Straddle / strangle buy or sell indicatorStraddle / strangle buy or sell indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Buy or sell (the strategy)

- Straddle/strangle price bought/sold: enter the price that you bought/sold one options strategy.

-Instrument price when bought/sold: the stock price when you bought/sold the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-Risk to reward: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (3).

Example: If the strategy was bought, -0.95 means, 95% of the options strategy value is lost (unrealized). If the strategy was bought, 3 means, the risk to reward is 3.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

在腳本中搜尋"implied"

Call Bear Spread indicatorCall bear spread indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a CREDIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

- Call spread price (Credit): The credit received for one unit of options strategy.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Max Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: In this spread, -0.95 means, 95% of the options strategy maximum loss is reached and, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Call bull spread indicatorCall bull spread indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a DEBIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

- Call spread price (Debit): The debit paid for one unit of options strategy.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Max Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: In this spread, -0.95 means, 95% of the options strategy maximum loss is reached and, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Put option buy or sell indicatorPut option indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Buy or sell (the strategy)

-The option price bought: at what price did you bought/sold one option.

-Instrument price when bought: the stock price when you bought/sold the option.

-Strike price: the strike price of the option.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-Risk to reward: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (3).

Example: If an option was bought, -0.95 means, 95% of the option value is lost (unrealized). If an option was bought, 3 means, the risk to reward is 3.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Call option buy or sell indicatorCall option indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Buy or sell (the strategy)

-The option price bought: at what price did you bought/sold one option.

-Instrument price when bought: the stock price when you bought/sold the option.

-Strike price: the strike price of the option.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-Risk to reward: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (3).

Example: If an option was bought, -0.95 means, 95% of the option value is lost (unrealized). If an option was bought, 3 means, the risk to reward is 3.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Synthetic VX3! & VX4! continuous /VX futuresTradingView is missing continuous 3rd and 4th month VIX (/VX) futures, so I decided to try to make a synthetic one that emulates what continuous maturity futures would look like. This is useful for backtesting/historical purposes as it enables traders to see how their further out VX contracts would've performed vs the front month contract.

The indicator pulls actual realtime data (if you subscribe to the CBOE data package) or 15 minute delayed data for the VIX spot (the actual non-tradeable VIX index), the continuous front month (VX1!), and the continuous second month (VX2!) continually rolled contracts. Then the indicator's script applies a formula to fairly closely estimate how 3rd and 4th month continuous contracts would've moved.

It uses an exponential mean‑reversion to a long‑run level formula using:

σ(T) = θ+(σ0−θ)e−kT

You can expect it to be off by ~5% or so (in times of backwardation it might be less accurate).

MeanReversion - LogReturn/Vola ZScoreShows the z-Score of log-return (blue line) and volatility (black line). In statistics, the z-score is the number of standard deviations by which a value of a raw score is above or below the mean value.

This indicator aggregates z-score based on two indicators:

MeanReversion by Logarithmic Returns

MeanReversion by Volatility

Change the time period in bars for longer or shorter time frames. At a daily chart 252 mean on trading year, 21 mean one trading month.

Rectified BB% for option tradingThis indicator shows the bollinger bands against the price all expressed in percentage of the mean BB value. With one sight you can see the amplitude of BB and the variation of the price, evaluate a reenter of the price in the BB.

The relative price is visualized as a candle with open/high/low/close value exspressed as percentage deviation from the BB mean

The indicator include a modified RSI, remapped from 0/100 to -100/100.

You can choose the BB parameters (length, standard deviation multiplier) and the RSI parameter (length, overbougth threshold, ovrsold threshold)

You can exclude/include the candles and the RSI line.

The indicator can be used to sell options when the volatility is high (the bollinger band is wide) and the price is reentering inside the bands.

If the price is forming a supply or demand area it can be a good opportunity to sell a bull put or a bear call

The RSI can be used as confirm of the supply/demand formation

If the bollinger band is narrow and the RSI is overbought/oversold it indicate a better opportunity to buy options

the indicator is designed to work with daily timeframe and default parameters.

ATR and IV Volatility TableThis is a volatility tool designed to get the daily bottom and top values calculated using a daily ATR and IV values.

ATR values can be calculated directly, however for IV I recommend to take the values from external sources for the asset that you want to trade.

Regarding of the usage, I always recommend to go at the end of the previous close day of the candle(with replay function) or beginning of the daily open candle and get the expected values for movements.

For example for 26April for SPX, we have an ATR of 77 points and the close of the candle was 4296.

So based on ATR for 27 April our TOP is going to be 4296 + 77 , while our BOT is going to be 4296-77

At the same time lets assume the IV for today is going to be around 25% -> this is translated to 25 / (sqrt (252)) = 1.57 aprox

So based on IV our TOP is going to be 4296 + 4296 * 0.0157 , while our BOT is going to be 4296 - 4296 * 0.0157

I found out from my calculations that 80-85% of the times these bot and top points act as an amazing support and resistence points for day trading, so I fully recommend you to start including them into your analysis.

If you have any questions let me know !

vx_termsUSAGE

--------

This script helps train your intuition for changes in the VX term structure. I recommend using it on the VIX chart, so you can compare changes in the terms to changes in VIX. It's also nice for calendar spread traders who want to get a feel for the same changes.

1. Select a day, month, and year using the inputs

2. Observe the data table.

3. Open the input again and increment or decrement the day (and month, year as necessary).

4. Click "Ok".

5. Click to deselect the indicator, which allows the chart to load new data.

6. The data table will be reloaded with the next/previous day's data.

The data table has the following columns:

- contract: the VX contracts, in sequence. refer to the CBOE for month codes (F for January, etc.)

- close: the closing price of the contract.

- ma:mb: the spread (difference) between this row and the next row.

- ma:mb chg: the spread's change from prior close.

For example, given the following values for the first two columns:

VXQ2021, 16.5, -3.1, -0.2

VXU2021, 19.6, ..., ...

The front month (Q = august) closed at 16.5, $3.1 below the s\September contract. The negative spread enlarged by $0.20 from $2.90 on the previous trading day.

BUGS, ODDITIES, AND LIMITATIONS:

-------------------------------------------

- The first column will be greyed out after expiration day, which is the 3rd Tuesday of that month. Unfortunately, I can't load the next month's contract due to some limitations with TV.

- The active date is highlighted with a yellow background. When a non-trading date is selected, the highlight will disappear. However, the data table will sometimes fill with the nearest trading date, prematurely. No worries, just know that the data is probably for the previous Friday.

- The script is clunky and slow, but this is the best I can do with TV. Hopefully they add more continuous contracts or allow true dynamic symbol loading.

SPECIAL THANKS:

---------------------

Thanks to HeWhoMustNotBeNamed for helping me get through some messiness. Very helpful guy.

www.tradingview.com

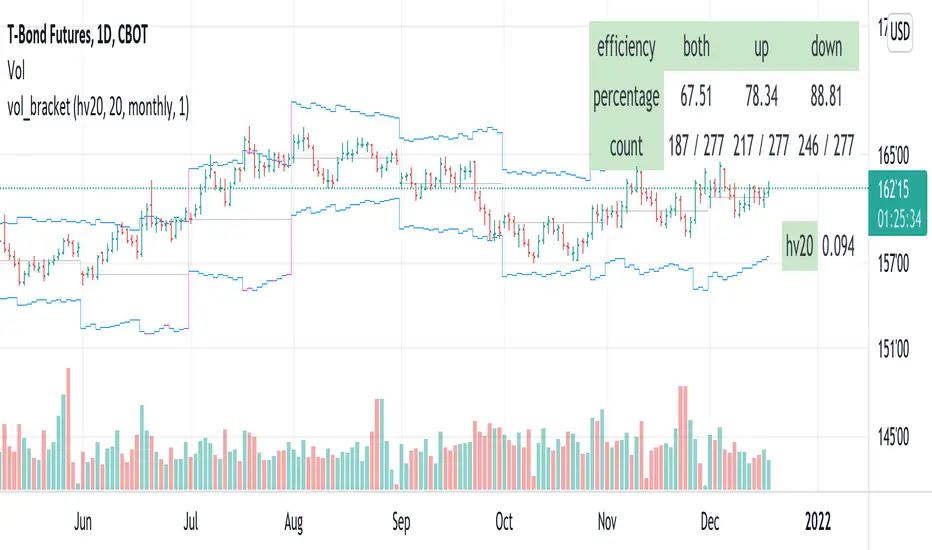

vol_bracketThis simple script shows an "N" standard deviation volatility bracket, anchored at the opening price of the current month, week, or quarter. This anchor is meant to coincide roughly with the expiration of options issued at the same interval. You can choose between a manually-entered IV or the hv30 volatility model.

Unlike my previous scripts, which all show the volatility bracket as a rolling figure, the anchor helps to visualize the volatility estimate in relation to price as it ranges over the (approximate) lifetime of a single, real contract.

VIX Term StructureThis script allows users to visualize the state of the VIX Futures Term Structure. The user is able to select from five CBOE VIX Indices; VIX, VIX9D, VIX3M, VIX6M, and VIX1Y and the script will color the candles based on the price relationship between selected indices. Visit the CBOE website for more info on how the various VIX indices are calculated.

Volatility Price TargetsPrints lines on the chart marking the price points for the standard deviation move using historical volatility. This script was born out of a need to easily spot target points for the wings of my Iron Condor Options trades. The study only shows on the Daily chart. Volatility is calculated based on the standard deviation of the daily returns of price. Price targets are calculated off yesterday's closing price and will not reprint.

Inputs

Days to Expiration - allow you to enter the number of days to expiration for the option, default is 30 for those monthly options traders but can be adjusted to your desire.

Standard Deviation - you can enter the number of deviations for which to calculate the price points 1,2, or 3.

Days in Year - you can adjust the number of days in the year used to calculate the daily volatility multiplier.

ICT Turtle SoupICT Turtle Soup identifies classic “failed breakout” reversals after liquidity sweeps of recent highs/lows, then augments the setup with volume validation, market structure context, Kill Zone (session) filters, Order Blocks (OB), Fair Value Gaps (FVG), OTE (61.8–78.6%) zones, and optional risk targets (SL/TP 1:1, 1:2, 1:3). A compact dashboard summarizes current context (recent high/low, lookbacks, active session, structure state, mitigation counts).

What the Script Does

⦁ Detects Turtle Soup events: Price breaks a prior swing extreme and then quickly reverses back inside the range.

⦁ Grades signal quality: Factors include reversal speed, volume confirmation, breakout magnitude, and consecutive patterns.

⦁ Overlays market context: Trend/range classification (ADX / MA / ATR Bands / Combined), Kill Zones (Asian/London/NY), and time-of-day filters.

⦁ Marks IMB / mitigation zones: Draws Order Blocks and Fair Value Gaps, with optional live mitigation tracking and fading/removal on mitigation.

⦁ Shows OTE zones (61.8–78.6%) after confirmed reversals to highlight potential pullback entries.

⦁ Plots risk management guides: Optional SL buffer below/above reversal wick and TP bands at 1:1, 1:2, 1:3 R multiples.

⦁ Emits alerts on bullish/bearish Turtle Soup confirmations.

How It Works (Conceptual)

1. Liquidity Sweep & Breakout Check

⦁ Looks back over user-defined windows (single or multiple lookbacks: short/medium/long) to find the most recent swing high/low.

⦁ Flags a breakout when price pierces that swing (above for bearish, below for bullish).

⦁ Optional breakout bar volume check requires volume > avg(volume, N) × multiplier.

⦁ Optional swing age check requires the broken swing to be at least X bars old.

2. Reversal Confirmation

⦁ Within N bars after the sweep, validates a mean-reversion close back inside the prior range with a minimum wick/body ratio to confirm rejection.

⦁ Quality Score adds points for:

⦁ Speed: reversal within fast_reversal_bars;

⦁ Volume: breakout and/or reversal volume spike;

⦁ Series: previous consecutive signals;

⦁ Magnitude: sufficient sweep distance.

⦁ Optional high-quality filter only shows signals meeting a minimum score.

3. Context Filters (Optional)

⦁ Sessions/Kill Zones: Only allow signals in selected sessions (Asian/London/NY) with fully custom HHMM inputs.

⦁ Time Window: Restrict to specific hours (e.g., 08–12).

⦁ Market Structure: Classify Trending vs. Ranging (via ADX, MA separation/slope, ATR bands, or Combined). You can allow signals in trends, ranges, or both.

4. Smart Confluence Layers

⦁ Order Blocks: Finds likely OBs with structural validation (e.g., bearish up-candle prior to down move), imbalance score (body/range × volume factor), and extend-until-touched with mitigation % tracking.

⦁ Fair Value Gaps: Detects valid 3-bar gaps (bull/bear) with size threshold, supports touch / 50% / full mitigation logic, and can fade or remove after mitigation.

⦁ OTE Zones: After a reversal, projects the 61.8–78.6% retracement box from the actual swing range; offset scales to timeframe to avoid clutter.

5. Risk & Display

⦁ SL/TP guides: Optional wick-buffered SL and 1:1/1:2/1:3 TPs.

⦁ Dashboard: Recent high/low, active lookbacks, current session, structure label, and live counts of mitigated OBs/FVGs.

Signals & Visuals

⦁ Bullish Turtle Soup: Triangle up + label (🐢S/M/L/D + star rating).

⦁ Bearish Turtle Soup: Triangle down + label (🐢S/M/L/D + star rating).

⦁ Labels can show: quality stars, FAST/SLOW reversal, reversal & breakout volume tags, previous consecutive count, and last move %.

⦁ Lines/Boxes: OBs, FVGs, OTE zones, SL/TP bands, and optional breakout magnitude line.

Inputs (Key Groups)

⦁ Turtle Soup: Lookbacks (single or S/M/L), reversal bars, wick ratio, magnitude line, reversal speed, volume confirmation (multiplier/length), consecutive tracking.

⦁ Order Blocks: Show/validate structure, lookback, extend-until-touched, mitigation % threshold, colors.

⦁ Fair Value Gaps: Show, min size %, colors, mitigation mode (Touch/50%/Full), optional remove-on-mitigation.

⦁ Kill Zones/Sessions: Enable Asian/London/NY with custom HHMM, colors.

⦁ OTE: Show OTE (61.8–78.6%), color, timeframe-adaptive offsets.

⦁ Signal Filters: Filter by session, time window, market structure method (ADX/MA/ATR/Combined), thresholds (ADX, MA periods, ATR multiplier), trending/ranging allowances, structure label & offset.

⦁ SL/TP: SL buffer %, TP 1:1/1:2/1:3 toggles & colors.

⦁ Breakout Validation: Require breakout-bar volume, min swing age, volume label toggles.

⦁ Alerts: Enable/disable.

⦁ Dashboard: Position, text size, colors, border.

How to Use

1. Markets & Timeframes: Works on FX, crypto, indices, and futures. Start with M5–H1 for intraday and H1–H4 for swing; refine lookbacks per instrument volatility.

2. Core Flow:

⦁ Enable multiple lookbacks for robustness on mixed volatility.

⦁ Turn on validate_swing_significance to avoid micro sweeps.

⦁ Use validate_breakout_volume + use_volume_confirmation to filter weak pokes.

3. Context Choice:

⦁ In ranging environments, allow both sides; in trends, consider counter-trend only at HTF OB/FVG/OTE confluence.

⦁ Narrow to London/NY for higher activity if desired.

4. Entries/Stops/Targets:

⦁ Entry on confirmed label close or at OTE pullback post-signal.

⦁ SL: below/above reversal wick + sl_buffer%.

⦁ TP: scale at 1:1/1:2/1:3 or manage via OB/FVG/structure breaks.

5. Confluence: Prefer Turtle Soup that aligns with OB/FVG zones and Combined structure method for added reliability.

Alerts

⦁ “Bullish Turtle Soup detected” and “Bearish Turtle Soup detected” fire on confirmation.

⦁ Set to Once Per Bar (as coded) or adjust in the alert dialog per your workflow.

Notes & Tips

⦁ Multiple lookbacks (S/M/L) help capture both shallow and deep liquidity sweeps.

⦁ Use market structure label with offset to keep it readable on the right of price.

⦁ Mitigation tracking visually communicates when OB/FVG confluence is no longer valid.

⦁ Dashboard = fast situational awareness; keep it on during live trading.

Limitations & Disclaimer

⦁ This tool is educational and not financial advice. No profitability or win-rate is implied. Markets carry risk; manage position size and test thoroughly.

⦁ Signal quality depends on market regime, spreads, news, and data quality. Backtests/forward-tests may differ.

⦁ Visual objects are capped for performance; old items may auto-clean to keep charts responsive.

Talandra TI – NQ LiteTalandra TI – NQ Lite Edition

Talandra TI – NQ Lite is a technical indicator created for disciplined futures trading on the NASDAQ 100 E-mini and Micro contracts (NQ1!). It is specifically calibrated for the five-minute and one-hour timeframes and is intended for traders who rely on objective directional alignment rather than discretionary signaling. The indicator incorporates a structured confluence of market components, including long-term trend structure through a 120-period simple moving average, momentum validation via short-term exponential and MACD crossovers, volatility screening through ATR-based range logic, and institutional participation assessment using relative volume analysis. All calculations are bound to the active chart price, ensuring the indicator remains visually synchronized with price movement without lag or drift.

The Lite Edition is designed for execution clarity and performance efficiency. By removing labels, commentary, and auxiliary markings, it presents only the essential directional outputs in the form of live BUY and SELL signals. This presentation style supports both discretionary and alert-based trading approaches, while maintaining full non-repainting integrity. Each signal reflects confirmed market alignment rather than early or speculative entry triggers, making the tool appropriate for structured systems, rule-based trading, and algorithmic integration.

Talandra TI – NQ Lite is intended for application on NASDAQ futures exclusively, with performance optimized on the five-minute chart for intraday decision-making and the one-hour chart for macro directional posture. It is not designed for countertrend entry, mean reversion, or adaptation across equity or cryptocurrency markets without modification. The indicator does not include risk management functions; users must provide their own stop-loss, position sizing, and capital control protocols. It is expressly a directional confirmation tool rather than a complete trading system.

This indicator does not provide financial advice or trading recommendations. It is offered purely for educational and informational purposes. Futures and derivatives trading involve significant risk, including the potential for substantial financial loss. No guarantee of accuracy, profitability, or trading performance is expressed or implied. Users accept full responsibility for all trade execution, including risk evaluation and capital exposure.

Talandra TI – NQ Lite is authored by JD Harmelin, with a focus on systematic market structure and momentum-based confirmation logic. The current release is Version 1.0, first published in 2025, representing the initial implementation of price-locked execution logic and macro trend integration. All rights are reserved. Redistribution or commercial use of this script without explicit written permission is prohibited. Use of this indicator constitutes acknowledgment and acceptance of full responsibility for any trading outcomes resulting from its application.

Copeland Dynamic Dominance Matrix System | GForgeCopeland Dynamic Dominance Matrix System | GForge - v1

---

📊 COMPREHENSIVE SYSTEM OVERVIEW

The GForge Dynamic BB% TrendSync System represents a revolutionary approach to algorithmic portfolio management, combining cutting-edge statistical analysis, momentum detection, and regime identification into a unified framework. This system processes up to 39 different cryptocurrency assets simultaneously, using advanced mathematical models to determine optimal capital allocation across dynamic market conditions.

Core Innovation: Multi-Dimensional Analysis

Unlike traditional single-asset indicators, this system operates on multiple analytical dimensions:

Momentum Analysis: Dual Bollinger Band Modified Deviation (DBBMD) calculations

Relative Strength: Comprehensive dominance matrix with head-to-head comparisons

Fundamental Screening: Alpha and Beta statistical filtering

Market Regime Detection: Five-component statistical testing framework

Portfolio Optimization: Dynamic weighting and allocation algorithms

Risk Management: Multi-layered protection and regime-based positioning

---

🔧 DETAILED COMPONENT BREAKDOWN

1. Dynamic Bollinger Band % Modified Deviation Engine (DBBMD)

The foundation of this system is an advanced oscillator that combines two independent Bollinger Band systems with asymmetric parameters to create unique momentum readings.

Technical Implementation:

[

// BB System 1: Fast-reacting with extended standard deviation

primary_bb1_ma_len = 40 // Shorter MA for responsiveness

primary_bb1_sd_len = 65 // Longer SD for stability

primary_bb1_mult = 1.0 // Standard deviation multiplier

// BB System 2: Complementary asymmetric design

primary_bb2_ma_len = 8 // Longer MA for trend following

primary_bb2_sd_len = 66 // Shorter SD for volatility sensitivity

primary_bb2_mult = 1.7 // Wider bands for reduced noise

Key Features:

Asymmetric Design: The intentional mismatch between MA and Standard Deviation periods creates unique oscillation characteristics that traditional Bollinger Bands cannot achieve

Percentage Scale: All readings are normalized to 0-100% scale for consistent interpretation across assets

Multiple Combination Modes:

BB1 Only: Fast/reactive system

BB2 Only: Smooth/stable system

Average: Balanced blend (recommended)

Both Required: Conservative (both must agree)

Either One: Aggressive (either can trigger)

Mean Deviation Filter: Additional volatility-based layer that measures the standard deviation of the DBBMD% itself, creating dynamic trigger bands

Signal Generation Logic:

// Primary thresholds

primary_long_threshold = 71 // DBBMD% level for bullish signals

primary_short_threshold = 33 // DBBMD% level for bearish signals

// Mean Deviation creates dynamic bands around these thresholds

upper_md_band = combined_bb + (md_mult * bb_std)

lower_md_band = combined_bb - (md_mult * bb_std)

// Signal triggers when DBBMD crosses these dynamic bands

long_signal = lower_md_band > long_threshold

short_signal = upper_md_band < short_threshold

For more information on this BB% indicator, find it here:

2. Revolutionary Dominance Matrix System

This is the system's most sophisticated innovation - a comprehensive framework that compares every asset against every other asset to determine relative strength hierarchies.

Mathematical Foundation:

The system constructs a mathematical matrix where each cell represents whether asset i dominates asset j:

// Core dominance matrix (39x39 for maximum assets)

var matrix dominance_matrix = matrix.new(39, 39, 0)

// For each qualifying asset pair (i,j):

for i = 0 to active_count - 1

for j = 0 to active_count - 1

if i != j

// Calculate price ratio BB% TrendSync for asset_i/asset_j

ratio_array = calculate_price_ratios(asset_i, asset_j)

ratio_dbbmd = calculate_dbbmd(ratio_array)

// Asset i dominates j if ratio is in uptrend

if ratio_dbbmd_state == 1

matrix.set(dominance_matrix, i, j, 1)

Copeland Scoring Algorithm:

Each asset receives a dominance score calculated as:

Dominance Score = Total Wins - Total Losses

// Calculate net dominance for each asset

for i = 0 to active_count - 1

wins = 0

losses = 0

for j = 0 to active_count - 1

if i != j

if matrix.get(dominance_matrix, i, j) == 1

wins += 1

else

losses += 1

copeland_score = wins - losses

array.set(dominance_scores, i, copeland_score)

Head-to-Head Analysis Process:

Ratio Construction: For each asset pair, calculate price_asset_A / price_asset_B

DBBMD Application: Apply the same DBBMD analysis to these ratios

Trend Determination: If ratio DBBMD shows uptrend, Asset A dominates Asset B

Matrix Population: Store dominance relationships in mathematical matrix

Score Calculation: Sum wins minus losses for final ranking

This creates a tournament-style ranking where each asset's strength is measured against all others, not just against a benchmark.

3. Advanced Alpha & Beta Filtering System

The system incorporates fundamental analysis through Capital Asset Pricing Model (CAPM) calculations to filter assets based on risk-adjusted performance.

Alpha Calculation (Excess Return Analysis):

// CAPM Alpha calculation

f_calc_alpha(asset_prices, benchmark_prices, alpha_length, beta_length, risk_free_rate) =>

// Calculate asset and benchmark returns

asset_returns = calculate_returns(asset_prices, alpha_length)

benchmark_returns = calculate_returns(benchmark_prices, alpha_length)

// Get beta for expected return calculation

beta = f_calc_beta(asset_prices, benchmark_prices, beta_length)

// Average returns over period

avg_asset_return = array_average(asset_returns) * 100

avg_benchmark_return = array_average(benchmark_returns) * 100

// Expected return using CAPM: E(R) = Beta * Market_Return + Risk_Free_Rate

expected_return = beta * avg_benchmark_return + risk_free_rate

// Alpha = Actual Return - Expected Return

alpha = avg_asset_return - expected_return

Beta Calculation (Volatility Relationship):

// Beta measures how much an asset moves relative to benchmark

f_calc_beta(asset_prices, benchmark_prices, length) =>

// Calculate return series for both assets

asset_returns =

benchmark_returns =

// Populate return arrays

for i = 0 to length - 1

asset_return = (current_price - previous_price) / previous_price

benchmark_return = (current_bench - previous_bench) / previous_bench

// Calculate covariance and variance

covariance = calculate_covariance(asset_returns, benchmark_returns)

benchmark_variance = calculate_variance(benchmark_returns)

// Beta = Covariance(Asset, Market) / Variance(Market)

beta = covariance / benchmark_variance

Filtering Applications:

Alpha Filter: Only includes assets with alpha above specified threshold (e.g., >0.5% monthly excess return)

Beta Filter: Screens for desired volatility characteristics (e.g., beta >1.0 for aggressive assets)

Combined Screening: Both filters must pass for asset qualification

Dynamic Thresholds: User-configurable parameters for different market conditions

4. Intelligent Tie-Breaking Resolution System

When multiple assets have identical dominance scores, the system employs sophisticated methods to determine final rankings.

Standard Tie-Breaking Hierarchy:

// Primary tie-breaking logic

if score_i == score_j // Tied dominance scores

// Level 1: Compare Beta values (higher beta wins)

beta_i = array.get(beta_values, i)

beta_j = array.get(beta_values, j)

if beta_j > beta_i

swap_positions(i, j)

else if beta_j == beta_i

// Level 2: Compare Alpha values (higher alpha wins)

alpha_i = array.get(alpha_values, i)

alpha_j = array.get(alpha_values, j)

if alpha_j > alpha_i

swap_positions(i, j)

Advanced Tie-Breaking (Head-to-Head Analysis):

For the top 3 performers, an enhanced tie-breaking mechanism analyzes direct head-to-head price ratio performance:

// Advanced tie-breaker for top performers

f_advanced_tiebreaker(asset1_idx, asset2_idx, lookback_period) =>

// Calculate price ratio over lookback period

ratio_history =

for k = 0 to lookback_period - 1

price_ratio = price_asset1 / price_asset2

array.push(ratio_history, price_ratio)

// Apply simplified trend analysis to ratio

current_ratio = array.get(ratio_history, 0)

average_ratio = calculate_average(ratio_history)

// Asset 1 wins if current ratio > average (trending up)

if current_ratio > average_ratio

return 1 // Asset 1 dominates

else

return -1 // Asset 2 dominates

5. Five-Component Aggregate Market Regime Filter

This sophisticated framework combines multiple statistical tests to determine whether market conditions favor trending strategies or require defensive positioning.

Component 1: Augmented Dickey-Fuller (ADF) Test

Tests for unit root presence to distinguish between trending and mean-reverting price series.

// Simplified ADF implementation

calculate_adf_statistic(price_series, lookback) =>

// Calculate first differences

differences =

for i = 0 to lookback - 2

diff = price_series - price_series

array.push(differences, diff)

// Statistical analysis of differences

mean_diff = calculate_mean(differences)

std_diff = calculate_standard_deviation(differences)

// ADF statistic approximation

adf_stat = mean_diff / std_diff

// Compare against threshold for trend determination

is_trending = adf_stat <= adf_threshold

Component 2: Directional Movement Index (DMI)

Classic Wilder indicator measuring trend strength through directional movement analysis.

// DMI calculation for trend strength

calculate_dmi_signal(high_data, low_data, close_data, period) =>

// Calculate directional movements

plus_dm_sum = 0.0

minus_dm_sum = 0.0

true_range_sum = 0.0

for i = 1 to period

// Directional movements

up_move = high_data - high_data

down_move = low_data - low_data

// Accumulate positive/negative movements

if up_move > down_move and up_move > 0

plus_dm_sum += up_move

if down_move > up_move and down_move > 0

minus_dm_sum += down_move

// True range calculation

true_range_sum += calculate_true_range(i)

// Calculate directional indicators

di_plus = 100 * plus_dm_sum / true_range_sum

di_minus = 100 * minus_dm_sum / true_range_sum

// ADX calculation

dx = 100 * math.abs(di_plus - di_minus) / (di_plus + di_minus)

adx = dx // Simplified for demonstration

// Trending if ADX above threshold

is_trending = adx > dmi_threshold

Component 3: KPSS Stationarity Test

Complementary test to ADF that examines stationarity around trend components.

// KPSS test implementation

calculate_kpss_statistic(price_series, lookback, significance_level) =>

// Calculate mean and variance

series_mean = calculate_mean(price_series, lookback)

series_variance = calculate_variance(price_series, lookback)

// Cumulative sum of deviations

cumulative_sum = 0.0

cumsum_squared_sum = 0.0

for i = 0 to lookback - 1

deviation = price_series - series_mean

cumulative_sum += deviation

cumsum_squared_sum += math.pow(cumulative_sum, 2)

// KPSS statistic

kpss_stat = cumsum_squared_sum / (lookback * lookback * series_variance)

// Compare against critical values

critical_value = significance_level == 0.01 ? 0.739 :

significance_level == 0.05 ? 0.463 : 0.347

is_trending = kpss_stat >= critical_value

Component 4: Choppiness Index

Measures market directionality using fractal dimension analysis of price movement.

// Choppiness Index calculation

calculate_choppiness(price_data, period) =>

// Find highest and lowest over period

highest = price_data

lowest = price_data

true_range_sum = 0.0

for i = 0 to period - 1

if price_data > highest

highest := price_data

if price_data < lowest

lowest := price_data

// Accumulate true range

if i > 0

true_range = calculate_true_range(price_data, i)

true_range_sum += true_range

// Choppiness calculation

range_high_low = highest - lowest

choppiness = 100 * math.log10(true_range_sum / range_high_low) / math.log10(period)

// Trending if choppiness below threshold (typically 61.8)

is_trending = choppiness < 61.8

Component 5: Hilbert Transform Analysis

Phase-based cycle detection and trend identification using mathematical signal processing.

// Hilbert Transform trend detection

calculate_hilbert_signal(price_data, smoothing_period, filter_period) =>

// Smooth the price data

smoothed_price = calculate_moving_average(price_data, smoothing_period)

// Calculate instantaneous phase components

// Simplified implementation for demonstration

instant_phase = smoothed_price

delayed_phase = calculate_moving_average(price_data, filter_period)

// Compare instantaneous vs delayed signals

phase_difference = instant_phase - delayed_phase

// Trending if instantaneous leads delayed

is_trending = phase_difference > 0

Aggregate Regime Determination:

// Combine all five components

regime_calculation() =>

trending_count = 0

total_components = 0

// Test each enabled component

if enable_adf and adf_signal == 1

trending_count += 1

if enable_adf

total_components += 1

// Repeat for all five components...

// Calculate trending proportion

trending_proportion = trending_count / total_components

// Market is trending if proportion above threshold

regime_allows_trading = trending_proportion >= regime_threshold

The system only allows asset positions when the specified percentage of components indicate trending conditions. During choppy or mean-reverting periods, the system automatically positions in USD to preserve capital.

6. Dynamic Portfolio Weighting Framework

Six sophisticated allocation methodologies provide flexibility for different market conditions and risk preferences.

Weighting Method Implementations:

1. Equal Weight Distribution:

// Simple equal allocation

if weighting_mode == "Equal Weight"

weight_per_asset = 1.0 / selection_count

for i = 0 to selection_count - 1

array.push(weights, weight_per_asset)

2. Linear Dominance Scaling:

// Linear scaling based on dominance scores

if weighting_mode == "Linear Dominance"

// Normalize scores to 0-1 range

min_score = array.min(dominance_scores)

max_score = array.max(dominance_scores)

score_range = max_score - min_score

total_weight = 0.0

for i = 0 to selection_count - 1

score = array.get(dominance_scores, i)

normalized = (score - min_score) / score_range

weight = 1.0 + normalized * concentration_factor

array.push(weights, weight)

total_weight += weight

// Normalize to sum to 1.0

for i = 0 to selection_count - 1

current_weight = array.get(weights, i)

array.set(weights, i, current_weight / total_weight)

3. Conviction Score (Exponential):

// Exponential scaling for high conviction

if weighting_mode == "Conviction Score"

// Combine dominance score with DBBMD strength

conviction_scores =

for i = 0 to selection_count - 1

dominance = array.get(dominance_scores, i)

dbbmd_strength = array.get(dbbmd_values, i)

conviction = dominance + (dbbmd_strength - 50) / 25

array.push(conviction_scores, conviction)

// Exponential weighting

total_weight = 0.0

for i = 0 to selection_count - 1

conviction = array.get(conviction_scores, i)

normalized = normalize_score(conviction)

weight = math.pow(1 + normalized, concentration_factor)

array.push(weights, weight)

total_weight += weight

// Final normalization

normalize_weights(weights, total_weight)

Advanced Features:

Minimum Position Constraint: Prevents dust allocations below specified threshold

Concentration Factor: Adjustable parameter controlling weight distribution aggressiveness

Dominance Boost: Extra weight for assets exceeding specified dominance thresholds

Dynamic Rebalancing: Automatic weight recalculation on portfolio changes

7. Intelligent USD Management System

The system treats USD as a competing asset with its own dominance score, enabling sophisticated cash management.

USD Scoring Methodologies:

Smart Competition Mode (Recommended):

f_calculate_smart_usd_dominance() =>

usd_wins = 0

// USD beats assets in downtrends or weak uptrends

for i = 0 to active_count - 1

asset_state = get_asset_state(i)

asset_dbbmd = get_asset_dbbmd(i)

// USD dominates shorts and weak longs

if asset_state == -1 or (asset_state == 1 and asset_dbbmd < long_threshold)

usd_wins += 1

// Calculate Copeland-style score

base_score = usd_wins - (active_count - usd_wins)

// Boost during weak market conditions

qualified_assets = count_qualified_long_assets()

if qualified_assets <= active_count * 0.2

base_score := math.round(base_score * usd_boost_factor)

base_score

Auto Short Count Mode:

// USD dominance based on number of bearish assets

usd_dominance = count_assets_in_short_state()

// Apply boost during low activity

if qualified_long_count <= active_count * 0.2

usd_dominance := usd_dominance * usd_boost_factor

Regime-Based USD Positioning:

When the five-component regime filter indicates unfavorable conditions, the system automatically overrides all asset signals and positions 100% in USD, protecting capital during choppy markets.

8. Multi-Asset Infrastructure & Data Management

The system maintains comprehensive data structures for up to 39 assets simultaneously.

Data Collection Framework:

// Full OHLC data matrices (200 bars depth for performance)

var matrix open_data = matrix.new(39, 200, na)

var matrix high_data = matrix.new(39, 200, na)

var matrix low_data = matrix.new(39, 200, na)

var matrix close_data = matrix.new(39, 200, na)

// Real-time data collection

if barstate.isconfirmed

for i = 0 to active_count - 1

ticker = array.get(assets, i)

= request.security(ticker, timeframe.period,

[open , high , low , close ],

lookahead=barmerge.lookahead_off)

// Store in matrices with proper shifting

matrix.set(open_data, i, 0, nz(o, 0))

matrix.set(high_data, i, 0, nz(h, 0))

matrix.set(low_data, i, 0, nz(l, 0))

matrix.set(close_data, i, 0, nz(c, 0))

Asset Configuration:

The system comes pre-configured with 39 major cryptocurrency pairs across multiple exchanges:

Major Pairs: BTC, ETH, XRP, SOL, DOGE, ADA, etc.

Exchange Coverage: Binance, KuCoin, MEXC for optimal liquidity

Configurable Count: Users can activate 2-39 assets based on preferences

Custom Tickers: All asset selections are user-modifiable

---

⚙️ COMPREHENSIVE CONFIGURATION GUIDE

Portfolio Management Settings

Maximum Portfolio Size (1-10):

Conservative (1-2): High concentration, captures strong trends

Balanced (3-5): Moderate diversification with trend focus

Diversified (6-10): Lower concentration, broader market exposure

Dominance Clarity Threshold (0.1-1.0):

Low (0.1-0.4): Prefers diversification, holds multiple assets frequently

Medium (0.5-0.7): Balanced approach, context-dependent allocation

High (0.8-1.0): Concentration-focused, single asset preference

Signal Generation Parameters

DBBMD Thresholds:

// Standard configuration

primary_long_threshold = 71 // Conservative: 75+, Aggressive: 65-70

primary_short_threshold = 33 // Conservative: 25-30, Aggressive: 35-40

// BB System parameters

bb1_ma_len = 40 // Fast system: 20-50

bb1_sd_len = 65 // Stability: 50-80

bb2_ma_len = 8 // Trend: 60-100

bb2_sd_len = 66 // Sensitivity: 10-20

Risk Management Configuration

Alpha/Beta Filters:

Alpha Threshold: 0.0-2.0% (higher = more selective)

Beta Threshold: 0.5-2.0 (1.0+ for aggressive assets)

Calculation Periods: 20-50 bars (longer = more stable)

Regime Filter Settings:

Trending Threshold: 0.3-0.8 (higher = stricter trend requirements)

Component Lookbacks: 30-100 bars (balance responsiveness vs stability)

Enable/Disable: Individual component control for customization

---

📊 PERFORMANCE TRACKING & VISUALIZATION

Real-Time Dashboard Features

The compact dashboard provides essential information:

Current Holdings: Asset names and allocation percentages

Dominance Score: Current position's relative strength ranking

Active Assets: Qualified long signals vs total asset count

Returns: Total portfolio performance percentage

Maximum Drawdown: Peak-to-trough decline measurement

Trade Count: Total portfolio transitions executed

Regime Status: Current market condition assessment

Comprehensive Ranking Table

The left-side table displays detailed asset analysis:

Ranking Position: Numerical order by dominance score

Asset Symbol: Clean ticker identification with color coding

Dominance Score: Net wins minus losses in head-to-head comparisons

Win-Loss Record: Detailed breakdown of dominance relationships

DBBMD Reading: Current momentum percentage with threshold highlighting

Alpha/Beta Values: Fundamental analysis metrics when filters enabled

Portfolio Weight: Current allocation percentage in signal portfolio

Execution Status: Visual indicator of actual holdings vs signals

Visual Enhancement Features

Color-Coded Assets: 39 distinct colors for easy identification

Regime Background: Red tinting during unfavorable market conditions

Dynamic Equity Curve: Portfolio value plotted with position-based coloring

Status Indicators: Symbols showing execution vs signal states

---

🔍 ADVANCED TECHNICAL FEATURES

State Persistence System

The system maintains asset states across bars to prevent excessive switching:

// State tracking for each asset and ratio combination

var array asset_states = array.new(1560, 0) // 39 * 40 ratios

// State changes only occur on confirmed threshold breaks

if long_crossover and current_state != 1

current_state := 1

array.set(asset_states, asset_index, 1)

else if short_crossover and current_state != -1

current_state := -1

array.set(asset_states, asset_index, -1)

Transaction Cost Integration

Realistic modeling of trading expenses:

// Transaction cost calculation

transaction_fee = 0.4 // Default 0.4% (fees + slippage)

// Applied on portfolio transitions

if should_execute_transition

was_holding_assets = check_current_holdings()

will_hold_assets = check_new_signals()

// Charge fees for meaningful transitions

if transaction_fee > 0 and (was_holding_assets or will_hold_assets)

fee_amount = equity * (transaction_fee / 100)

equity -= fee_amount

total_fees += fee_amount

Dynamic Memory Management

Optimized data structures for performance:

200-Bar History: Sufficient for calculations while maintaining speed

Matrix Operations: Efficient storage and retrieval of multi-asset data

Array Recycling: Memory-conscious data handling for long-running backtests

Conditional Calculations: Skip unnecessary computations during initialization

12H 30 assets portfolio

---

🚨 SYSTEM LIMITATIONS & TESTING STATUS

CURRENT DEVELOPMENT PHASE: ACTIVE TESTING & OPTIMIZATION

This system represents cutting-edge algorithmic trading technology but remains in continuous development. Key considerations:

Known Limitations:

Requires significant computational resources for 39-asset analysis

Performance varies significantly across different market conditions

Complex parameter interactions may require extensive optimization

Slippage and liquidity constraints not fully modeled for all assets

No consideration for market impact in large position sizes

Areas Under Active Development:

Enhanced regime detection algorithms

Improved transaction cost modeling

Additional portfolio weighting methodologies

Machine learning integration for parameter optimization

Cross-timeframe analysis capabilities

---

🔒 ANTI-REPAINTING ARCHITECTURE & LIVE TRADING READINESS

One of the most critical aspects of any trading system is ensuring that signals and calculations are based on confirmed, historical data rather than current bar information that can change throughout the trading session. This system implements comprehensive anti-repainting measures to ensure 100% reliability for live trading .

The Repainting Problem in Trading Systems

Repainting occurs when an indicator uses current, unconfirmed bar data in its calculations, causing:

False Historical Signals: Backtests appear better than reality because calculations change as bars develop

Live Trading Failures: Signals that looked profitable in testing fail when deployed in real markets

Inconsistent Results: Different results when running the same indicator at different times during a trading session

Misleading Performance: Inflated win rates and returns that cannot be replicated in practice

GForge Anti-Repainting Implementation

This system eliminates repainting through multiple technical safeguards:

1. Historical Data Usage for All Calculations

// CRITICAL: All calculations use PREVIOUS bar data (note the offset)

= request.security(ticker, timeframe.period,

[open , high , low , close , close],

lookahead=barmerge.lookahead_off)

// Store confirmed previous bar OHLC for calculations

matrix.set(open_data, i, 0, nz(o1, 0)) // Previous bar open

matrix.set(high_data, i, 0, nz(h1, 0)) // Previous bar high

matrix.set(low_data, i, 0, nz(l1, 0)) // Previous bar low

matrix.set(close_data, i, 0, nz(c1, 0)) // Previous bar close

// Current bar close only for visualization

matrix.set(current_prices, i, 0, nz(c0, 0)) // Live price display

2. Confirmed Bar State Processing

// Only process data when bars are confirmed and closed

if barstate.isconfirmed

// All signal generation and portfolio decisions occur here

// using only historical, unchanging data

// Shift historical data arrays

for i = 0 to active_count - 1

for bar = math.min(data_bars, 199) to 1

// Move confirmed data through historical matrices

old_data = matrix.get(close_data, i, bar - 1)

matrix.set(close_data, i, bar, old_data)

// Process new confirmed bar data

calculate_all_signals_and_dominance()

3. Lookahead Prevention

// Explicit lookahead prevention in all security calls

request.security(ticker, timeframe.period, expression,

lookahead=barmerge.lookahead_off)

// This ensures no future data can influence current calculations

// Essential for maintaining signal integrity across all timeframes

4. State Persistence with Historical Validation

// Asset states only change based on confirmed threshold breaks

// using historical data that cannot change

var array asset_states = array.new(1560, 0)

// State changes use only confirmed, previous bar calculations

if barstate.isconfirmed

=

f_calculate_enhanced_dbbmd(confirmed_price_array, ...)

// Only update states after bar confirmation

if long_crossover_confirmed and current_state != 1

current_state := 1

array.set(asset_states, asset_index, 1)

Live Trading vs. Backtesting Consistency

The system's architecture ensures identical behavior in both environments:

Backtesting Mode:

Uses historical offset data for all calculations

Processes confirmed bars with `barstate.isconfirmed`

Maintains identical signal generation logic

No access to future information

Live Trading Mode:

Uses same historical offset data structure

Waits for bar confirmation before signal updates

Identical mathematical calculations and thresholds

Real-time price display without affecting signals

Technical Implementation Details

Data Collection Timing

// Example of proper data collection timing

if barstate.isconfirmed // Wait for bar to close

// Collect PREVIOUS bar's confirmed OHLC data

for i = 0 to active_count - 1

ticker = array.get(assets, i)

// Get confirmed previous bar data (note offset)

=

request.security(ticker, timeframe.period,

[open , high , low , close , close],

lookahead=barmerge.lookahead_off)

// ALL calculations use prev_* values

// current_close only for real-time display

portfolio_calculations_use_previous_bar_data()

Signal Generation Process

// Signal generation workflow (simplified)

if barstate.isconfirmed and data_bars >= minimum_required_bars

// Step 1: Calculate DBBMD using historical price arrays

for i = 0 to active_count - 1

historical_prices = get_confirmed_price_history(i) // Uses offset data

= calculate_dbbmd(historical_prices)

update_asset_state(i, state)

// Step 2: Build dominance matrix using confirmed data

calculate_dominance_relationships() // All historical data

// Step 3: Generate portfolio signals

new_portfolio = generate_target_portfolio() // Based on confirmed calculations

// Step 4: Compare with previous signals for changes

if portfolio_signals_changed()

execute_portfolio_transition()

Verification Methods for Users

Users can verify the anti-repainting behavior through several methods:

1. Historical Replay Test

Run the indicator on historical data

Note signal timing and portfolio changes

Replay the same period - signals should be identical

No retroactive changes in historical signals

2. Intraday Consistency Check

Load indicator during active trading session

Observe that previous day's signals remain unchanged

Only current day's final bar should show potential signal changes

Refresh indicator - historical signals should be identical

Live Trading Deployment Considerations

Data Quality Assurance

Exchange Connectivity: Ensure reliable data feeds for all 39 assets

Missing Data Handling: System includes safeguards for data gaps

Price Validation: Automatic filtering of obvious price errors

Timeframe Synchronization: All assets synchronized to same bar timing

Performance Impact of Anti-Repainting Measures

The robust anti-repainting implementation requires additional computational resources:

Memory Usage: 200-bar historical data storage for 39 assets

Processing Delay: Signals update only after bar confirmation

Calculation Overhead: Multiple historical data validations

Alert Timing: Slight delay compared to current-bar indicators

However, these trade-offs are essential for reliable live trading performance and accurate backtesting results.

Critical: Equity Curve Anti-Repainting Architecture

The most sophisticated aspect of this system's anti-repainting design is the temporal separation between signal generation and performance calculation . This creates a realistic trading simulation that perfectly matches live trading execution.

The Timing Sequence

// STEP 1: Store what we HELD during the current bar (for performance calc)

if barstate.isconfirmed

// Record positions that were active during this bar

array.clear(held_portfolio)

array.clear(held_weights)

for i = 0 to array.size(execution_portfolio) - 1

array.push(held_portfolio, array.get(execution_portfolio, i))

array.push(held_weights, array.get(execution_weights, i))

// STEP 2: Calculate performance based on what we HELD

portfolio_return = 0.0

for i = 0 to array.size(held_portfolio) - 1

held_asset = array.get(held_portfolio, i)

held_weight = array.get(held_weights, i)

// Performance from current_price vs reference_price

// This is what we ACTUALLY earned during this bar

if held_asset != "USD"

current_price = get_current_price(held_asset) // End of bar

reference_price = get_reference_price(held_asset) // Start of bar

asset_return = (current_price - reference_price) / reference_price

portfolio_return += asset_return * held_weight

// STEP 3: Apply return to equity (realistic timing)

equity := equity * (1 + portfolio_return)

// STEP 4: Generate NEW signals for NEXT period (using confirmed data)

= f_generate_target_portfolio()

// STEP 5: Execute transitions if signals changed

if signal_changed

// Update execution_portfolio for NEXT bar

array.clear(execution_portfolio)

array.clear(execution_weights)

for i = 0 to array.size(new_signal_portfolio) - 1

array.push(execution_portfolio, array.get(new_signal_portfolio, i))

array.push(execution_weights, array.get(new_signal_weights, i))

Why This Prevents Equity Curve Repainting

Performance Attribution: Returns are calculated based on positions that were **actually held** during each bar, not future signals

Signal Timing: New signals are generated **after** performance calculation, affecting only **future** bars

Realistic Execution: Mimics real trading where you earn returns on current positions while planning future moves

No Retroactive Changes: Once a bar closes, its performance contribution to equity is permanent and unchangeable

The One-Bar Offset Mechanism

This system implements a critical one-bar timing offset:

// Bar N: Performance Calculation

// ================================

// 1. Calculate returns on positions held during Bar N

// 2. Update equity based on actual holdings during Bar N

// 3. Plot equity point for Bar N (based on what we HELD)

// Bar N: Signal Generation

// ========================

// 4. Generate signals for Bar N+1 (using confirmed Bar N data)

// 5. Send alerts for what will be held during Bar N+1

// 6. Update execution_portfolio for Bar N+1

// Bar N+1: The Cycle Continues

// =============================

// 1. Performance calculated on positions from Bar N signals

// 2. New signals generated for Bar N+2

Alert System Timing

The alert system reflects this sophisticated timing:

Transaction Cost Realism

Even transaction costs follow realistic timing:

// Fees applied when transitioning between different portfolios

if should_execute_transition

// Charge fees BEFORE taking new positions (realistic timing)

if transaction_fee > 0

fee_amount = equity * (transaction_fee / 100)

equity -= fee_amount // Immediate cost impact

total_fees += fee_amount

// THEN update to new portfolio

update_execution_portfolio(new_signals)

transitions += 1

// Fees reduce equity immediately, affecting all future calculations

// This matches real trading where fees are deducted upon execution

LIVE TRADING CERTIFICATION:

This system has been specifically designed and tested for live trading deployment. The comprehensive anti-repainting measures ensure that:

Backtesting results accurately represent real trading potential

Signals are generated using only confirmed, historical data

No retroactive changes can occur to previously generated signals

Portfolio transitions are based on reliable, unchanging calculations

Performance metrics reflect realistic trading outcomes including proper timing

Users can deploy this system with confidence that live trading results will closely match backtesting performance, subject to normal market execution factors such as slippage and liquidity.

---

⚡ ALERT SYSTEM & AUTOMATION

The system provides comprehensive alerting for automation and monitoring:

Available Alert Conditions

Portfolio Signal Change: Triggered when new portfolio composition is generated

Regime Override Active: Alerts when market regime forces USD positioning

Individual Asset Signals: Can be configured for specific asset transitions

Performance Thresholds: Drawdown or return-based notifications

---

📈 BACKTESTING & PERFORMANCE ANALYSIS

8 Comprehensive Metrics Tracking

The system maintains detailed performance statistics:

Equity Curve: Real-time portfolio value progression

Returns Calculation: Total and annualized performance metrics

Drawdown Analysis: Peak-to-trough decline measurements

Transaction Counting: Portfolio transition frequency

Fee Tracking: Cumulative transaction cost impact

Win Rate Analysis: Success rate of position changes

Backtesting Configuration

// Backtesting parameters

initial_capital = 10000.0 // Starting capital

use_custom_start = true // Enable specific start date

custom_start = timestamp("2023-09-01") // Backtest beginning

transaction_fee = 0.4 // Combined fees and slippage %

// Performance calculation

total_return = (equity - initial_capital) / initial_capital * 100

current_drawdown = (peak_equity - equity) / peak_equity * 100

---

🔧 TROUBLESHOOTING & OPTIMIZATION

Common Configuration Issues

Insufficient Data: Ensure 100+ bars available before start date

[*} Not Compiling: Go on an asset's price chart with 2 or 3 years of data to

make the system compile or just simply reapply the indicator again

Too Many Assets: Reduce active count if experiencing timeouts

Regime Filter Too Strict: Lower trending threshold if always in USD

Excessive Switching: Increase MD multiplier or adjust thresholds

---

💡 USER FEEDBACK & ENHANCEMENT REQUESTS

The continuous evolution of this system depends heavily on user experience and community feedback. Your insights will help motivate me for new improvements and new feature developments.

---

⚖️ FINAL COMPREHENSIVE RISK DISCLAIMER

TRADING INVOLVES SUBSTANTIAL RISK OF LOSS

This indicator is a sophisticated analytical tool designed for educational and research purposes. Important warnings and considerations:

System Limitations:

No algorithmic system can guarantee profitable outcomes

Complex systems may fail in unexpected ways during extreme market events

Historical backtesting does not account for all real-world trading challenges

Slippage, liquidity constraints, and market impact can significantly affect results

System parameters require careful optimization and ongoing monitoring

The creator and distributor of this indicator assume no liability for any financial losses, system failures, or adverse outcomes resulting from its use. This tool is provided "as is" without any warranties, express or implied.

By using this indicator, you acknowledge that you have read, understood, and agreed to assume all risks associated with algorithmic trading and cryptocurrency investments.

Mikula's Master 360° Square of 12Mikula’s Master 360° Square of 12

An educational W. D. Gann study indicator for price and time. Anchor a compact Square of 12 table to a start point you choose. Begin from a bar’s High or Low (or set a manual start price). From that anchor you can progress or regress the table to study how price steps through cycles in either direction.

What you’re looking at :

Zodiac rail (far left): the twelve signs.

Degree rail: 24 rows in 15° steps from 15° up to 360°/0°.

Transit rail and Natal rail: track one planet per rail. Each planet is placed at its current row (℞ shown when retrograde). As longitude advances, the planet climbs bottom → top, then wraps to the bottom at the next sign; during retrograde it steps downward.

Hover a planet’s cell to see a tooltip with its exact longitude and sign (e.g., 152.4° ♌︎). The linked price cell in the grid moves with the planet’s row so you can follow a planet’s path through the zodiac as a path through price.

Price grid (right): the 12×24 Square of 12. Each column is a cycle; cells are stepped price levels from your start price using your increment.

Bottom rail: shows the current square number and labels the twelve columns in that square.

How the square is read

The square always begins at the bottom left. Read each column bottom → top. At the top, return to the bottom of the next column and read up again. One square contains twelve cycles. Because the anchor can be a High or a Low, you can progress the table upward from the anchor or regress it downward while keeping the same bottom-to-top reading order.

Iterate Square (shifting)

Iterate Square shifts the entire 12×24 grid to the next set of twelve cycles.

Square 1 shows cycles 1–12; Square 2 shows 13–24; Square 3 shows 25–36, etc.

Visibility rules

Pivot cells are table-bound. If you shift the square beyond those prices, their highlights won’t appear in the table.

A/B levels and Transit/Natal planetary lines are chart overlays and can remain visible on the table as you shift the square.

Quick use

Choose an anchor (date/time + High/Low) or enable a manual start price .

Set the increment. If you anchored with a Low and want the table to step downward from there, use a negative value.

Optional: pick Transit and Natal planets (one per rail), toggle their plots, and hover their cells for longitude/sign.

Optional: turn on A/B levels to display repeating bands from the start price.

Optional: enable swing pivots to tint matching cells after the anchor.

Use Iterate Square to shift to later squares of twelve cycles.

Examples

These are exploratory examples to spark ideas:

Overview layout (zodiac & degree rails, Transit/Natal rails, price grid)

A-levels plotted, pivots tinted on the table, real-time price highlighted

Drawing angles from the anchor using price & time read from the table

Using a TradingView Gann box along the A-levels to study reactions

Attribution & originality

This script is an original implementation (no external code copied). Conceptual credit to Patrick Mikula, whose discussion of the Master 360° Square of 12 inspired this study’s presentation.

Further reading (neutral pointers)

Patrick Mikula, Gann’s Scientific Methods Unveiled, Vol. 2, “W. D. Gann’s Use of the Circle Chart.”

W. D. Gann’s Original Commodity Course (as provided by WDGAN.com).

No affiliation implied.

License CC BY-NC-SA 4.0 (non-commercial; please attribute @Javonnii and link the original).

Dependency AstroLib by @BarefootJoey

Disclaimer Educational use only; not financial advice.