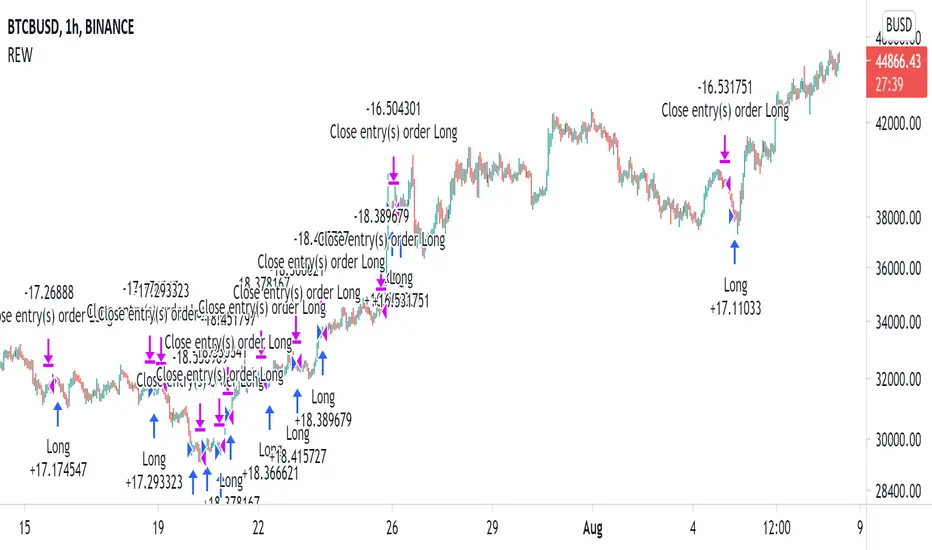

3RSI 3CCI BB 5orders DCA strategy+This strategy is just an attempt to find the indicator values for the trading bot service that I use (link in profile). Due to the use of the “request.security” function in the code, the indicators can be redrawn, but this is not important in history. The strategy used only 5 orders for the "DCA" - bot, located at the same distance in the price overlap range. I only use this strategy when trading in pairs against bitcoin.

Эта стратегия – просто попытка подобрать значения индикаторов для сервиса торговых ботов, который я использую (ссылка в профиле). Из-за использования в коде функции «request.security» возможна перерисовка индикаторов, но на истории это не важно. В стратегии использовано всего 5 ордеров для «DCA» - бота, находящихся на одинаковом расстоянии в диапазоне перекрытия цены. Я использую данную стратегию только при торговле в парах к биткоину.

在腳本中搜尋"bitcoin"

Webhook Starter Kit [HullBuster]

Introduction

This is an open source strategy which provides a framework for webhook enabled projects. It is designed to work out-of-the-box on any instrument triggering on an intraday bar interval. This is a full featured script with an emphasis on actual trading at a brokerage through the TradingView alert mechanism and without requiring browser plugins.

The source code is written in a self documenting style with clearly defined sections. The sections “communicate” with each other through state variables making it easy for the strategy to evolve and improve. This is an excellent place for Pine Language beginners to start their strategy building journey. The script exhibits many Pine Language features which will certainly ad power to your script building abilities.

This script employs a basic trend follow strategy utilizing a forward pyramiding technique. Trend detection is implemented through the use of two higher time frame series. The market entry setup is a Simple Moving Average crossover. Positions exit by passing through conditional take profit logic. The script creates ten indicators including a Zscore oscillator to measure support and resistance levels. The indicator parameters are exposed through 47 strategy inputs segregated into seven sections. All of the inputs are equipped with detailed tool tips to help you get started.

To improve the transition from simulation to execution, strategy.entry and strategy.exit calls show enhanced message text with embedded keywords that are combined with the TradingView placeholders at alert time. Thereby, enabling a single JSON message to generate multiple execution events. This is genius stuff from the Pine Language development team. Really excellent work!

This document provides a sample alert message that can be applied to this script with relatively little modification. Without altering the code, the strategy inputs can alter the behavior to generate thousands of orders or simply a few dozen. It can be applied to crypto, stocks or forex instruments. A good way to look at this script is as a webhook lab that can aid in the development of your own endpoint processor, impress your co-workers and have hours of fun.

By no means is a webhook required or even necessary to benefit from this script. The setups, exits, trend detection, pyramids and DCA algorithms can be easily replaced with more sophisticated versions. The modular design of the script logic allows you to incrementally learn and advance this script into a functional trading system that you can be proud of.

Design

This is a trend following strategy that enters long above the trend line and short below. There are five trend lines that are visible by default but can be turned off in Section 7. Identified, in frequency order, as follows:

1. - EMA in the chart time frame. Intended to track price pressure. Configured in Section 3.

2. - ALMA in the higher time frame specified in Section 2 Signal Line Period.

3. - Linear Regression in the higher time frame specified in Section 2 Signal Line Period.

4. - Linear Regression in the higher time frame specified in Section 2 Signal Line Period.

5. - DEMA in the higher time frame specified in Section 2 Trend Line Period.

The Blue, Green and Orange lines are signal lines are on the same time frame. The time frame selected should be at least five times greater than the chart time frame. The Purple line represents the trend line for which prices above the line suggest a rising market and prices below a falling market. The time frame selected for the trend should be at least five times greater than the signal lines.

Three oscillators are created as follows:

1. Stochastic - In the chart time frame. Used to enter forward pyramids.

2. Stochastic - In the Trend period. Used to detect exit conditions.

3. Zscore - In the Signal period. Used to detect exit conditions.

The Stochastics are configured identically other than the time frame. The period is set in Section 2.

Two Simple Moving Averages provide the trade entry conditions in the form of a crossover. Crossing up is a long entry and down is a short. This is in fact the same setup you get when you select a basic strategy from the Pine editor. The crossovers are configured in Section 3. You can see where the crosses are occurring by enabling Show Entry Regions in Section 7.

The script has the capacity for pyramids and DCA. Forward pyramids are enabled by setting the Pyramid properties tab with a non zero value. In this case add on trades will enter the market on dips above the position open price. This process will continue until the trade exits. Downward pyramids are available in Crypto and Range mode only. In this case add on trades are placed below the entry price in the drawdown space until the stop is hit. To enable downward pyramids set the Pyramid Minimum Span In Section 1 to a non zero value.

This implementation of Dollar Cost Averaging (DCA) triggers off consecutive losses. Each loss in a run increments a sequence number. The position size is increased as a multiple of this sequence. When the position eventually closes at a profit the sequence is reset. DCA is enabled by setting the Maximum DCA Increments In Section 1 to a non zero value.

It should be noted that the pyramid and DCA features are implemented using a rudimentary design and as such do not perform with the precision of my invite only scripts. They are intended as a feature to stress test your webhook endpoint. As is, you will need to buttress the logic for it to be part of an automated trading system. It is for this reason that I did not apply a Martingale algorithm to this pyramid implementation. But, hey, it’s an open source script so there is plenty of room for learning and your own experimentation.

How does it work

The overall behavior of the script is governed by the Trading Mode selection in Section 1. It is the very first input so you should think about what behavior you intend for this strategy at the onset of the configuration. As previously discussed, this script is designed to be a trend follower. The trend being defined as where the purple line is predominately heading. In BiDir mode, SMA crossovers above the purple line will open long positions and crosses below the line will open short. If pyramiding is enabled add on trades will accumulate on dips above the entry price. The value applied to the Minimum Profit input in Section 1 establishes the threshold for a profitable exit. This is not a hard number exit. The conditional exit logic must be satisfied in order to permit the trade to close. This is where the effort put into the indicator calibration is realized. There are four ways the trade can exit at a profit:

1. Natural exit. When the blue line crosses the green line the trade will close. For a long position the blue line must cross under the green line (downward). For a short the blue must cross over the green (upward).

2. Alma / Linear Regression event. The distance the blue line is from the green and the relative speed the cross is experiencing determines this event. The activation thresholds are set in Section 6 and relies on the period and length set in Section 2. A long position will exit on an upward thrust which exceeds the activation threshold. A short will exit on a downward thrust.

3. Exponential event. The distance the yellow line is from the blue and the relative speed the cross is experiencing determines this event. The activation thresholds are set in Section 3 and relies on the period and length set in the same section.

4. Stochastic event. The purple line stochastic is used to measure overbought and over sold levels with regard to position exits. Signal line positions combined with a reading over 80 signals a long profit exit. Similarly, readings below 20 signal a short profit exit.

Another, optional, way to exit a position is by Bale Out. You can enable this feature in Section 1. This is a handy way to reduce the risk when carrying a large pyramid stack. Instead of waiting for the entire position to recover we exit early (bale out) as soon as the profit value has doubled.

There are lots of ways to implement a bale out but the method I used here provides a succinct example. Feel free to improve on it if you like. To see where the Bale Outs occur, enable Show Bale Outs in Section 7. Red labels are rendered below each exit point on the chart.

There are seven selectable Trading Modes available from the drop down in Section 1:

1. Long - Uses the strategy.risk.allow_entry_in to execute long only trades. You will still see shorts on the chart.

2. Short - Uses the strategy.risk.allow_entry_in to execute short only trades. You will still see long trades on the chart.

3. BiDir - This mode is for margin trading with a stop. If a long position was initiated above the trend line and the price has now fallen below the trend, the position will be reversed after the stop is hit. Forward pyramiding is available in this mode if you set the Pyramiding value in the Properties tab. DCA can also be activated.

4. Flip Flop - This is a bidirectional trading mode that automatically reverses on a trend line crossover. This is distinctively different from BiDir since you will get a reversal even without a stop which is advantageous in non-margin trading.

5. Crypto - This mode is for crypto trading where you are buying the coins outright. In this case you likely want to accumulate coins on a crash. Especially, when all the news outlets are talking about the end of Bitcoin and you see nice deep valleys on the chart. Certainly, under these conditions, the market will be well below the purple line. No margin so you can’t go short. Downward pyramids are enabled for Crypto mode when two conditions are met. First the Pyramiding value in the Properties tab must be non zero. Second the Pyramid Minimum Span in Section 1 must be non zero.

6. Range - This is a counter trend trading mode. Longs are entered below the purple trend line and shorts above. Useful when you want to test your webhook in a market where the trend line is bisecting the signal line series. Remember that this strategy is a trend follower. It’s going to get chopped out in a range bound market. By turning on the Range mode you will at least see profitable trades while stuck in the range. However, when the market eventually picks a direction, this mode will sustain losses. This range trading mode is a rudimentary implementation that will need a lot of improvement if you want to create a reliable switch hitter (trend/range combo).

7. No Trade. Useful when setting up the trend lines and the entry and exit is not important.

Once in the trade, long or short, the script tests the exit condition on every bar. If not a profitable exit then it checks if a pyramid is required. As mentioned earlier, the entry setups are quite primitive. Although they can easily be replaced by more sophisticated algorithms, what I really wanted to show is the diminished role of the position entry in the overall life of the trade. Professional traders spend much more time on the management of the trade beyond the market entry. While your trade entry is important, you can get in almost anywhere and still land a profitable exit.

If DCA is enabled, the size of the position will increase in response to consecutive losses. The number of times the position can increase is limited by the number set in Maximum DCA Increments of Section 1. Once the position breaks the losing streak the trade size will return the default quantity set in the Properties tab. It should be noted that the Initial Capital amount set in the Properties tab does not affect the simulation in the same way as a real account. In reality, running out of money will certainly halt trading. In fact, your account would be frozen long before the last penny was committed to a trade. On the other hand, TradingView will keep running the simulation until the current bar even if your funds have been technically depleted.

Entry and exit use the strategy.entry and strategy.exit calls respectfully. The alert_message parameter has special keywords that the endpoint expects to properly calculate position size and message sequence. The alert message will embed these keywords in the JSON object through the {{strategy.order.alert_message}} placeholder. You should use whatever keywords are expected from the endpoint you intend to webhook in to.

Webhook Integration

The TradingView alerts dialog provides a way to connect your script to an external system which could actually execute your trade. This is a fantastic feature that enables you to separate the data feed and technical analysis from the execution and reporting systems. Using this feature it is possible to create a fully automated trading system entirely on the cloud. Of course, there is some work to get it all going in a reliable fashion. Being a strategy type script place holders such as {{strategy.position_size}} can be embedded in the alert message text. There are more than 10 variables which can write internal script values into the message for delivery to the specified endpoint.

Entry and exit use the strategy.entry and strategy.exit calls respectfully. The alert_message parameter has special keywords that my endpoint expects to properly calculate position size and message sequence. The alert message will embed these keywords in the JSON object through the {{strategy.order.alert_message}} placeholder. You should use whatever keywords are expected from the endpoint you intend to webhook in to.

Here is an excerpt of the fields I use in my webhook signal:

"broker_id": "kraken",

"account_id": "XXX XXXX XXXX XXXX",

"symbol_id": "XMRUSD",

"action": "{{strategy.order.action}}",

"strategy": "{{strategy.order.id}}",

"lots": "{{strategy.order.contracts}}",

"price": "{{strategy.order.price}}",

"comment": "{{strategy.order.alert_message}}",

"timestamp": "{{time}}"

Though TradingView does a great job in dispatching your alert this feature does come with a few idiosyncrasies. Namely, a single transaction call in your script may cause multiple transmissions to the endpoint. If you are using placeholders each message describes part of the transaction sequence. A good example is closing a pyramid stack. Although the script makes a single strategy.close() call, the endpoint actually receives a close message for each pyramid trade. The broker, on the other hand, only requires a single close. The incongruity of this situation is exacerbated by the possibility of messages being received out of sequence. Depending on the type of order designated in the message, a close or a reversal. This could have a disastrous effect on your live account. This broker simulator has no idea what is actually going on at your real account. Its just doing the job of running the simulation and sending out the computed results. If your TradingView simulation falls out of alignment with the actual trading account lots of really bad things could happen. Like your script thinks your are currently long but the account is actually short. Reversals from this point forward will always be wrong with no one the wiser. Human intervention will be required to restore congruence. But how does anyone find out this is occurring? In closed systems engineering this is known as entropy. In practice your webhook logic should be robust enough to detect these conditions. Be generous with the placeholder usage and give the webhook code plenty of information to compare states. Both issuer and receiver. Don’t blindly commit incoming signals without verifying system integrity.

Setup

The following steps provide a very brief set of instructions that will get you started on your first configuration. After you’ve gone through the process a couple of times, you won’t need these anymore. It’s really a simple script after all. I have several example configurations that I used to create the performance charts shown. I can share them with you if you like. Of course, if you’ve modified the code then these steps are probably obsolete.

There are 47 inputs divided into seven sections. For the most part, the configuration process is designed to flow from top to bottom. Handy, tool tips are available on every field to help get you through the initial setup.

Step 1. Input the Base Currency and Order Size in the Properties tab. Set the Pyramiding value to zero.

Step 2. Select the Trading Mode you intend to test with from the drop down in Section 1. I usually select No Trade until I’ve setup all of the trend lines, profit and stop levels.

Step 3. Put in your Minimum Profit and Stop Loss in the first section. This is in pips or currency basis points (chart right side scale). Remember that the profit is taken as a conditional exit not a fixed limit. The actual profit taken will almost always be greater than the amount specified. The stop loss, on the other hand, is indeed a hard number which is executed by the TradingView broker simulator when the threshold is breached.

Step 4. Apply the appropriate value to the Tick Scalar field in Section 1. This value is used to remove the pipette from the price. You can enable the Summary Report in Section 7 to see the TradingView minimum tick size of the current chart.

Step 5. Apply the appropriate Price Normalizer value in Section 1. This value is used to normalize the instrument price for differential calculations. Basically, we want to increase the magnitude to significant digits to make the numbers more meaningful in comparisons. Though I have used many normalization techniques, I have always found this method to provide a simple and lightweight solution for less demanding applications. Most of the time the default value will be sufficient. The Tick Scalar and Price Normalizer value work together within a single calculation so changing either will affect all delta result values.

Step 6. Turn on the trend line plots in Section 7. Then configure Section 2. Try to get the plots to show you what’s really happening not what you want to happen. The most important is the purple trend line. Select an interval and length that seem to identify where prices tend to go during non-consolidation periods. Remember that a natural exit is when the blue crosses the green line.

Step 7. Enable Show Event Regions in Section 7. Then adjust Section 6. Blue background fills are spikes and red fills are plunging prices. These measurements should be hard to come by so you should see relatively few fills on the chart if you’ve set this up as intended. Section 6 includes the Zscore oscillator the state of which combines with the signal lines to detect statistically significant price movement. The Zscore is a zero based calculation with positive and negative magnitude readings. You want to input a reasonably large number slightly below the maximum amplitude seen on the chart. Both rise and fall inputs are entered as a positive real number. You can easily use my code to create a separate indicator if you want to see it in action. The default value is sufficient for most configurations.

Step 8. Turn off Show Event Regions and enable Show Entry Regions in Section 7. Then adjust Section 3. This section contains two parts. The entry setup crossovers and EMA events. Adjust the crossovers first. That is the Fast Cross Length and Slow Cross Length. The frequency of your trades will be shown as blue and red fills. There should be a lot. Then turn off Show Event Regions and enable Display EMA Peaks. Adjust all the fields that have the word EMA. This is actually the yellow line on the chart. The blue and red fills should show much less than the crossovers but more than event fills shown in Step 7.

Step 9. Change the Trading Mode to BiDir if you selected No Trades previously. Look on the chart and see where the trades are occurring. Make adjustments to the Minimum Profit and Stop Offset in Section 1 if necessary. Wider profits and stops reduce the trade frequency.

Step 10. Go to Section 4 and 5 and make fine tuning adjustments to the long and short side.

Example Settings

To reproduce the performance shown on the chart please use the following configuration: (Bitcoin on the Kraken exchange)

1. Select XBTUSD Kraken as the chart symbol.

2. On the properties tab set the Order Size to: 0.01 Bitcoin

3. On the properties tab set the Pyramiding to: 12

4. In Section 1: Select “Crypto” for the Trading Model

5. In Section 1: Input 2000 for the Minimum Profit

6. In Section 1: Input 0 for the Stop Offset (No Stop)

7. In Section 1: Input 10 for the Tick Scalar

8. In Section 1: Input 1000 for the Price Normalizer

9. In Section 1: Input 2000 for the Pyramid Minimum Span

10. In Section 1: Check mark the Position Bale Out

11. In Section 2: Input 60 for the Signal Line Period

12. In Section 2: Input 1440 for the Trend Line Period

13. In Section 2: Input 5 for the Fast Alma Length

14. In Section 2: Input 22 for the Fast LinReg Length

15. In Section 2: Input 100 for the Slow LinReg Length

16. In Section 2: Input 90 for the Trend Line Length

17. In Section 2: Input 14 Stochastic Length

18. In Section 3: Input 9 Fast Cross Length

19. In Section 3: Input 24 Slow Cross Length

20. In Section 3: Input 8 Fast EMA Length

21. In Section 3: Input 10 Fast EMA Rise NetChg

22. In Section 3: Input 1 Fast EMA Rise ROC

23. In Section 3: Input 10 Fast EMA Fall NetChg

24. In Section 3: Input 1 Fast EMA Fall ROC

25. In Section 4: Check mark the Long Natural Exit

26. In Section 4: Check mark the Long Signal Exit

27. In Section 4: Check mark the Long Price Event Exit

28. In Section 4: Check mark the Long Stochastic Exit

29. In Section 5: Check mark the Short Natural Exit

30. In Section 5: Check mark the Short Signal Exit

31. In Section 5: Check mark the Short Price Event Exit

32. In Section 5: Check mark the Short Stochastic Exit

33. In Section 6: Input 120 Rise Event NetChg

34. In Section 6: Input 1 Rise Event ROC

35. In Section 6: Input 5 Min Above Zero ZScore

36. In Section 6: Input 120 Fall Event NetChg

37. In Section 6: Input 1 Fall Event ROC

38. In Section 6: Input 5 Min Below Zero ZScore

In this configuration we are trading in long only mode and have enabled downward pyramiding. The purple trend line is based on the day (1440) period. The length is set at 90 days so it’s going to take a while for the trend line to alter course should this symbol decide to node dive for a prolonged amount of time. Your trades will still go long under those circumstances. Since downward accumulation is enabled, your position size will grow on the way down.

The performance example is Bitcoin so we assume the trader is buying coins outright. That being the case we don’t need a stop since we will never receive a margin call. New buy signals will be generated when the price exceeds the magnitude and speed defined by the Event Net Change and Rate of Change.

Feel free to PM me with any questions related to this script. Thank you and happy trading!

CFTC RULE 4.41

These results are based on simulated or hypothetical performance results that have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Also, because these trades have not actually been executed, these results may have under-or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated or hypothetical trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to these being shown.

Random Entries Work!" tHe MaRkEtS aRe RaNdOm ", say moron academics.

The purpose of this study is to show that most markets are NOT random! Most markets show a clear bias where we can make such easy money, that a random number generator can do it.

=== HOW THE INDICATOR WORKS ===

The study will randomly enter the market

The study will randomly exit the market if in a trade

You can choose a Long Only, Short Only, or Bidirectional strategy

=== DEFAULT VALUES AND THEIR LOGIC ===

Percent Chance to Enter Per Bar: 10%

Percent Chance to Exit Per Bar: 3%

Direction: Long Only

Commission: 0

Each bar has a 10% chance to enter the market. Each bar has a 3% to exit the market . It will only enter long.

I included zero commission for simplification. It's a good exercise to include a commission/slippage to see just how much trading fees take from you.

=== TIPS ===

Increasing "Percent Chance to Exit" will shorten the time in a trade. You can see the "Avg # Bars In Trade" go down as you increase. If "Percent Chance to Exit" is too high, the study won't be in the market long enough to catch any movement, possibly exiting on the same bar most of the time.

If you're getting the red screen, that means the strategy lost so much money it went broke. Try reducing the percent equity on the Properties tab.

Switch the start year to avoid/minimize black swan events like the covid drop in 2020.

=== FINDINGS ===

Most markets lose money with a "Random" direction strategy.

Most markets lose ALL money with a "Short Only" strategy.

Most markets make money with a "Long Only" strategy.

Try this strategy on: Bitcoin (BTCUSD) and the NASDAQ (QQQ).

There are two popular memes right now: "Bitcoin to the moon" and "Stocks only go up". Both are seemingly true. Bitcoin was the best performing asset of the 2010's, gaining several billion percent in gains. The stock market is on a 100 year long uptrend. Why? BECAUSE FIAT CURRENCIES ALWAYS GO DOWN! This is inflation. If we measure the market in terms of others assets instead of fiat, the Long Only strategy doesn't work anymore (or works less well).

Try this strategy on: Bitcoin/GLD (BTCUSD/GLD), the Eurodollar (EURUSD), and the S&P 500 measured in gold (SPY/GLD).

Bitcoin measured in gold (BTCUSD/GLD) still works with a Long Only strategy because Bitcoin increased in value over both USD and gold.

The Eurodollar (EURUSD) generally loses money no matter what, especially if you add any commission. This makes sense as they are both fiat currencies with similar inflation schedules.

Gold and the S&P 500 have gained roughly the same amount since ~2000. Some years will show better results for a long strategy, while others will favor a short strategy. Now look at just SPY or GLD (which are both measured in USD by default!) and you'll see the same trend again: a Long Only strategy crushes even when entering and exiting randomly.

=== " JUST TELL ME WHAT TO DO, YOU NERD! " ===

Bulls always win and Bears always lose because fiat currencies go to zero.

You're not underperforming a random number generator, are you?

Buy the Dips (by Coinrule)Taking your first steps into automated trading may be challenging. Coinrule's mission is to make it as easy as possible, also for beginners.

Here follows the best trading strategy to get started with Coinrule. This strategy doesn't involve complex indicators, yet was proved to be effective in the long term for many coins. Results seem to be improved when trading a coin vs Bitcoin.

The strategy buys the dips of a coin to sell with a profit. A stop-loss protects every trade.

Crypto markets offer high volatility and, thus, excellent opportunities for trading. Excluding times of severe downtrend, buying the dip is a simple and effective long-term trading strategy. The buy-signal is set to a 2% drop in a 30-minutes time frame.

Each trade comes with a take profit and a stop loss. Both set at 2%.

You can adjust these percentages to the market volatility as an advanced setup. You can backtest the outcomes using the backtesting tool from Tradingview

The strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Ranged Volume Strategy - evoThis is the strategy version for the ranged volume indicator I published a few days ago.

Long : First yellow break-out after red

Short : First red break-out after yellow

Because this is volume, you want to be using this on an exchange with high volume for the best results. Default settings are not optimized but work great on bitcoins daily chart.

A short explanation of the indicator below:

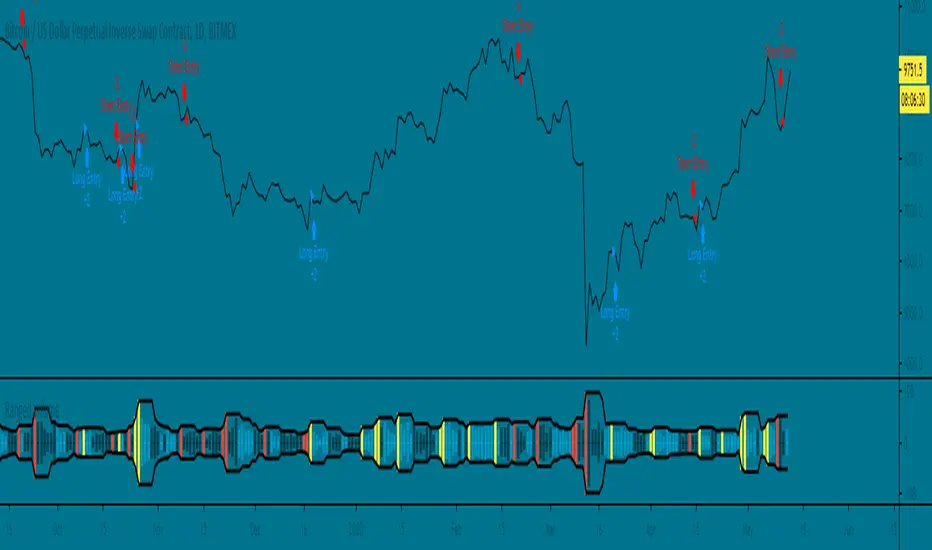

Voss Strategy (Filter + Trend Indicator) [Bitduke]Created strategy based on Voss Predictive Filter, implemented by TradingView user e2e4mfck.

Voss Predictive Filter

This is a relatively new filter from John F. Ehlers’ article, “A Peek Into The Future .” Ehlers describes the calculation of a new filter that could help signal cyclical turning points in markets.

But filter has a negative group delay and while an indicator based on it cannot actually see into the future, it may provide the trader with signals in advance of other indicators.

In mentioned article he tested filter on SPY and at one point in time "it went into a trend mode in January 2019, and the cycle signal failed miserably, signaling a short position during the runup. <...> The only way to minimize the impact of this condition is to employ an additional trend detector."

Thus I've added another Ehlers' based trend based indicator Instantaneous Trendline (thanks to LazyBear for implementation) to minimize the impact of the trend mode and got a good results on XBTUSD pair 4h.

Backtest :

> Range: 2016 - 2020

> XBTUSD

> 4h

> ~20% drawdown

> Sharpe (0.361, not too impressive)

I think it can be improved with Risk Management system and experimenting with various trend following indicators.

Moving Average Strategy of BiznesFilosofWhat is brilliant is simple! Therefore, this strategy works very well. It is configured on bitcoin. But you can use it for other tools. Only need to change the settings.

Remember that this is not a panacea, but only an assistant! You yourself have to choose which entry and exit points to choose.

In more detail about strategy on my channel in YouTube.

===

Что гениально, то просто! Потому, эта стратегия очень хорошо работает. Настроена она на биткоин. Но можно использовать и для других инструментов. Только нужно поменять настройки.

Помните, что это не панацея, а только помощник! Вы сами должны панимать, какие выбирать точки входа и выхода.

Более подробно про стратегию на моём канале в Ютуб.

ALT Risk Strategy with Fear & Greed + ISM PMI📊 Overview

This advanced crypto trading strategy combines multiple macro indicators to identify optimal buy and sell zones for altcoins. It tracks the relationship between altcoin performance versus Bitcoin (ALT/BTC pairs) while incorporating broader market sentiment and economic data to generate risk-adjusted entry and exit signals.

🎯 Core Methodology

Base Risk Metric (65% weight):

MACD Momentum (5%): Normalized trend strength on weekly ALT/BTC pair

RSI (60%): Relative strength indicating overbought/oversold conditions

Price Deviation (35%): Distance from 150-period moving average

Fear & Greed Index (20% weight):

Analyzes market sentiment using multiple factors:

Price momentum and rate of return

Money flow and volume analysis

Volatility metrics (crypto: BVOL24H, traditional: VIX)

Dominance indicators (crypto: BTC.D, traditional: Gold)

Two modes: Crypto-focused or Traditional markets

Customizable smoothing and weighting

US ISM PMI Integration (15% weight):

Manufacturing economic indicator (contraction vs expansion)

PMI < 50 = Economic weakness = Better crypto buying opportunities

PMI > 50 = Economic strength = Risk-on environment

Configurable offset to lead/lag the signal

Daily data smoothed over customizable period

💰 Trading Logic

Tiered Buy System:

Level 1 (Risk < 70): Initial entry with conservative amount

Level 2 (Risk < 50): Double down as risk decreases

Level 3 (Risk < 30): Maximum accumulation at extreme lows

All purchases customizable by dollar amount

Tiered Sell System:

Level 1 (Risk > 70): Take partial profits (default 25%)

Level 2 (Risk > 85): Continue scaling out (default 35%)

Level 3 (Risk > 100): Final exit (default 40%)

Sells reset when new buys occur (can re-accumulate)

⚙️ Key Features

Multi-Asset Support: ETH, SOL, ADA, LINK, UNI, XRP, DOGE, AVAX, MATIC, RENDER, or custom

Exchange Selection: Works with Binance, Coinbase, Kraken, Bitfinex, Bybit

3Commas Integration: Optional webhook alerts for automated bot trading

Visual Risk Zones: Color-coded indicator (green/lime/yellow/orange/red/maroon)

Real-time Info Table: Displays current risk metric, F&G index, PMI value, weights, and position status

Flexible Weighting: Adjust influence of each component (Base/F&G/PMI)

Weekly Timeframe: Reduces noise and focuses on macro trends

📈 Use Cases

DCA Strategy: Dollar-cost averaging with intelligent timing

Swing Trading: Catching major market cycles (weeks to months)

Risk Management: Exit before major downturns, enter during fear

Macro Trading: Align crypto positions with economic conditions

Bot Automation: Connect to 3Commas for hands-free execution

🎓 Credits & Attribution

Original Concept & Base Risk Metric:

Inspired by community-developed ALT/BTC risk oscillators

Fear & Greed methodology adapted from crypto market sentiment research

Enhancements & Integration:

ISM PMI integration and weighting system

Multi-indicator combination framework

Tiered buy/sell logic with reset mechanism

3Commas webhook integration

Development:

Primary Development: Claude AI (Anthropic)

Collaboration & Testing: User feedback and iteration

Pine Script Implementation: TradingView v5

⚠️ Disclaimer

This strategy is for educational and informational purposes only. Past performance does not guarantee future results. Cryptocurrency trading involves substantial risk of loss. Always conduct your own research and consider your risk tolerance before trading. The strategy uses lagging indicators (weekly timeframe) which may not react quickly to sudden market changes.

🔧 Recommended Settings

For better performance than default conservative settings:

Increase buy amounts: Try $50/$75/$100 for more meaningful positions

Adjust thresholds: Consider 40/60/80 for more frequent entries

Test different weights: Experiment with F&G and PMI influence

Optimize for your asset: Different cryptos may require different parameters

Version: 1.0

Last Updated: December 2025

Compatible With: TradingView Pine Script v5

Optimized BTC Mean Reversion (RSI 20/65)📈 Optimized BTC Mean Reversion (RSI 20/65)

Optimized BTC Mean Reversion (RSI 20/65) is a rule-based trading strategy designed to capture mean-reversion moves in strong market structures, primarily optimized for Bitcoin, but adaptable to other liquid cryptocurrencies.

The strategy combines RSI extremes, Stochastic momentum, and EMA trend filtering to identify high-probability reversal zones while maintaining strict risk management.

🔍 Strategy Logic

This system focuses on entering trades when price temporarily deviates from equilibrium, while still respecting the broader trend.

✅ Long Conditions

RSI below 20 (oversold)

Stochastic below 25

Price trading above the 200 EMA (or within a controlled deviation)

Designed to buy sharp pullbacks in bullish conditions

❌ Short Conditions

RSI above 65 (overbought)

Stochastic above 75

Price trading below the 200 EMA

Designed to sell relief rallies in bearish conditions

🛡 Risk Management

Fixed Stop Loss: 4%

Fixed Take Profit: 6%

Risk/Reward: 1 : 1.5

No pyramiding (single position at a time)

Full equity position sizing (adjustable)

All exits are predefined at entry, ensuring consistency and emotional discipline.

📊 Indicators Used

200 EMA – Trend direction filter

RSI (14) – Mean-reversion trigger (20 / 65 levels)

Stochastic Oscillator – Momentum confirmation

👁 Visual Features

EMA plotted directly on chart

Real-time Stop Loss, Take Profit, and Entry Price lines

Clear long/short entry markers

Works on all timeframes (optimized for intraday and swing trading)

🔔 Alerts

Long entry alerts

Short entry alerts

(Perfect for automation or discretionary execution)

⚠️ Disclaimer

This strategy is intended for educational and research purposes only. Past performance does not guarantee future results. Always test on a demo account and adjust risk parameters to your own trading plan.

Gyspy Bot Trade Engine - V1.2B - Strategy 12-7-25 - SignalLynxGypsy Bot Trade Engine (MK6 V1.2B) - Ultimate Strategy & Backtest

Brought to you by Signal Lynx | Automation for the Night-Shift Nation 🌙

1. Executive Summary & Architecture

Gypsy Bot (MK6 V1.2B) is not merely a strategy; it is a massive, modular Trade Engine built specifically for the TradingView Pine Script environment. While most strategies rely on a single dominant indicator (like an RSI cross or a MACD flip) to generate signals, Gypsy Bot functions as a sophisticated Consensus Algorithm.

The engine calculates data from up to 12 distinct Technical Analysis Modules simultaneously on every bar closing. It aggregates these signals into a "Vote Count" and only executes a trade entry when a user-defined threshold of concurring signals is met. This "Voting System" acts as a noise filter, requiring multiple independent mathematical models—ranging from volume flow and momentum to cyclical harmonics and trend strength—to agree on market direction before capital is committed.

Beyond entries, Gypsy Bot features a proprietary Risk Management suite called the Dump Protection Team (DPT). This logic layer operates independently of the entry modules, specifically scanning for "Moon" (Parabolic) or "Nuke" (Crash) volatility events to force-exit positions, overriding standard stops to preserve capital during Black Swan events.

2. ⚠️ The Philosophy of "Curve Fitting" (Must Read)

One must be careful when applying Gypsy Bot to new pairs or charts.

To be fully transparent: Gypsy Bot is, by definition, a very advanced curve-fitting engine. Because it grants the user granular control over 12 modules, dozens of thresholds, and specific voting requirements, it is extremely easy to "over-fit" the data. You can easily toggle switches until the backtest shows a 100% win rate, only to have the strategy fail immediately in live markets because it was tuned to historical noise rather than market structure.

To use this engine successfully, you must adopt a specific optimization mindset:

Ignore Raw Net Profit: Do not tune for the highest dollar amount. A strategy that makes $1M in the backtest but has a 40% drawdown is useless.

Prioritize Stability: Look for a high Profit Factor (1.5+), a high Percent Profitable, and a smooth equity curve.

Regular Maintenance is Mandatory: Markets shift regimes (e.g., from Bull Trend to Crab Range). Parameters that worked perfectly in 2021 may fail in 2024. Gypsy Bot settings should be reviewed and adjusted at regular intervals (e.g., quarterly) to ensure the voting logic remains aligned with current market volatility.

Timeframe Recommendations:

Gypsy Bot is optimized for High Time Frame (HTF) trend following. It generally produces the most reliable results on charts ranging from 1-Hour to 12-Hours, with the 4-Hour timeframe historically serving as the "sweet spot" for most major cryptocurrency assets.

3. The Voting Mechanism: How Entries Are Generated

The heart of the Gypsy Bot engine is the ActivateOrders input (found in the "Order Signal Modifier" settings).

The engine constantly monitors the output of all enabled Modules.

Long Votes: GoLongCount

Short Votes: GoShortCount

If you have 10 Modules enabled, and you set ActivateOrders to 7:

The engine will ONLY trigger a Buy Entry if 7 or more modules return a valid "Buy" signal on the same closed candle.

If only 6 modules agree, the trade is rejected.

This allows you to mix "Leading" indicators (Oscillators) with "Lagging" indicators (Moving Averages) to create a high-probability entry signal that requires momentum, volume, and trend to all be in alignment.

4. Technical Deep Dive: The 12 Modules

Gypsy Bot allows you to toggle the following modules On/Off individually to suit the asset you are trading.

Module 1: Modified Slope Angle (MSA)

Logic: Calculates the geometric angle of a moving average relative to the timeline.

Function: It filters out "lazy" trends. A trend is only considered valid if the slope exceeds a specific steepness threshold. This helps avoid entering trades during weak drifts that often precede a reversal.

Module 2: Correlation Trend Indicator (CTI)

Logic: Based on John Ehlers' work, this measures how closely the current price action correlates to a straight line (a perfect trend).

Function: It outputs a confidence score (-1 to 1). Gypsy Bot uses this to ensure that we are not just moving up, but moving up with high statistical correlation, reducing fake-outs.

Module 3: Ehlers Roofing Filter

Logic: A sophisticated spectral filter that combines a High-Pass filter (to remove long-term drift) with a Super Smoother (to remove high-frequency noise).

Function: It attempts to isolate the "Roof" of the price action. It is excellent at catching cyclical turning points before standard moving averages react.

Module 4: Forecast Oscillator

Logic: Uses Linear Regression forecasting to predict where price "should" be relative to where it is.

Function: When the Forecast Oscillator crosses its zero line, it indicates that the regression trend has flipped. We offer both "Aggressive" and "Conservative" calculation modes for this module.

Module 5: Chandelier ATR Stop

Logic: A volatility-based trend follower that hangs a "leash" (ATR multiple) from the highest high (for longs) or lowest low (for shorts).

Function: Used here as an entry filter. If price is above the Chandelier line, the trend is Bullish. It also includes a "Bull/Bear Qualifier" check to ensure structural support.

Module 6: Crypto Market Breadth (CMB)

Logic: This is a macro-filter. It pulls data from multiple major tickers (BTC, ETH, and Perpetual Contracts) across different exchanges.

Function: It calculates a "Market Health" percentage. If Bitcoin is rising but the rest of the market is dumping, this module can veto a trade, ensuring you don't buy into a "fake" rally driven by a single asset.

Module 7: Directional Index Convergence (DIC)

Logic: Analyzes the convergence/divergence between Fast and Slow Directional Movement indices.

Function: Identifies when trend strength is expanding. A buy signal is generated only when the positive directional movement overpowers the negative movement with expanding momentum.

Module 8: Market Thrust Indicator (MTI)

Logic: A volume-weighted breadth indicator. It uses Advance/Decline data and Up/Down Volume data.

Function: This is one of the most powerful modules. It confirms that price movement is supported by actual volume flow. We recommend using the "SSMA" (Super Smoother) MA Type for the cleanest signals on the 4H chart.

Module 9: Simple Ichimoku Cloud

Logic: Traditional Japanese trend analysis using the Tenkan-sen and Kijun-sen.

Function: Checks for a "Kumo Breakout." Price must be fully above the Cloud (for longs) or below it (for shorts). This is a classic "trend confirmation" module.

Module 10: Simple Harmonic Oscillator

Logic: Analyzes the harmonic wave properties of price action to detect cyclical tops and bottoms.

Function: Serves as a counter-trend or early-reversal detector. It tries to identify when a cycle has bottomed out (for buys) or topped out (for sells) before the main trend indicators catch up.

Module 11: HSRS Compression / Super AO

Logic: Two options in one.

HSRS: Hirashima Sugita Resistance Support. Detects volatility compression (squeezes) relative to dynamic support/resistance bands.

Super AO: A combination of the Awesome Oscillator and SuperTrend logic.

Function: Great for catching explosive moves that result from periods of low volatility (consolidation).

Module 12: Fisher Transform (MTF)

Logic: Converts price data into a Gaussian normal distribution.

Function: Identifies extreme price deviations. This module uses Multi-Timeframe (MTF) logic to look at higher-timeframe trends (e.g., looking at the Daily Fisher while trading the 4H chart) to ensure you aren't trading against the major trend.

5. Global Inhibitors (The Veto Power)

Even if 12 out of 12 modules vote "Buy," Gypsy Bot performs a final safety check using Global Inhibitors. If any of these are triggered, the trade is blocked.

Bitcoin Halving Logic:

Hardcoded dates for past and projected future Bitcoin halvings (up to 2040).

Trading is inhibited or restricted during the chaotic weeks immediately surrounding a Halving event to avoid volatility crushes.

Miner Capitulation:

Uses Hash Rate Ribbons (Moving averages of Hash Rate).

If miners are capitulating (Shutting down rigs due to unprofitability), the engine flags a "Bearish" regime and can flip logic to Short-only or flat.

ADX Filter (Flat Market Protocol):

If the Average Directional Index (ADX) is below a specific threshold (e.g., 20), the market is deemed "Flat/Choppy." The bot will refuse to open trend-following trades in a flat market.

CryptoCap Trend:

Checks the total Crypto Market Cap chart. If the broad market is in a downtrend, it can inhibit Long entries on individual altcoins.

6. Risk Management & The Dump Protection Team (DPT)

Gypsy Bot separates "Entry Logic" from "Risk Management Logic."

Dump Protection Team (DPT)

This is a specialized logic branch designed to save the account during Black Swan events.

Nuke Protection: If the DPT detects a volatility signature consistent with a flash crash, it overrides all other logic and forces an immediate exit.

Moon Protection: If a parabolic pump is detected that violates statistical probability (Bollinger deviations), DPT can force a profit take before the inevitable correction.

Advanced Adaptive Trailing Stop (AATS)

Unlike a static trailing stop (e.g., "trail by 5%"), AATS is dynamic.

Penthouse Level: If price is at the top of the HSRS channel (High Volatility), the stop loosens to allow for wicks.

Dungeon Level: If price is compressed at the bottom, the stop tightens to protect capital.

Staged Take Profits

TP1: Scalp a portion (e.g., 10%) to cover fees and secure a win.

TP2: Take the bulk of profit.

TP3: Leave a "Runner" position with a loose trailing stop to catch "Moon" moves.

7. Recommended Setup Guide

When applying Gypsy Bot to a new chart, follow this sequence:

Set Timeframe: 4 Hours (4H).

Reset: Turn OFF Trailing Stop, Stop Loss, and Take Profits. (We want to see raw entry performance first).

Tune DPT: Adjust "Dump/Moon Protection" inputs first. These have the highest impact on net performance.

Tune Module 8 (MTI): This module is a heavy filter. Experiment with the MA Type (SSMA is recommended).

Select Modules: Enable/Disable modules 1-12 based on the asset's personality (Trending vs. Ranging).

Voting Threshold: Adjust ActivateOrders. A lower number = More Trades (Aggressive). A higher number = Fewer, higher conviction trades (Conservative).

Final Polish: Re-enable Stop Losses, Trailing Stops, and Staged Take Profits to smooth the equity curve and define your max risk per trade.

8. Technical Specs

Engine Version: Pine Script V6

Repainting: This strategy uses Closed Candle data for all Risk Management and Entry decisions. This ensures that Backtest results align closely with real-time behavior (no repainting of historical signals).

Alerts: This script generates Strategy alerts. If you require visual-only alerts, see the source code header for instructions on switching to "Study" (Indicator) mode.

Disclaimer:

This script is a complex algorithmic tool for market analysis. Past performance is not indicative of future results. Use this tool to assist your own decision-making, not to replace it.

9. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

BTC Dynamic Volatility Trend Backtested from 2017 to present, this strategy has delivered a staggering 7100%+ cumulative return. It doesn't just track the market; it dominates it. By capturing major trends and strictly limiting drawdowns, it has significantly outperformed the standard 'Buy & Hold' BTC strategy, proving its ability to generate massive alpha across multiple bull and bear cycles.

自 2017 年至今,本策略实现了惊人的 7100%+ 累计收益率。它不仅仅是跟随市场,更是超越了市场。通过精准捕捉主升浪并严格控制回撤,该策略在穿越多轮牛熊周期后,大幅度跑赢了比特币‘买入持有’(Buy & Hold)的基准收益,展现了极致的阿尔法(Alpha)捕捉能力。"

Introduction :Simplicity is the ultimate sophistication. This strategy is designed specifically for Bitcoin (BTC), capturing its unique characteristics: high volatility, frequent fakeouts, and massive trend persistence. It abandons complex indicators in favor of a robust logic: "Follow the Trend, Filter the Noise, Let Profits Run."

Core Logic

Trend Filter (Fibonacci EMA 144): We use the 144-period Exponential Moving Average as the baseline. Longs are only taken above this line, and shorts only below. This keeps you on the right side of the major trend.

Volatility Breakout (Donchian Channel 20): Entries are triggered only when price breaks the 20-day high (for longs) or low (for shorts). This confirms momentum and avoids trading in chop.

Dynamic Risk Management (ATR Chandelier Exit):

Instead of fixed % stops, we use Average True Range (ATR) to calculate stop losses.

The Ratchet Mechanism: The stop loss moves up with the price but never moves down (for longs). This locks in profits automatically as the trend develops and exits immediately when volatility turns against you.

Why Use This Strategy?

Zero Repainting: All signals are confirmed.

No Curve Fitting: Uses classic parameters (144, 20) that have worked for decades.

Mental Peace: The strategy handles the exit. You don't need to guess where to sell. It holds through minor corrections and exits only when the trend truly reverses.

Settings

Leverage %: Adjust your position size based on equity (default 100% = 1x).

Timeframe: Recommended for 4H charts.

中文版 (Chinese Version)

简介 :大道至简。本策略专为 比特币 (BTC) 设计,针对其高波动、假突破多但趋势爆发力强的特点,摒弃了复杂的过度拟合指标,回归交易本质:“顺大势,滤噪音,截断亏损,让利润奔跑”。

核心逻辑

趋势过滤器 (斐波那契 EMA 144): 使用 144 周期指数移动平均线作为多空分水岭。价格在均线之上只做多,之下只做空。这能有效过滤掉大部分震荡市的噪音。

波动率突破 (唐奇安通道 20): 只有当价格突破过去 20 根 K 线的最高价(做多)或最低价(做空)时才进场。这确保了我们只在趋势确立的瞬间入场。

动态风控 (ATR 吊灯止损):

拒绝固定点数止损,使用 ATR(平均真实波幅)根据市场热度动态计算安全距离。

棘轮机制: 止损线会跟随价格上涨而上移,但绝不会下移(做多时)。这实现了自动化的“利润锁定”,既能扛住正常的波动回调,又能在大势反转时果断离场。

策略优势

绝不重绘: 所有信号均为收盘确认或实时触价。

拒绝拟合: 使用经过数十年市场验证的经典参数组合。

心态管理: 策略全自动管理出场。你不需要纠结何时止盈,它会帮你吃到完整的鱼身,直到趋势结束。

使用建议

资金管理: 可通过参数调整仓位占比(默认 100% = 1倍杠杆)。

推荐周期: 建议在4小时 图表上运行效果最佳。

Estrategia Trend Following: 52w/26w BreakoutThis is a classic long-term Trend Following strategy, heavily inspired by the Donchian Channel system and the legendary "Turtle Trading" rules. It is designed to capture major market moves (bull runs) while filtering out short-term market noise and volatility.

This script is ideal for investors and swing traders who prefer a "hands-off" approach, looking to catch large trends rather than day-trading small fluctuations.

How it Works:

1. Entry Condition (The Breakout):

52-Week High: The strategy enters a Long position when the price breaks above the highest high of the last 252 trading days (approx. 1 year).

SuperTrend Filter: An additional filter using the SuperTrend indicator ensures that the breakout is supported by positive momentum, helping to reduce false signals during choppy lateral markets.

2. Exit Condition (The Trailing Stop):

26-Week Low: The strategy ignores short-term corrections. It only closes the position if the price closes below the lowest low of the last 126 trading days (approx. 6 months).

This wide stop allows the trade to "breathe" and stay open during significant pullbacks, ensuring you stay in the trend for as long as possible.

Features & Settings:

Customizable Lookback Periods: You can adjust the Entry (default 252 days) and Exit (default 126 days) periods in the settings menu.

Visual Aids:

Blue Line: Represents the 1-Year High (Entry Threshold).

Red Line: Represents the 6-Month Low (Dynamic Stop Loss).

Channel Shading: Visualizes the trading range between the high and low.

Labels: Clearly marks "BUY" and "EXIT" points on the chart.

Recommended Usage:

Timeframe: Daily (1D). This logic is designed for daily candles.

Assets: Works best on assets with strong trending characteristics (e.g., Bitcoin/Crypto, Tech Stocks, Indices like SPX/NDX, and Commodities).

Patience Required: This strategy generates very few signals. It may stay quiet for months and then hold a position for over a year.

BTC Mon 8am Buy / Wed 2pm Sell (NY Time, Daily + Intraday)This strategy implements a fixed weekly time-based trading schedule for Bitcoin, using New York market hours as the reference clock. It is designed to test whether a consistent pattern exists between early-week accumulation and mid-week distribution in BTC price behavior.

Entry Rule — Monday 8:00 AM (NY Time)

The strategy enters a long position every Monday at exactly 08:00 AM Eastern Time, one hour after the U.S. equities market pre-open activity begins influencing global liquidity.

This timing attempts to capture early-week directional moves in Bitcoin, which sometimes occur as traditional markets come online.

Exit Rule — Wednesday 2:00 PM (NY Time)

The strategy closes the position every Wednesday at 2:00 PM Eastern Time, a point in the week where:

U.S. equity markets are still open

BTC often experiences mid-week volatility rotations

Liquidity is generally high

This exit removes exposure before later-week uncertainty and gives a consistent, measurable time window for each trade.

Timeframe Compatibility

Works on intraday charts (recommended 1h or lower) using precise time-based triggers.

Also runs on daily charts, where entries and exits occur on the Monday and Wednesday bars respectively (daily charts cannot show intraday timestamps).

All timestamps are synced to America/New_York regardless of the exchange’s native timezone.

Trading Frequency

Exactly one trade per week, preventing overtrading and allowing comparison of weekly performance across years of historical BTC price data.

Purpose of the Strategy

This is not a value-based or trend-following system, but a behavioral/time-cycle analysis tool.

It helps evaluate whether a repeating short-term edge exists based solely on:

Weekday timing

Liquidity cycles

Institutional market influence

BTC’s habitual early-week momentum patterns

It is ideal for:

Backtesting weekly BTC behavior

Studying time-based edges

Comparing alternative weekday/time combinations

Visualizing weekly P&L structure

Risk Notes

This strategy does not attempt to predict price direction and should not be assumed profitable without robust backtesting.

Time-based edges can appear, disappear, or invert depending on macro conditions.

There is no stop loss or risk management included by default, so the strategy reflects raw timing-based performance.

Superior-Range Bound Renko - Strategy - 11-29-25 - SignalLynxSuperior-Range Bound Renko Strategy with Advanced Risk Management Template

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

Welcome to Superior-Range Bound Renko (RBR) — a volatility-aware, structure-respecting swing-trading system built on top of a full Risk Management (RM) Template from Signal Lynx.

Instead of relying on static lookbacks (like “14-period RSI”) or plain MA crosses, Superior RBR:

Adapts its range definition to market volatility in real time

Emulates Renko Bricks on a standard, time-based chart (no Renko chart type required)

Uses a stack of Laguerre Filters to detect genuine impulse vs. noise

Adds an Adaptive SuperTrend powered by a small k-means-style clustering routine on volatility

Under the hood, this script also includes the full Signal Lynx Risk Management Engine:

A state machine that separates “Signal” from “Execution”

Layered exit tools: Stop Loss, Trailing Stop, Staged Take Profit, Advanced Adaptive Trailing Stop (AATS), and an RSI-style stop (RSIS)

Designed for non-repainting behavior on closed candles by basing execution-critical logic on previous-bar data

We are publishing this as an open-source template so traders and developers can leverage a professional-grade RM engine while integrating their own signal logic if they wish.

2. Quick Action Guide (TL;DR)

Best Timeframe:

4 Hours (H4) and above. This is a high-conviction swing-trading system, not a scalper.

Best Assets:

Volatile instruments that still respect market structure:

Bitcoin, Ethereum, Gold (XAUUSD), high-volatility Forex pairs (e.g., GBPJPY), indices with clean ranges.

Strategy Type:

Volatility-Adaptive Trend Following + Impulse Detection.

It hunts for genuine expansion out of ranges, not tiny mean-reversion nibbles.

Key Feature:

Renko Emulation on time-based candles.

We mathematically model Renko Bricks and overlay them on your standard chart to define:

“Equilibrium” zones (inside the brick structure)

“Breakout / impulse” zones (when price AND the impulse line depart from the bricks)

Repainting:

Designed to be non-repainting on closed candles.

All RM execution logic uses confirmed historical data (no future bars, no security() lookahead). Intrabar flicker during formation is allowed, but once a bar closes the engine’s decisions are stable.

Core Toggles & Filters:

Enable Longs and Shorts independently

Optional Weekend filter (block trades on Saturday/Sunday)

Per-module toggles: Stop Loss, Trailing Stop, Staged Take Profits, AATS, RSIS

3. Detailed Report: How It Works

A. The Strategy Logic: Superior RBR

Superior RBR builds its entry signal from multiple mathematical layers working together.

1) Adaptive Lookback (Volatility Normalization)

Instead of a fixed 100-bar or 200-bar range, the script:

Computes ATR-based volatility over a user-defined period.

Normalizes that volatility relative to its recent min/max.

Maps the normalized value into a dynamic lookback window between a minimum and maximum (e.g., 4 to 100 bars).

High Volatility:

The lookback shrinks, so the system reacts faster to explosive moves.

Low Volatility:

The lookback expands, so the system sees a “bigger picture” and filters out chop.

All the core “Range High/Low” and “Range Close High/Low” boundaries are built on top of this adaptive window.

2) Range Construction & Quick Ranges

The engine constructs several nested ranges:

Outer Range:

rangeHighFinal – dynamic highest high

rangeLowFinal – dynamic lowest low

Inner Close Range:

rangeCloseHighFinal – highest close

rangeCloseLowFinal – lowest close

Quick Ranges:

“Half-length” variants of those, used to detect more responsive changes in structure and volatility.

These ranges define:

The macro box price is trading inside

Shorter-term “pressure zones” where price is coiling before expansion

3) Renko Emulation (The Bricks)

Rather than using the Renko chart type (which discards time), this script emulates Renko behavior on your normal candles:

A “brick size” is defined either:

As a standard percentage move, or

As a volatility-driven (ATR) brick, optionally inhibited by a minimum standard size

The engine tracks a base value and derives:

brickUpper – top of the emulated brick

brickLower – bottom of the emulated brick

When price moves sufficiently beyond those levels, the brick “shifts”, and the directional memory (renkoDir) updates:

renkoDir = +2 when bricks are advancing upward

renkoDir = -2 when bricks are stepping downward

You can think of this as a synthetic Renko tape overlaid on time-based candles:

Inside the brick: equilibrium / consolidation

Breaking away from the brick: momentum / expansion

4) Impulse Tracking with Laguerre Filters

The script uses multiple Laguerre Filters to smooth price and brick-derived data without traditional lag.

Key filters include:

LagF_1 / LagF_W: Based on brick upper/lower baselines

LagF_Q: Based on HLCC4 (high + low + 2×close)/4

LagF_Y / LagF_P: Complex averages combining brick structures and range averages

LagF_V (Primary Impulse Line):

A smooth, high-level impulse line derived from a blend of the above plus the outer ranges

Conceptually:

When the impulse line pushes away from the brick structure and continues in one direction, an impulse move is underway.

When its direction flips and begins to roll over, the impulse is fading, hinting at mean reversion back into the range.

5) Fib-Based Structure & Swaps

The system also layers in Fib levels derived from the adaptive ranges:

Standard levels (12%, 23.6%, 38.2%, 50%, 61%, 76.8%, 88%) from the main range

A secondary “swap” set derived from close-range dynamics (fib12Swap, fib23Swap, etc.)

These Fibs are used to:

Bucket price into structural zones (below 12, between 23–38, etc.)

Detect breakouts when price and Laguerre move beyond key Fib thresholds

Drive zSwap logic (where a secondary Fib set becomes the active structure once certain conditions are met)

6) Adaptive SuperTrend with K-Means-Style Volatility Clustering

Under the hood, the script uses a small k-means-style clustering routine on ATR:

ATR is measured over a fixed period

The range of ATR values is split into Low, Medium, High volatility centroids

Current ATR is assigned to the nearest centroid (cluster)

From that, a SuperTrend variant (STK) is computed with dynamic sensitivity:

In quiet markets, SuperTrend can afford to be tighter

In wild markets, it widens appropriately to avoid constant whipsaw

This SuperTrend-based oscillator (LagF_K and its signals) is then combined with the brick and Laguerre stack to confirm valid trend regimes.

7) Final Baseline Signals (+2 / -2)

The “brain” of Superior RBR lives in the Baseline & Signal Generation block:

Two composite signals are built: B1 and B2:

They combine:

Fib breakouts

Renko direction (renkoDir)

Expansion direction (expansionQuickDir)

Multiple Laguerre alignments (LagF_Q, LagF_W, LagF_Y, LagF_Z, LagF_P, LagF_V)

They also factor in whether Fib structures are expanding or contracting.

A user toggle selects the “Baseline” signal:

finalSig = B2 (default) or B1 (alternate baseline)

finalSig is then filtered through the RM state machine and only when everything aligns, we emit:

+2 = Long / Buy signal

-2 = Short / Sell signal

0 = No new trade

Those +2 / -2 values are what feed the Risk Management Engine.

B. The Risk Management (RM) Engine

This script features the Signal Lynx Risk Management Engine, a proprietary state machine built to separate Signal from Execution.

Instead of firing orders directly on indicator conditions, we:

Convert the raw signal into a clean integer (Fin = +2 / -2 / 0)

Feed it into a Trade State Machine that understands:

Are we flat?

Are we in a long or short?

Are we in a closing sequence?

Should we permit re-entry now or wait?

Logic Injection / Template Concept:

The RM engine expects a simple integer:

+2 → Buy

-2 → Sell

Everything else (0) is “no new trade”

This makes the script a template:

You can remove the Superior RBR block

Drop in your own logic (RSI, MACD, price action, etc.)

As long as you output +2 or -2 into the same signal channel, the RM engine can drive all exits and state transitions.

Aggressive vs Conservative Modes:

The input AgressiveRM (Aggressive RM) governs how we interpret signals:

Conservative Mode (Aggressive RM = false):

Uses a more filtered internal signal (AF) to open trades

Effectively waits for a clean trend flip / confirmation before new entries

Minimizes whipsaw at the cost of fewer trades

Aggressive Mode (Aggressive RM = true):

Reacts directly to the fresh alert (AO) pulses

Allows faster re-entries in the same direction after RM-based exits

Still respects your pyramiding setting; this script ships with pyramiding = 0 by default, so it will not stack multiple positions unless you change that parameter in the strategy() call.

The state machine enforces discipline on top of your signal logic, reducing double-fires and signal spam.

C. Advanced Exit Protocols (Layered Defense)

The exit side is where this template really shines. Instead of a single “take profit or stop loss,” it uses multiple, cooperating layers.

1) Hard Stop Loss

A classic percentage-based Stop Loss (SL) relative to the entry price.

Acts as a final “catastrophic protection” layer for unexpected moves.

2) Standard Trailing Stop

A percentage-based Trailing Stop (TS) that:

Activates only after price has moved a certain percentage in your favor (tsActivation)

Then trails price by a configurable percentage (ts)

This is a straightforward, battle-tested trailing mechanism.

3) Staged Take Profits (Three Levels)

The script supports three staged Take Profit levels (TP1, TP2, TP3):

Each stage has:

Activation percentage (how far price must move in your favor)

Trailing amount for that stage

Position percentage to close

Example setup:

TP1:

Activate at +10%

Trailing 5%

Close 10% of the position

TP2:

Activate at +20%

Trailing 10%

Close another 10%

TP3:

Activate at +30%

Trailing 5%

Close the remaining 80% (“runner”)

You can tailor these quantities for partial scaling out vs. letting a core position ride.

4) Advanced Adaptive Trailing Stop (AATS)

AATS is a sophisticated volatility- and structure-aware stop:

Uses Hirashima Sugita style levels (HSRS) to model “floors” and “ceilings” of price:

Dungeon → Lower floors → Mid → Upper floors → Penthouse

These levels classify where current price sits within a long-term distribution.

Combines HSRS with Bollinger-style envelopes and EMAs to determine:

Is price extended far into the upper structure?

Is it compressed near the lower ranges?

From this, it computes an adaptive factor that controls how tight or loose the trailing level (aATS / bATS) should be:

High Volatility / Penthouse areas:

Stop loosens to avoid getting wicked out by inevitable spikes.

Low Volatility / compressed structure:

Stop tightens to lock in and protect profit.

AATS is designed to be the “smart last line” that responds to context instead of a single fixed percentage.

5) RSI-Style Stop (RSIS)

On top of AATS, the script includes a RSI-like regime filter:

A McGinley Dynamic mean of price plus ATR bands creates a dynamic channel.

Crosses above the top band and below the lower band change a directional state.

When enabled (UseRSIS):

RSIS can confirm or veto AATS closes:

For longs: A shift to bearish RSIS can force exits sooner.

For shorts: A shift to bullish RSIS can do the same.

This extra layer helps avoid over-reactive stops in strong trends while still respecting a regime change when it happens.

D. Repainting Protection

Many strategies look incredible in the Strategy Tester but fail in live trading because they rely on intrabar values or future-knowledge functions.

This template is built with closed-candle realism in mind:

The Risk Management logic explicitly uses previous bar data (open , high , low , close ) for the key decisions on:

Trailing stop updates

TP triggers

SL hits

RM state transitions

No security() lookahead or future-bar access is used.

This means:

Backtest behavior is designed to match what you can actually get with TradingView alerts and live automation.

Signals may “flicker” intrabar while the candle is forming (as with any strategy), but on closed candles, the RM decisions are stable and non-repainting.

4. For Developers & Modders

We strongly encourage you to mod this script.

To plug your own strategy into the RM engine:

Look for the section titled:

// BASELINE & SIGNAL GENERATION

You will see composite logic building B1 and B2, and then selecting:

baseSig = B2

altSig = B1

finalSig = sigSwap ? baseSig : altSig

You can replace the content used to generate baseSig / altSig with your own logic, for example:

RSI crosses

MACD histogram flips

Candle pattern detectors

External condition flags

Requirements are simple:

Your final logic must output:

2 → Buy signal

-2 → Sell signal

0 → No new trade

That output flows into the RM engine via finalSig → AlertOpen → state machine → Fin.

Once you wire your signals into finalSig, the entire Risk Management system (Stops, TPs, AATS, RSIS, re-entry logic, weekend filters, long/short toggles) becomes available for your custom strategy without re-inventing the wheel.

This makes Superior RBR not just a strategy, but a reference architecture for serious Pine dev work.

5. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

BTC BRD – Bullet-Proof Reversal StrategyBTC BRD – Bullet-Proof Reversal Strategy is a price-action based reversal system that turns your existing “Bullet-Proof Reversal Detector” into a fully backtestable TradingView strategy with built-in risk management. It is designed to catch clean swing reversals using pure market structure, then automatically place stop-loss and take-profit orders based on your preferred risk-reward settings.

## Core concept

The strategy identifies true swing highs and lows using pivots and then waits for a clear market structure shift before entering any trade. It looks for a higher low followed by a break of structure for longs, and a lower high followed by a break of structure for shorts, helping filter out many random spikes and fakeouts. This makes it suitable for traders who prefer clean, rule-based entries grounded in market structure rather than noisy, indicator-heavy setups.

## Entries and exits

- Long trades are triggered after a bullish higher-low plus a confirmed break above the last swing high.

- Short trades are triggered after a bearish lower-high plus a confirmed break below the last swing low.

- Every position is protected with an automatic stop-loss and a calculated take-profit, so each trade has a predefined risk and reward from the moment it is opened.

## Risk management

The strategy lets you control your risk with a configurable risk-reward ratio (RR) and flexible stop-loss options. You can choose between an ATR-based stop (ATR × multiplier) or a fixed percentage stop relative to the entry price. Once the stop distance is known, the take-profit level is automatically derived from your RR value, making trade sizing and evaluation more consistent across different pairs and timeframes.

## Use cases and recommendations

This script is ideal for swing and intraday traders who want to systematically test market-structure reversals on assets like Bitcoin or other volatile instruments. For best results, experiment with different timeframes and ATR/percentage settings, and always validate performance using the Strategy Tester before deploying it on live markets. Remember that no strategy is guaranteed to be profitable, so use proper risk management and adapt settings to your own style and risk tolerance.

Stratégie SMC V18.2 (BTC/EUR FINAL R3 - Tendance)This strategy is an automated implementation of Smart Money Concepts (SMC), designed to operate on the Bitcoin/Euro (BTC/EUR) chart using the 15-minute Timeframe (M15).It focuses on identifying high-probability zones (Order Blocks) after a confirmed Break of Structure (BOS) and a Liquidity Sweep, utilizing an H1/EMA 200 trend filter to only execute trades in the direction of the dominant market flow.Risk management is strict: every trade uses a fixed Risk-to-Reward Ratio (R:R) of 1:3.🧱 Core Logic Components

1. Trend Filter (H1/EMA 200)Objective: To avoid counter-trend entries, which has allowed the success rate to increase to nearly $65\%$ in backtests.Mechanism: A $200$-period EMA is plotted on a higher timeframe (Default: H1/60 minutes).Long (Buy): Entry is only permitted if the current price (M15) is above the trend EMA.Short (Sell): Entry is only permitted if the current price (M15) is below the trend EMA.

2. Order Block (OB) DetectionA potential Order Block is identified on the previous candle if it is

accompanied by an inefficiency (FVG - Fair Value Gap).

3. Advanced SMC ValidationBOS (Break of Structure): A recent BOS must be confirmed by breaking the swing high/low defined by the swing length (Default: 4 M15 candles).Liquidity (Liquidity Sweep): The Order Block zone must have swept recent liquidity (defined by the Liquidity Search Length) within a certain tolerance (Default: $0.1\%$).Point of Interest: The OB must form in a premium zone (for shorts) or a discount zone (for longs) relative to the current swing range (above or below the $50\%$ level of the range).

4. Execution and Risk ManagementEntry: The trade is triggered when the price touches the active Order Block (mitigation).Stop Loss (SL): The SL is fixed at the low of the OB (for longs) or the high of the OB (for shorts).Take Profit (TP): The TP is strictly set at a level corresponding to 3 times the SL distance (R:R 1:3).Lot Sizing: The trade quantity is calculated to risk a fixed amount (Default: 2.00 Euros) per transaction, capped by a Lot Max and Lot Min defined by the user.