style_dotted)

BuMChLlineMain := line.new(BuMChMain_Xd1 , BuMChMain_Yd12 , bar_index , BuMChMain_Yd12, color = color.black , style = line.style_dotted)

BuMChFilineMain := linefill.new(BuMChHlineMain ,BuMChLlineMain , color = color.rgb(76, 175, 80 , 75 ) )

Monty3192_LibraryLibrary "Monty3192_Library"

Libreria Monty3192 - MontyTrader

calc_func(inversion1, inversion2, inversion3, inversion4, inversion5, inversion6, inversion7, inversion8, inversion9, inversion10, precio1, precio2, precio3, precio4, precio5, precio6, precio7, precio8, precio9, precio10, act_1, act_2, act_3, act_4, act_5, act_6, act_7, act_8, act_9, act_10)

Parameters:

inversion1 (float)

inversion2 (float)

inversion3 (float)

inversion4 (float)

inversion5 (float)

inversion6 (float)

inversion7 (float)

inversion8 (float)

inversion9 (float)

inversion10 (float)

precio1 (float)

precio2 (float)

precio3 (float)

precio4 (float)

precio5 (float)

precio6 (float)

precio7 (float)

precio8 (float)

precio9 (float)

precio10 (float)

act_1 (bool)

act_2 (bool)

act_3 (bool)

act_4 (bool)

act_5 (bool)

act_6 (bool)

act_7 (bool)

act_8 (bool)

act_9 (bool)

act_10 (bool)

rend_func(p1, p2, p3, p4, p5, p6, p7, p8, p9, p10, po)

Parameters:

p1 (float)

p2 (float)

p3 (float)

p4 (float)

p5 (float)

p6 (float)

p7 (float)

p8 (float)

p9 (float)

p10 (float)

po (float)

f_drawLine(cond, x1, y1, x2, y2, colorr, txt, act, offset, txtc, txts)

Parameters:

cond (bool)

x1 (int)

y1 (float)

x2 (int)

y2 (float)

colorr (color)

txt (string)

act (bool)

offset (int)

txtc (color)

txts (string)

f_Vline(cond, x1, y1, x2, y2, colorr, txt, sel, txts, txtc)

Parameters:

cond (bool)

x1 (int)

y1 (float)

x2 (int)

y2 (float)

colorr (color)

txt (string)

sel (bool)

txts (string)

txtc (color)

get_all_time_high()

TRADINGLibrary "TRADING"

This library is a client script for making a webhook signal formatted string to PoABOT server.

entry_message(password, percent, leverage, margin_mode, kis_number)

Create a entry message for POABOT

Parameters:

password (string) : (string) The password of your bot.

percent (float) : (float) The percent for entry based on your wallet balance.

leverage (int) : (int) The leverage of entry. If not set, your levereage doesn't change.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account. Default 1

Returns: (string) A json formatted string for webhook message.

order_message(password, percent, leverage, margin_mode, kis_number)

Create a order message for POABOT

Parameters:

password (string) : (string) The password of your bot.

percent (float) : (float) The percent for entry based on your wallet balance.

leverage (int) : (int) The leverage of entry. If not set, your levereage doesn't change.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account. Default 1

Returns: (string) A json formatted string for webhook message.

close_message(password, percent, margin_mode, kis_number)

Create a close message for POABOT

Parameters:

password (string) : (string) The password of your bot.

percent (float) : (float) The percent for close based on your wallet balance.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account. Default 1

Returns: (string) A json formatted string for webhook message.

exit_message(password, percent, margin_mode, kis_number)

Create a exit message for POABOT

Parameters:

password (string) : (string) The password of your bot.

percent (float) : (float) The percent for exit based on your wallet balance.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account. Default 1

Returns: (string) A json formatted string for webhook message.

manual_message(password, exchange, base, quote, side, qty, price, percent, leverage, margin_mode, kis_number, order_name)

Create a manual message for POABOT

Parameters:

password (string) : (string) The password of your bot.

exchange (string) : (string) The exchange

base (string) : (string) The base

quote (string) : (string) The quote of order message

side (string) : (string) The side of order messsage

qty (float) : (float) The qty of order message

price (float) : (float) The price of order message

percent (float) : (float) The percent for order based on your wallet balance.

leverage (int) : (int) The leverage of entry. If not set, your levereage doesn't change.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account.

order_name (string) : (string) The name of order message

Returns: (string) A json formatted string for webhook message.

in_trade(start_time, end_time, hide_trade_line)

Create a trade start line

Parameters:

start_time (int) : (int) The start of time.

end_time (int) : (int) The end of time.

hide_trade_line (bool) : (bool) if true, hide trade line. Default false.

Returns: (bool) Get bool for trade based on time range.

real_qty(qty, precision, leverage, contract_size, default_qty_type, default_qty_value)

Get exchange specific real qty

Parameters:

qty (float) : (float) qty

precision (float) : (float) precision

leverage (int) : (int) leverage

contract_size (float) : (float) contract_size

default_qty_type (string)

default_qty_value (float)

Returns: (float) exchange specific qty.

method set(this, password, start_time, end_time, leverage, initial_capital, default_qty_type, default_qty_value, margin_mode, contract_size, kis_number, entry_percent, close_percent, exit_percent, fixed_qty, fixed_cash, real, auto_alert_message, hide_trade_line)

Set bot object.

Namespace types: bot

Parameters:

this (bot)

password (string) : (string) password for poabot.

start_time (int) : (int) start_time timestamp.

end_time (int) : (int) end_time timestamp.

leverage (int) : (int) leverage.

initial_capital (float)

default_qty_type (string)

default_qty_value (float)

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

contract_size (float)

kis_number (int) : (int) kis_number for poabot.

entry_percent (float) : (float) entry_percent for poabot.

close_percent (float) : (float) close_percent for poabot.

exit_percent (float) : (float) exit_percent for poabot.

fixed_qty (float) : (float) fixed qty.

fixed_cash (float) : (float) fixed cash.

real (bool) : (bool) convert qty for exchange specific.

auto_alert_message (bool) : (bool) convert alert_message for exchange specific.

hide_trade_line (bool) : (bool) if true, Hide trade line. Default false.

Returns: (void)

method print(this, message)

Print message using log table.

Namespace types: bot

Parameters:

this (bot)

message (string)

Returns: (void)

method start_trade(this)

start trade using start_time and end_time

Namespace types: bot

Parameters:

this (bot)

Returns: (void)

method entry(this, id, direction, qty, limit, stop, oca_name, oca_type, comment, alert_message, when)

It is a command to enter market position. If an order with the same ID is already pending, it is possible to modify the order. If there is no order with the specified ID, a new order is placed. To deactivate an entry order, the command strategy.cancel or strategy.cancel_all should be used. In comparison to the function strategy.order, the function strategy.entry is affected by pyramiding and it can reverse market position correctly. If both 'limit' and 'stop' parameters are 'NaN', the order type is market order.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to cancel or modify an order by referencing its identifier.

direction (string) : (string) A required parameter. Market position direction: 'strategy.long' is for long, 'strategy.short' is for short.

qty (float) : (float) An optional parameter. Number of contracts/shares/lots/units to trade. The default value is 'NaN'.

limit (float) : (float) An optional parameter. Limit price of the order. If it is specified, the order type is either 'limit', or 'stop-limit'. 'NaN' should be specified for any other order type.

stop (float) : (float) An optional parameter. Stop price of the order. If it is specified, the order type is either 'stop', or 'stop-limit'. 'NaN' should be specified for any other order type.

oca_name (string) : (string) An optional parameter. Name of the OCA group the order belongs to. If the order should not belong to any particular OCA group, there should be an empty string.

oca_type (string) : (string) An optional parameter. Type of the OCA group. The allowed values are: "strategy.oca.none" - the order should not belong to any particular OCA group; "strategy.oca.cancel" - the order should belong to an OCA group, where as soon as an order is filled, all other orders of the same group are cancelled; "strategy.oca.reduce" - the order should belong to an OCA group, where if X number of contracts of an order is filled, number of contracts for each other order of the same OCA group is decreased by X.

comment (string) : (string) An optional parameter. Additional notes on the order.

alert_message (string) : (string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method order(this, id, direction, qty, limit, stop, oca_name, oca_type, comment, alert_message, when)

It is a command to place order. If an order with the same ID is already pending, it is possible to modify the order. If there is no order with the specified ID, a new order is placed. To deactivate order, the command strategy.cancel or strategy.cancel_all should be used. In comparison to the function strategy.entry, the function strategy.order is not affected by pyramiding. If both 'limit' and 'stop' parameters are 'NaN', the order type is market order.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to cancel or modify an order by referencing its identifier.

direction (string) : (string) A required parameter. Market position direction: 'strategy.long' is for long, 'strategy.short' is for short.

qty (float) : (float) An optional parameter. Number of contracts/shares/lots/units to trade. The default value is 'NaN'.

limit (float) : (float) An optional parameter. Limit price of the order. If it is specified, the order type is either 'limit', or 'stop-limit'. 'NaN' should be specified for any other order type.

stop (float) : (float) An optional parameter. Stop price of the order. If it is specified, the order type is either 'stop', or 'stop-limit'. 'NaN' should be specified for any other order type.

oca_name (string) : (string) An optional parameter. Name of the OCA group the order belongs to. If the order should not belong to any particular OCA group, there should be an empty string.

oca_type (string) : (string) An optional parameter. Type of the OCA group. The allowed values are: "strategy.oca.none" - the order should not belong to any particular OCA group; "strategy.oca.cancel" - the order should belong to an OCA group, where as soon as an order is filled, all other orders of the same group are cancelled; "strategy.oca.reduce" - the order should belong to an OCA group, where if X number of contracts of an order is filled, number of contracts for each other order of the same OCA group is decreased by X.

comment (string) : (string) An optional parameter. Additional notes on the order.

alert_message (string) : (string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method close_all(this, comment, alert_message, immediately, when)

Exits the current market position, making it flat.

Namespace types: bot

Parameters:

this (bot)

comment (string) : (string) An optional parameter. Additional notes on the order.

alert_message (string) : (string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

immediately (bool) : (bool) An optional parameter. If true, the closing order will be executed on the tick where it has been placed, ignoring the strategy parameters that restrict the order execution to the open of the next bar. The default is false.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method cancel(this, id, when)

It is a command to cancel/deactivate pending orders by referencing their names, which were generated by the functions: strategy.order, strategy.entry and strategy.exit.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to cancel an order by referencing its identifier.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method cancel_all(this, when)

It is a command to cancel/deactivate all pending orders, which were generated by the functions: strategy.order, strategy.entry and strategy.exit.

Namespace types: bot

Parameters:

this (bot)

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method close(this, id, comment, qty, qty_percent, alert_message, immediately, when)

It is a command to exit from the entry with the specified ID. If there were multiple entry orders with the same ID, all of them are exited at once. If there are no open entries with the specified ID by the moment the command is triggered, the command will not come into effect. The command uses market order. Every entry is closed by a separate market order.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to close an order by referencing its identifier.

comment (string) : (string) An optional parameter. Additional notes on the order.

qty (float) : (float) An optional parameter. Number of contracts/shares/lots/units to exit a trade with. The default value is 'NaN'.

qty_percent (float) : (float) Defines the percentage (0-100) of the position to close. Its priority is lower than that of the 'qty' parameter. Optional. The default is 100.

alert_message (string) : (string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

immediately (bool) : (bool) An optional parameter. If true, the closing order will be executed on the tick where it has been placed, ignoring the strategy parameters that restrict the order execution to the open of the next bar. The default is false.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

ticks_to_price(ticks, from)

Converts ticks to a price offset from the supplied price or the average entry price.

Parameters:

ticks (float) : (float) Ticks to convert to a price.

from (float) : (float) A price that can be used to calculate from. Optional. The default value is `strategy.position_avg_price`.

Returns: (float) A price level that has a distance from the entry price equal to the specified number of ticks.

method exit(this, id, from_entry, qty, qty_percent, profit, limit, loss, stop, trail_price, trail_points, trail_offset, oca_name, comment, comment_profit, comment_loss, comment_trailing, alert_message, alert_profit, alert_loss, alert_trailing, when)

It is a command to exit either a specific entry, or whole market position. If an order with the same ID is already pending, it is possible to modify the order. If an entry order was not filled, but an exit order is generated, the exit order will wait till entry order is filled and then the exit order is placed. To deactivate an exit order, the command strategy.cancel or strategy.cancel_all should be used. If the function strategy.exit is called once, it exits a position only once. If you want to exit multiple times, the command strategy.exit should be called multiple times. If you use a stop loss and a trailing stop, their order type is 'stop', so only one of them is placed (the one that is supposed to be filled first). If all the following parameters 'profit', 'limit', 'loss', 'stop', 'trail_points', 'trail_offset' are 'NaN', the command will fail. To use market order to exit, the command strategy.close or strategy.close_all should be used.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to cancel or modify an order by referencing its identifier.

from_entry (string) : (string) An optional parameter. The identifier of a specific entry order to exit from it. To exit all entries an empty string should be used. The default values is empty string.

qty (float) : (float) An optional parameter. Number of contracts/shares/lots/units to exit a trade with. The default value is 'NaN'.

qty_percent (float) : (float) Defines the percentage of (0-100) the position to close. Its priority is lower than that of the 'qty' parameter. Optional. The default is 100.

profit (float) : (float) An optional parameter. Profit target (specified in ticks). If it is specified, a limit order is placed to exit market position when the specified amount of profit (in ticks) is reached. The default value is 'NaN'.

limit (float) : (float) An optional parameter. Profit target (requires a specific price). If it is specified, a limit order is placed to exit market position at the specified price (or better). Priority of the parameter 'limit' is higher than priority of the parameter 'profit' ('limit' is used instead of 'profit', if its value is not 'NaN'). The default value is 'NaN'.

loss (float) : (float) An optional parameter. Stop loss (specified in ticks). If it is specified, a stop order is placed to exit market position when the specified amount of loss (in ticks) is reached. The default value is 'NaN'.

stop (float) : (float) An optional parameter. Stop loss (requires a specific price). If it is specified, a stop order is placed to exit market position at the specified price (or worse). Priority of the parameter 'stop' is higher than priority of the parameter 'loss' ('stop' is used instead of 'loss', if its value is not 'NaN'). The default value is 'NaN'.

trail_price (float) : (float) An optional parameter. Trailing stop activation level (requires a specific price). If it is specified, a trailing stop order will be placed when the specified price level is reached. The offset (in ticks) to determine initial price of the trailing stop order is specified in the 'trail_offset' parameter: X ticks lower than activation level to exit long position; X ticks higher than activation level to exit short position. The default value is 'NaN'.

trail_points (float) : (float) An optional parameter. Trailing stop activation level (profit specified in ticks). If it is specified, a trailing stop order will be placed when the calculated price level (specified amount of profit) is reached. The offset (in ticks) to determine initial price of the trailing stop order is specified in the 'trail_offset' parameter: X ticks lower than activation level to exit long position; X ticks higher than activation level to exit short position. The default value is 'NaN'.

trail_offset (float) : (float) An optional parameter. Trailing stop price (specified in ticks). The offset in ticks to determine initial price of the trailing stop order: X ticks lower than 'trail_price' or 'trail_points' to exit long position; X ticks higher than 'trail_price' or 'trail_points' to exit short position. The default value is 'NaN'.

oca_name (string) : (string) An optional parameter. Name of the OCA group (oca_type = strategy.oca.reduce) the profit target, the stop loss / the trailing stop orders belong to. If the name is not specified, it will be generated automatically.

comment (string) : (string) Additional notes on the order. If specified, displays near the order marker on the chart. Optional. The default is na.

comment_profit (string) : (string) Additional notes on the order if the exit was triggered by crossing `profit` or `limit` specifically. If specified, supercedes the `comment` parameter and displays near the order marker on the chart. Optional. The default is na.

comment_loss (string) : (string) Additional notes on the order if the exit was triggered by crossing `stop` or `loss` specifically. If specified, supercedes the `comment` parameter and displays near the order marker on the chart. Optional. The default is na.

comment_trailing (string) : (string) Additional notes on the order if the exit was triggered by crossing `trail_offset` specifically. If specified, supercedes the `comment` parameter and displays near the order marker on the chart. Optional. The default is na.

alert_message (string) : (string) Text that will replace the '{{strategy.order.alert_message}}' placeholder when one is used in the "Message" field of the "Create Alert" dialog. Optional. The default is na.

alert_profit (string) : (string) Text that will replace the '{{strategy.order.alert_message}}' placeholder when one is used in the "Message" field of the "Create Alert" dialog. Only replaces the text if the exit was triggered by crossing `profit` or `limit` specifically. Optional. The default is na.

alert_loss (string) : (string) Text that will replace the '{{strategy.order.alert_message}}' placeholder when one is used in the "Message" field of the "Create Alert" dialog. Only replaces the text if the exit was triggered by crossing `stop` or `loss` specifically. Optional. The default is na.

alert_trailing (string) : (string) Text that will replace the '{{strategy.order.alert_message}}' placeholder when one is used in the "Message" field of the "Create Alert" dialog. Only replaces the text if the exit was triggered by crossing `trail_offset` specifically. Optional. The default is na.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

percent_to_ticks(percent, from)

Converts a percentage of the supplied price or the average entry price to ticks.

Parameters:

percent (float) : (float) The percentage of supplied price to convert to ticks. 50 is 50% of the entry price.

from (float) : (float) A price that can be used to calculate from. Optional. The default value is `strategy.position_avg_price`.

Returns: (float) A value in ticks.

percent_to_price(percent, from)

Converts a percentage of the supplied price or the average entry price to a price.

Parameters:

percent (float) : (float) The percentage of the supplied price to convert to price. 50 is 50% of the supplied price.

from (float) : (float) A price that can be used to calculate from. Optional. The default value is `strategy.position_avg_price`.

Returns: (float) A value in the symbol's quote currency (USD for BTCUSD).

bot

Fields:

password (series__string)

start_time (series__integer)

end_time (series__integer)

leverage (series__integer)

initial_capital (series__float)

default_qty_type (series__string)

default_qty_value (series__float)

margin_mode (series__string)

contract_size (series__float)

kis_number (series__integer)

entry_percent (series__float)

close_percent (series__float)

exit_percent (series__float)

log_table (series__table)

fixed_qty (series__float)

fixed_cash (series__float)

real (series__bool)

auto_alert_message (series__bool)

hide_trade_line (series__bool)

LoggerLibLibrary "LoggerLib"

Function Description:

This library aims to extend the logging functionality by overloading various logging methods.

The objective is to enable appending ".log" at the end of different types to make logging outputs easier.

Key features of this function include:

Multi Debug Levels: The readout will encompass error, warning, and info messages.

Controlled Output: Logging can be set for every bar or only the last X bars.

Automatic Logging: Essential variables such as bar_index, time, price, and # of times log has been called can be extracted.

Methods Included:

Logs variables.

Logs floats.

Logs integers.

Logs strings.

Logs booleans.

Logs arrays.

Logs matrices.

Logs maps.

This comprehensive logging function enhances logging capabilities,

providing versatility and ease of use in capturing and debugging data across different contexts.

method log(this, debugLevel, showLast, verbose, showLabels)

Logs any variable type, excluding custom UDTs, and displays to the logs or as a label on bars.

```

// Example

variable = close

variable.log()

variable.log(2, 0,true,true)

// Example Arrays

ArrayVariable = array.from()

ArrayVariable.log()

// Examples Maps

MapVariable = map.new()

MapVariable.log( )

// Example Funky stuff

close.log(debugLevel = 1, showLast = 1, verbose = true, showLabels = true)

```

Namespace types: series float, simple float, input float, const float

Parameters:

this (float) : Variable to be formatted into a logger message

debugLevel (int) : Log Level `1 = log.info | 2 = log.warning 3 = log.error`

showLast (int) : Shows last x Logs, 0 shows all.

verbose (bool) : Include additional Debug logger Data.

showLabels (bool) : Create Labels of the logs on that main chart.

Returns: void

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: series int, simple int, input int, const int

Parameters:

this (int)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: series string, simple string, input string, const string

Parameters:

this (string)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

this (bool)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: series color, simple color, input color, const color

Parameters:

this (color)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: array

Parameters:

this (array)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: array

Parameters:

this (array)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: array

Parameters:

this (array)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: array

Parameters:

this (array)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: map

Parameters:

this (map)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: matrix

Parameters:

this (matrix)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: matrix

Parameters:

this (matrix)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: matrix

Parameters:

this (matrix)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

method log(this, debugLevel, showLast, verbose, showLabels)

Namespace types: matrix

Parameters:

this (matrix)

debugLevel (int)

showLast (int)

verbose (bool)

showLabels (bool)

divergingchartpatternLibrary "divergingchartpattern"

Library having implementation of converging chart patterns

getPatternNameByType(patternType)

Returns pattern name based on type

Parameters:

patternType (int) : integer value representing pattern type

Returns: string name of the pattern

method find(this, sProperties, dProperties, patterns, ohlcArray)

find converging patterns for given zigzag

Namespace types: zg.Zigzag

Parameters:

this (Zigzag type from Trendoscope/ZigzagLite/2) : Current zigzag Object

sProperties (ScanProperties) : ScanProperties Object

dProperties (DrawingProperties type from Trendoscope/abstractchartpatterns/5) : DrawingProperties Object

patterns (array type from Trendoscope/abstractchartpatterns/5) : array of existing patterns to check for duplicates

ohlcArray (array type from Trendoscope/ohlc/1) : array of OHLC values for historical reference

Returns: string name of the pattern

ScanProperties

Object containing properties for pattern scanning

Fields:

baseProperties (ScanProperties type from Trendoscope/abstractchartpatterns/5) : Object of Base Scan Properties

convergingDistanceMultiplier (series float)

booksLibrary "books"

this library contains excerpts from great books to help with trading.

enhiridion()

Fills the map with admonitions from Epictetus' "Enchiridion".

Returns: map with admonitions

CandleInsightsLibrary "CandleInsights"

CandleInsights provides a set of utility functions to facilitate identifying certain types of individual candles and candle patterns.

isBullish()

Returns true if candle is bullish.

Returns: bool

isBearish()

Returns true if candle is bearish.

Returns: bool

isHammer()

Returns true if candle is a hammer. TODO: Allow params

Returns: bool

isShootingStar()

Returns true if candle is a shooting star. TODO: Allow params

Returns: bool

isBearishToppingTail()

Returns true if candle is bearish with a top wick over half the range of the candle. TODO: Allow params

Returns: bool

isHanging()

Returns true if candle is considering a hanging candle (aka hanging man). TODO: Allow params

Returns: bool

isLongBullish(pctChg)

Parameters:

pctChg (float)

isBullishEngulfing()

utilsLibrary "utils"

Provides a set of utility functions for use in strategies or indicators.

colorGreen(opacity)

Parameters:

opacity (int)

colorRed(opacity)

Parameters:

opacity (int)

colorTeal(opacity)

Parameters:

opacity (int)

colorBlue(opacity)

Parameters:

opacity (int)

colorOrange(opacity)

Parameters:

opacity (int)

colorPurple(opacity)

Parameters:

opacity (int)

colorPink(opacity)

Parameters:

opacity (int)

colorYellow(opacity)

Parameters:

opacity (int)

colorWhite(opacity)

Parameters:

opacity (int)

colorBlack(opacity)

Parameters:

opacity (int)

trendChangingUp(emaShort, emaLong)

Signals when the trend is starting to change in a positive direction.

Parameters:

emaShort (float)

emaLong (float)

Returns: bool

trendChangingDown(emaShort, emaLong)

Signals when the trend is starting to change in a negative direction.

Parameters:

emaShort (float)

emaLong (float)

Returns: bool

percentChange(start, end)

Returns the percent change between a start number and end number. A positive change returns a positive value and vice versa.

Parameters:

start (float)

end (float)

Returns: float

percentOf(percent, n)

Returns the number that's the percentage of the provided value.

Parameters:

percent (float) : Use 0.2 for 20 percent, 0.35 for 35 percent, etc.

n (float) : The number to calculate the percentage of.

Returns: float

targetPriceByPercent(percent, n)

Parameters:

percent (float)

n (float)

hasNegativeSlope(start, end)

Parameters:

start (float)

end (float)

timeinrange(resolution, session, timezone)

Returns true when the current time is within a given session window. Note, the time is calculated in the "America/New_York" timezone.

Parameters:

resolution (simple string) : The time interval to use to start/end the background color. Use "1" for the coloring the background up to the minute.

session (simple string) : The session string to use to identify the time window. Example: "0930-1600:23456" means normal market hours on weekdays.

timezone (simple string)

Returns: series bool

barsSinceLastEntry()

Returns the number of bars since the last entry order.

Returns: series int

barsSinceLastExit()

Returns the number of bars since the last exit order.

Returns: series int

calcSlope(ln, lookback)

Calculates the slope of the provided line based on its x,y coordinates in the previous bar to the current bar.

Parameters:

ln (float)

lookback (int)

Returns: series float

openPL()

Returns slope of the line given the start and end x,y coordinates.

Returns: series float

hasConsecutiveNegativeCandles(lookbackInput)

Returns true if the number of consecutive red candles matches the provided count.

Parameters:

lookbackInput (int) : The amount of bars to look back to check for consecutive negative bars. Default = 1.

Returns: series bool

stdevPercent(stdev, price)

Returns the standard deviation as a percentage of price.

Parameters:

stdev (float) : The standard deviation value

price (float) : The current price of the target ticker.

Returns: series float

XXPivotsBreakoutsLibrary "XXPivotsBreakouts"