True Close – Institutional Trading Sessions (Zeiierman)█ Overview

True Close – Institutional Trading Sessions (Zeiierman) is a professional-grade session mapping tool designed to help traders align with how institutions perceive the market’s true close. Unlike the textbook “daily close” used by retail traders, institutional desks often anchor their risk management, execution benchmarks, and exposure metrics to the first hour of the next session.

This indicator visualizes that logic directly on your chart — drawing session boxes, true close levels, and time-aligned labels across Sydney, Tokyo, London, and New York. It highlights the first hour of each session, projects the institutional closing price, and builds a live dashboard that tells you which sessions are active, which are in the critical opening phase, and what levels matter most right now.

More than just a visual tool, this indicator embeds institutional rhythm directly into your workflow — giving you a window into where big players finalize yesterday’s business, rebalance exposure, and execute delayed orders. It’s not just about painting sessions on your chart — it’s about adopting the mindset of those who truly move the market. Institutions don’t settle risk at the bell; they complete it in the next session. This tool lets you see that transition in real time, giving you an edge that goes beyond candles and indicators.

█ How It Works

⚪ Session Detection Engine

Each session is identified by its own time block (e.g., 09:00–17:30 for London). Once a session opens:

A full-session box is drawn to track its range.

The first hour is highlighted separately.

Once the first hour completes, the true close line is plotted, representing the price institutions often treat as the "real" close of the prior day.

⚪ Institutional True Close Logic

The script captures the close of the first hour, not the end of the day.

This line becomes a static reference across your chart, letting you visualize how price interacts with that institutional anchor:

Rejections from it show where yesterday's flow is respected.

Breaks through it may indicate that today's flows are rewriting the narrative.

⚪ Dynamic Dashboard Table

A live table appears in the corner of your screen, showing:

Each session's active status

Whether we’re inside the first hour

The current “true close” price if available

Each cell comes with advanced tooltips giving institutional context, flow dynamics, and market microstructure insights — from rebalancing spillovers to VWAP/TWAP lag effects.

█ How to Use

⚪ Use the First-Hour Line as Your Institutional Anchor

Treat it like the price level that big funds care about. Watch how the price behaves around level. Fades, re-tests, or continuation moves often occur as the market finishes recapping yesterday’s leftover orders.

⚪ Structure Entries Around the Session Context

Are you inside the first hour? Expect more volatility, more decisive flow. After the first session hour, expect fading liquidity as the market slows down and awaits the next session to open.

█ Settings

UTC Offset – Select your preferred time zone; all sessions adjust accordingly.

Session Toggles – Enable/disable Sydney, Tokyo, London, or NY.

Box Display Options – Show/hide session background, first-hour fill, borders.

True Close Line Controls – Enable line, label, and customize width & color.

Execution Hour Labels – Optional toggle for first-hour label placement.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Tradingsessions

Market Session Boxes with Volume Delta [algo_aakash]This script highlights four key forex trading sessions — Tokyo, London, New York, and Sydney — by drawing color-coded boxes directly on the chart. For each session, it shows:

High and low of the session

Total volume traded

Volume delta (bullish vs bearish pressure)

Optional extension of session highs/lows into future candles

Cleanly labeled time range and stats

Users can:

Select which sessions to display

Customize session times (in UTC+0)

Choose colors per session

Toggle session labels and extension lines

Use Case: Designed to help intraday and short-term traders visualize market rhythm, liquidity zones, and session-based volatility. The volume delta metric adds an extra layer of sentiment analysis.

This tool works best on intraday timeframes like 15m, 30m, or 1H.

Disclaimer:

This indicator is for educational and visual analysis purposes. It does not constitute trading advice or guarantee results. Always conduct your own analysis before making trading decisions.

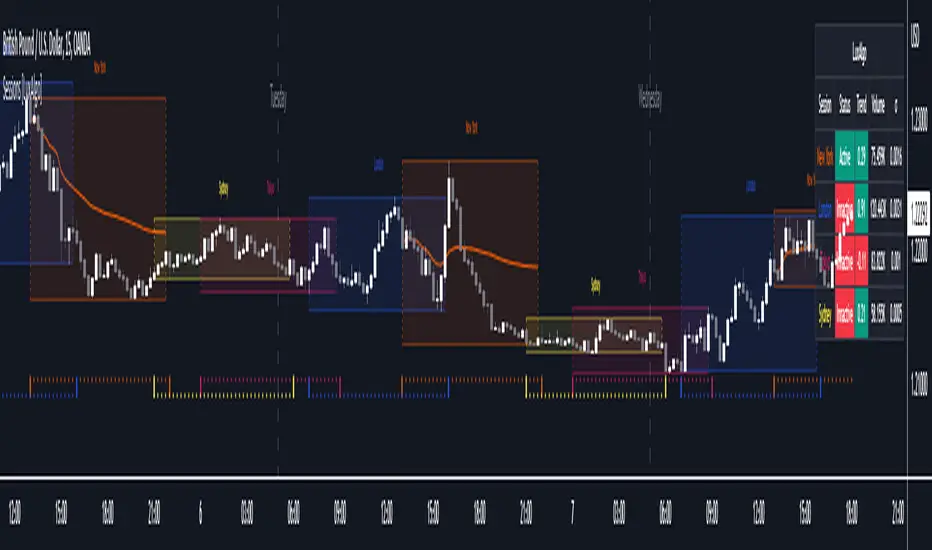

Trading Sessions [BigBeluga]

This indicator brings Smart Money Concept (ICT) session logic to life by plotting key global trading sessions with volume and delta analytics. It not only highlights session ranges but also tracks their midpoints — which often act as intraday support/resistance levels.

🔵 KEY FEATURES

Visual session boxes: Plots boxes for Tokyo, London, New York, and Sydney sessions based on user-defined UTC+0 time ranges.

Volume & delta metrics: Displays total volume and delta volume (buy–sell difference) within each session.

Mid, High & Low Range Extension: Once a session ends, the high, low, and midpoint levels automatically extend — ideal for detecting SR zones.

Session labels: Each box includes a label with session name, time, volume, and delta for quick reference.

Custom session control: Enable or disable sessions individually and configure start/end times.

Clean aesthetics: Transparent shaded boxes with subtle borders make it easy to overlay without clutter.

Sessions Dashboard: Shows the time range of each session and tells you whether the session is currently active.

🔵 USAGE

Enable the sessions you want to monitor (e.g., New York or Tokyo) from the settings.

Use session volume and delta values to gauge the strength and direction of institutional activity.

Watch for price interaction with the extended range — it often acts as dynamic support/resistance after the session ends.

Overlay it with liquidity tools or breaker blocks for intraday strategy alignment.

🔵 EXAMPLES

Extended Future Range acted as resistance/support.

Delta value helped confirm bullish pressure during New York open.

Multiple sessions helped identify kill zone overlaps and high-volume turns.

Trading Sessions is more than just a visual scheduler — it's a precision tool for traders who align with session-based volume dynamics and ICT methodology. Use it to define high-probability zones, confirm volume shifts, and read deeper into the true intent behind market structure.

VWAP Balance Zones - SessionsVWAP Balance Zones Sessions Version is an alternate take on the Original VWAP Balance Zones indicator. The Sessions version allows users to select a specific session to view the VWAP Balance Zones at while still utilizing the full ETH Data.

The Session version provides a better focused display while still maintaining the core functions of the original script with mindful optimizations.

Author's Note: "VBZ Sessions was made with logistics in mind, for the users who only trade within certain times of the day. While it displays the same core concepts, it is not as "Raw" of a display as the Original. For this reason, some users may prefer the Original VWAP Balance Zones, which is why I have opted to release this alternate version instead of updating the original."

> What are VWAP Balance Zones?

"VWAP Balance Zones" is an original concept aimed at identifying the equilibrium area between market participants within the current trend by averaging the Daily Extremes and the Daily VWAP.

Refer to the illustration below for a better understanding of exactly how VWAP Balance Zones are formed:

These zones are displayed for the Daily, Weekly, and Monthly VWAPs, with the most interactive timeframe being the Daily.

> Features

1. The Session Version uses ETH data at all times, and does not solely rely on the chart's data to create the VWAPs or Zones.

This allows the user to focus on a specific trading session, while not losing out on the full VBZ Calculation, with the notable benefit of a cleaner display.

The Original VBZ starts drawing at the beginning of the chart's "Day", and would produce different results when using an RTH chart vs an ETH chart. Along with creating a bird's nest of unusable data at the beginning of the day.

2. Session Start and End lines are displayed for easier identification of the designated trading session.

3. The extreme "Close" Lines are no longer displayed to reduce noise and redundancy.

4. Additionally, the interior VWAP lines are no longer displayed. Ultimately, this was to reduce noise and focus the script on the 50% zones.

5. Weekly and Monthly Zones are now displayed due to the reduced noise!

6. As with the original, the weekly display will yield to the daily, and the monthly display will yield to the weekly.

In the screenshot below, you can observe this behavior.

Enjoy!

London/NY Sessions [jpkxyz]London/NY Sessions Indicator Guide

This indicator tracks the forex market's most active trading periods: London session, New York session, and their overlap.

This characteristics of the London and New York trading sessions are well documented and many traders use them as a key element in their trading strategies. It is most relevant in forex trading, however it is to an extend also applicable in cryptocurrencies.

London Session (08:00-16:00 UTC)

Most active trading session (35% of daily forex volume)

Highest trading volume and liquidity

Major price movements and trend development

Significant institutional participation

New York Session (13:00-20:00 UTC)

Second most active trading period

High institutional order flow

Major US economic releases

Significant impact on USD pairs

London/New York Overlap (13:00-16:00 UTC)

The most active period in forex markets:

Maximum market liquidity

Highest daily trading volume

Strong price movements

Tightest spreads

Peak institutional activity

This indicator helps traders:

Visualize key trading sessions

Track session highs and lows

Monitor overlap dynamics

Identify potential support/resistance levels (session highs/lows)

Sessions Full Markets [TradingFinder] Forex Stocks Index 7 Time🔵 Introduction

In global financial markets, particularly in FOREX and stocks, precise timing of trading sessions plays a crucial role in the success of traders. Each trading session—Asian, European, and American—has its own unique characteristics in terms of volatility and trading volume.

The Asian session (Tokyo), Sydney session, Shanghai session, European session (London and Frankfurt), and American session (New York AM and New York PM) are examples of these trading sessions, each of which opens and closes at specific times.

This session indicator also includes a Time Convertor, enabling users to view FOREX market hours based on GMT, UTC, EST, and local time. Another valuable feature of this indicator is the automatic detection of Daylight Saving Time (DST), which automatically applies time changes for the New York, London, and Sydney sessions.

🔵 How to Use

The indicator also displays session times based on the exact opening and closing times for each geographic region. Users can utilize this indicator to view trading hours either locally or in UTC time, and if needed, set their own custom trading times.

Additionally, the session information table includes the start and end times of each session and whether they are open or closed. This functionality helps traders make better trading decisions by using accurate and precise time data.

Key Features of the Session Indicator

The session indicator is a versatile and advanced tool that provides several unique features for traders.

Some of these features are :

• Automatic Daylight Saving Time (DST) Detection : This indicator dynamically detects Daylight Saving Time (DST) changes for various trading sessions, including New York, London, and Sydney, without requiring manual adjustments. This feature allows traders to manage their trades without worrying about time changes.

Below are the start and end dates for DST in the New York, London, and Sydney trading sessions :

1. New York :

Start of DST: Second Sunday of March, at 2:00 AM.

End of DST: First Sunday of November, at 2:00 AM

2. London :

Start of DST: Last Sunday of March, at 1:00 AM.

End of DST: Last Sunday of October, at 2:00 AM.

3. Sydney :

Start of DST: First Sunday of October, at 2:00 AM.

End of DST: First Sunday of April, at 3:00 AM.

• Session Display Based on Different Time Zones : The session indicator allows users to view trading times based on different time zones, such as UTC, the local time of each market, or the user’s local time. This feature is especially useful for traders operating in diverse geographic regions.

• Custom Trading Time Setup : Another notable feature of this indicator is the ability to set custom trading times. Traders can adjust their own trading times according to their personal strategies and benefit from this flexibility.

• Session Information Table : The session indicator provides a complete information table that includes the exact start and end times of each trading session and whether they are open or closed. This table helps users simultaneously and accurately monitor the status of all trading sessions and make better trading decisions.

🟣 Session Trading Hours Based on Market Mode and Time Zones

The session indicator provides precise information on the start and end times of trading sessions.

These times are adjusted based on different market modes (FOREX, stocks, and TFlab suggestions) and time zones (UTC and local time) :

🟣 (FOREX Session Time) Forex Market Mode

• Sessions in UTC (DST inactive) :

Sydney: 22:00 - 06:00

Tokyo: 23:00 - 07:00

Shanghai: 01:00 - 09:00

Asia: 22:00 - 07:00

Europe: 07:00 - 16:00

London: 08:00 - 16:00

New York: 13:00 - 21:00

• Sessions in UTC (DST active) :

Sydney: 21:00 - 05:00

Tokyo: 23:00 - 07:00

Shanghai: 01:00 - 09:00

Asia: 21:00 - 07:00

Europe: 06:00 - 15:00

London: 07:00 - 15:00

New York: 12:00 - 20:00

• Sessions in Local Time :

Sydney: 08:00 - 16:00

Tokyo: 08:00 - 16:00

Shanghai: 09:00 - 17:00

Asia: 22:00 - 07:00

Europe: 07:00 - 16:00

London: 08:00 - 16:00

New York: 08:00 - 16:00

🟣 Stock Market Trading Hours (Stock Market Mode)

• Sessions in UTC (DST inactive) :

Sydney: 00:00 - 06:00

Asia: 00:00 - 06:00

Europe: 07:00 - 16:30

London: 08:00 - 16:30

New York: 14:30 - 21:00

Tokyo: 00:00 - 06:00

Shanghai: 01:30 - 07:00

• Sessions in UTC (DST active) :

Sydney: 23:00 - 05:00

Asia: 23:00 - 06:00

Europe: 06:00 - 15:30

London: 07:00 - 15:30

New York: 13:30 - 20:00

Tokyo: 00:00 - 06:00

Shanghai: 01:30 - 07:00

• Sessions in Local Time:

Sydney: 10:00 - 16:00

Tokyo: 09:00 - 15:00

Shanghai: 09:30 - 15:00

Asia: 00:00 - 06:00

Europe: 07:00 - 16:30

London: 08:00 - 16:30

New York: 09:30 - 16:00

🟣 TFlab Suggestion Mode

• Sessions in UTC (DST inactive) :

Sydney: 23:00 - 05:00

Tokyo: 00:00 - 06:00

Shanghai: 01:00 - 09:00

Asia: 23:00 - 06:00

Europe: 07:00 - 16:00

London: 08:00 - 16:00

New York: 13:00 - 21:00

• Sessions in UTC (DST active) :

Sydney: 22:00 - 04:00

Tokyo: 00:00 - 06:00

Shanghai: 01:00 - 09:00

Asia: 22:00 - 06:00

Europe: 06:00 - 15:00

London: 07:00 - 15:00

New York: 12:00 - 20:00

• Sessions in Local Time :

Sydney: 09:00 - 16:00

Tokyo: 09:00 - 15:00

Shanghai: 09:00 - 17:00

Asia: 23:00 - 06:00

Europe: 07:00 - 16:00

London: 08:00 - 16:00

New York: 08:00 - 16:00

🔵 Setting

Using the session indicator is straightforward and practical. Users can add this indicator to their trading chart and take advantage of its features.

The usage steps are as follows :

Selecting Market Mode : The user can choose one of the three main modes.

Forex Market Mode: Displays the forex market trading hours.

oStock Market Mode: Displays the trading hours of stock exchanges.

Custom Mode: Allows the user to set trading hours based on their needs.

TFlab Suggestion Mode: Displays the higher volume hours of the forex market in Asia.

Setting the Time Zone : The indicator allows displaying sessions based on various time zones. The user can select one of the following options:

UTC (Coordinated Universal Time)

Local Time of the Session

User’s Local Time

Displaying Comprehensive Session Information : The session information table includes the opening and closing times of each session and whether they are open or closed. This table helps users monitor all sessions at a glance and precisely set the best time for entering and exiting trades.

🔵Conclusion

The session indicator is a highly efficient and essential tool for active traders in the FOREX and stock markets. With its unique features, such as automatic DST detection and the ability to display sessions based on different time zones, the session indicator helps traders to precisely and efficiently adjust their trading activities.

This indicator not only shows users the exact opening and closing times of sessions, but by providing a session status table, it helps traders identify the best times to enter and exit trades. Moreover, the ability to set custom trading times allows traders to easily personalize their trading schedules according to their strategies.

In conclusion, using the session indicator ensures that traders are continuously and accurately informed of time changes and the opening and closing hours of markets, eliminating the need for manual updates to align with DST changes. These features enable traders to optimize their trading strategies with greater confidence and up-to-date information, allowing them to capitalize on opportunities in the market.

New York, London and custom trading sessionsHi Traders

The script :

The Time sessions script plots the trading sessions of both New York and London markets (background fills), In addition to the above the script also plots a user defined trading session period (vertical lines). All plots may be toggled true or false inorder to ensure you can focus on the respective market / markets / custom session.

Market sessions are useful for technical or quantitative analysis, as the majority of trading activity and net daily volume occurs in these zones, in fact the U.S./London market overlap tends to have the greatest volume accumulation across that range of time / bars than that range at any other time within the daily session. For FX traders it may also be important to take into account for many currency pairs the average exchange rate pip movement is greatest within these zones.

The custom session, is intended to be used for traders who trade only within specific intervals within the market session or day for 24/7 traded asset classes

Additional notes :

Not as of now, I have only added three optional trading sessions. If you would like to change the sessions, copy the scripts code and change the "ctm_session" default time range value, insuring the second time value is 1 min > than the first.

As always i Hope this is a useful script, and I will be updating this script in the near future.

[MiV] Trading SessionHello, everyone!

Today I want to present my new script, which I hope will help not only me!

I'm sure that many people, like me, went through such a stage as "building their strategy". This is when you sit and test on the history how you would enter or exit a trade.

Recently I was doing the same thing and realized that my "tests" involve night time, when in reality I would be asleep and not trading! So I decided to create an indicator that would display my "working hours" so that the backtest I conduct would be as realistic as possible.

Also this indicator is able to display sessions of major exchanges and forex working hours, so it will be useful not only for cryptocurrency lovers.

In addition, we don't always trade every day and, for example, I don't trade on Sunday. That's why we added a feature that "turns off" the day and does not highlight it in color if you're not planning to trade on that day.

And finally, I added a notification of the beginning and end of the trading session. A small thing, but it may also be a useful feature for those who like to sit at the chart!

I will be glad to receive any comments and suggestions!

-----

Всем привет!

Хочу сегодня представить свой новый скрипт, который, надеюсь, поможет не только мне!

Уверен, что многие, как и я, проходили такой этап как "постройка своей стратегии". Это когда ты сидишь и тестируешь на истории то как бы ты входил или выходил из сделки.

Вот недавно я ровно также занимался этим и осознал, что мои "тесты" затрагивают и ночное время, когда в реальности я бы спал и не торговал! Поэтому я решил создать индикатор, который будет отображать мои "рабочие часы", чтобы бектест, который я провожу, был максимально реалистичным.

Также данный индикатор умеет отображать сессии крупных бирж и время работы форекса, так что полезным он будет не только для любителей криптовалюты.

Кроме того, мы же не всегда торгуем каждый день и например я не торгую в воскресенье. Поэтому добавлен функционал, который "выключает" день и не подсвечивает его цветом, если ты в этот день не планируешь торговать.

Ну и в заключении, добавил уведомление о начале и завершении торговой сессии. Мелочь, а тоже может быть полезной фичей для тех кто любит засесть за графиком!

Буду рад любым замечаниям и предложениям!

Custom Trading Session HighlighterThe Custom Trading Session Highlighter is a simple yet powerful indicator that allows you to visualize specific trading sessions on your chart by highlighting the background within the specified time range. This indicator can be helpful for traders who want to focus on specific market hours or analyze the market behavior during certain time periods.

Features:

>Customizable start and end times: Input your desired trading session start and end times using the format "HHMM" (e.g., "0930" for 9:30 AM). The indicator allows you to select the time range in 30-minute intervals.

>Trading session background color: The specified trading session will be highlighted with a semi-transparent green color, making it easy to differentiate the session from the rest of the chart.

>Overlay: The indicator overlays on the price chart, so it doesn't take up any additional space on your screen.

How to use:

>Add the Custom Trading Session Highlighter to your chart.

>Configure the start and end times of the session you want to highlight using the input fields in the indicator settings.

>Observe the highlighted trading session on your chart to analyze market behavior within that specific time range.

Regular Trading Hour Sessions for America, Asia and EUThis trading view script is a simple one but I find it very helpful in spotting changes in trend of FX.

The basic idea is to create a visual direction from the previous session to the next new session.

The concept while basic provides visual trend direction and changes as session change.

The three sessions are:

1. Asia from 2130-0400

2. Europe from 0300-1130

3. America from 0930-1600

When you use a line chart you will see the default line when no sessions are active.

Features I plan to add

* Tracking delta of each session

* Moving Averages of each session

* Momentum of each session

* Delta difference

My ultimate goal for this script will be to provide a way to visualize the impact of each session and provide data to buy/sell triggers for Trading Strategies.

Please provide feedback and if you use the script or add a feature please update me or send me the feature to add to the script.

Market Sessions - By LeviathanA simple indicator to help you keep track of 4 market sessions (default: Tokyo, London, New York, Sydney) in 4 different visual forms (boxes, timeline, zones, colored candles) with many other useful tools.

You can choose between 4 different market sessions. The default ones are Tokyo, London, New York and Sydney but you can easily customize the times, names and colors to make the script plot any session you need. Sessions can be viewed in 4 different ways: boxes, zones, timelines, or just colored candles, all with customizable appearances. You can make your chart cleaner by merging sessions overlaps, choosing a custom lookback period and also picking between various additional settings such as viewing session High/Low or Open/Close change in % or pips, hiding weekends, viewing the Open/Close Line to identify session’s direction and 0.5 level to see session’s “Equilibrium” and much more. More updates with interesting tools will be added in the future.

Note: The script will plot the correct default Tokyo, London, New York and Sydney sessions automatically, your chart/Tradingview app timezone does not matter! If you wish to tweak the open/close times of sessions, just make sure you input them in UTC (but even this can be changed later in the settings)

Settings Overview

SESSIONS

- You can show/hide Tokyo Session, rename it, change the color and set up start/end time.

- You can show/hide London Session, rename it, change the color and set up start/end time.

- You can show/hide New York Session, rename it, change the color and set up start/end time.

- You can show/hide Sydney Session, rename it, change the color and set up start/end time.

* Keep in mind that you can fully change and customize these sessions and therefore create any other sessions or a zone you wish to display.

ADDITIONAL TOOLS AND SETTINGS

1. “Change (Pips)” - this will add the pip distance between Session High and Session Low or the pip distance between Session Open and Session Close to the session label.

2. “Change (%)” - this will add the percentage distance between Session High and Session Low or the percentage distance between Session Open and Session Close to the session label.

3. “Merge Overlaps” - this will merge the overlapping sessions and show only one at a time (end of Tokyo is moved to start of London, the end of London is moved to the start of New York, end of New York is moved to start of Sydney and end of Sydney is moved to start of Tokyo).

4. “Hide Weekends” - this will prevent the script from plotting sessions over the weekend when the markets are closed.

5. “Open/Close Line” - this will draw a line from the session open to the session close (or current price, if session is ongoing).

6. “Session 0.5 Level” - this will draw a horizontal line halfway between the session’s high and the session’s low.

7. “Color Candles” - this will color the bars/candlesticks with the color of the session in which they occurred.

8. Display Type” - Choose between three different ways of session visualization (Boxes, Zones and Candles).

9. “Lookback (Days)” - this input tells the script to only draw sessions for X days back (1 = one day).

10. “Change (%/Pips) Source) - this is where you choose the source of “Change (Pips)” and ”Change (%) ” labels. Picking “Session High/Low” will show you the change between Session High and Session Low and picking “Session Open/Close” will show you the change between Session Open and Session Close.

11. “Input Timezone” - this defines the timezone of the session start/end inputs (you don’t have to change this unless you know what you’re doing)

Make sure to read future update logs to keep track of the most recent additions and settings of this script.

Box generation code inspired by Jos(TradingCode), session box visuals inspired by @boitoki's FX Market Sessions

Sessions [LuxAlgo]This indicator shows when user set sessions are active and returns various tools + metrics using the closing price within active sessions as an input. Users have the option to change up to 4 session times.

The indicator will increasingly lack accuracy when the chart timeframe is higher than 1 hour.

Settings

Sessions

Enable Session: Allows to enable or disable all associated elements with a specific user set session.

Session Time: Opening and closing times of the user set session in the hh:mm format.

Range: Highlights the associated session range on the chart.

Trendline: Returns the associated session trendline on the chart.

Mean: Returns the associated session mean average on the chart.

VWAP: Returns the associated session volume weighted average price on the chart.

Ranges Settings

Range Area Transparency: Transparency of the area highlighting sessions ranges.

Range Outline: Highlights the borders of the session range area.

Range Label: Shows the session label at the mid-point of the session interval.

Dashboard

Show Dashboard: Enables sessions dashboard on the chart.

Advanced Dashboard: Returns more information regarding user set sessions on the dashboard.

Dividers

Show Session Divider: Highlights active sessions using intervals on the bottom of the chart (this can lead to less responsive charts)

Show Daily Divider: Highlights days on the chart.

Usage

This tool is versatile and allows the user to perform a wide variety of tasks all focusing on highlighting and analyzing price movements within a specific user set session in a periodic fashion.

Significant forex trading sessions are used by default, but the users are free to choose the opening and closing time of their choices.

Using ranges can indicate which sessions returned the most volatile price movements.

Trendlines can be useful to estimate the underlying trend of a specific session, but they can also offer a quick way to see which session started a trend reversal.

The session Mean highlights the equilibrium level within a session, extrapolating these levels can provide potential support and resistances levels of interest.

Finally, users can use the sessions VWAP's for real time applications, using them as trailing supports and resistances.

Using The Advanced Dashboard

The advanced dashboard returns useful information regarding the user set sessions. Each dashboard elements are described below:

Status: Highlights whether the user set session is active (open) of inactive (closed).

Trend: Shows correlation coefficient between the session prices and a linear sequence of values. Values above 0 indicates an up-trending session, while values under 0 indicates a down-trending session. Values closer to (1, -1) indicates a more trending session.

Volume: Shows accumulated volume within the session

σ (Standard Deviation): Shows standard deviation of the session, while this value is not bounded it can be useful to compare it with the other ones to see which session was the most volatile.

Note that when a session becomes inactive the value on the dashboard will hold until the specific session becomes active again.

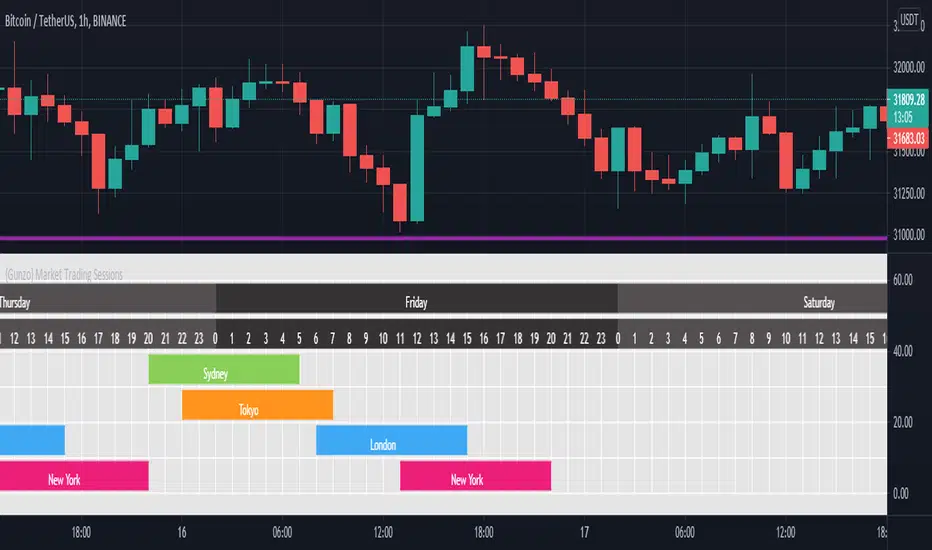

Market Trading Sessions (TG Fork)Visualize trading sessions opening hours of several international exchanges on a grid. Contrary to other indicators, this one automatically aligns the session with the current chart's timezone.

This is helpful for bar replay or manual backtesting, to spot patterns of correlations (this can also be used in conjunction with correlation indicators, see my other indicators).

Original indicator by Gunzo, if you like this indicator, please show the original author some love:

This indicator is also inspired by the following indicators:

ZenAndTheArtOfTrading with

UnknownUnicorn468659 with

This fork implements the following features:

Converted to PineScript v5.

Adapted default color palette to dark mode, as is the default in TradingView now.

Fix drawing issues, now the design shows as it was originally meant to be.

Fixed mistiming issue that made some sessions display with a delay compared to the real session, especially the first session was bar at the start of the session was not displayed.

Inputted the accurate timings for each session, instead of the default 0800-1600 in the original indicator.

Essentially, you can just add this indicator and it should work out of the box. If not, please let me know, and I'll try to fix it!

{Gunzo} Market Trading Sessions (Tokyo, London, New York)Market Trading Sessions is a tool designed to help traders to find the best times of the day for price action trading. It displays non-overlapping visuals for the major trading sessions : Oceania, Asia, Europe, and USA.

OVERVIEW :

This tool has been designed to match all the following requirements that I needed for optimal usage :

Display opening and closing of main markets

See clearly market sessions (non-overlapping colors)

Display Sydney session if wanted

Display GMT hours and days

Visually pleasing design and colors

Highly configurable

As I had trouble finding a script matching all these criteria, I created this tool and I'm sharing it with the TradingView community, hoping you will find it useful too.

SETTINGS :

Display market sessions on weekends : Display theoretical market sessions times on the weekend which can be useful for non forex markets.

Display session for Oceania\Sydney : Display "Oceania\Sydney" trading session

Display session for Asia\Tokyo : Display "Asia\Tokyo" trading session

Display session for Europe\London : Display "Europe\London" trading session

Display session for USA\New York : Display "USA\New York" trading session

Display session names : Display names of the session on the visual

Oceania color : Configurable color for the "Oceania\Sydney" sessions

Asia color : Configurable color for the "Asia\Tokyo" sessions

Europe color : Configurable color for the "Europe\London" sessions

USA color : Configurable color for the "USA\New York" sessions

Background color : Configurable color for the table background

Border color : Configurable color for the table borders

Text color : Configurable color for the table text

Header color : Configurable color for the table header (even days)

Header color (alternate) : Configurable color for the table header (odd days)

Session Volatility CalculatorHey traders!

This script calculates the average volatility of trading sessions.

You specify a start date, an end date, and a session time (eg. market open, Asian session etc)

The script then scans through all the price action on your chart and calculates the average price movement during that specified period.

What Is It For?

I created this script for my own purposes when developing certain strategies and testing certain ideas.

The purpose of this script is to give you an idea of how much price tends to move during certain times of day for certain markets.

You could think of it as a "session's average true range".

In crypto and forex this might be how much price tends to move on certain pairs during the Australian/Asian session, or the European session, or the overnight U.S. session etc.

In stocks this might be how much a symbol tends to move during the first hour of the day or the last hour of the day.

The point of calculating this information is for better understanding how markets move during certain times of day.

It's not a perfect science obviously since some days can be wilder than others depending on what fundamental events are developing, but it's useful information to have for times when there are no expected volatility-inducing events.

This info can help with optimizing targets and stop loss placement for certain day-trading strategies, and just generally getting an idea of what kinds of moves you might reasonably expect out of overnight positions or certain times of day etc - or at least that's what I use it for.

Settings

Hover your mouse over the "i" symbol to get more information on the script's settings, but here's a brief description:

Start Date: The date to begin calculating from (set to 1000 by default so it scans the entire chart).

End Date: The date to stop calculating (set to 2099 by default so it scans the entire chart)

Time Session: This is the time session during the day that you want to analyze.

Color Background: If turned on, this setting changes the background color to highlight the session.

Indicator Values

The indicator outputs a handful of values onto your chart. This is what the colors correspond to:

Top-Right Box: The average price range during the given time of day over historical price action.

Green Number: The recent session's highest price.

Red Number: The recent session's lowest price.

Purple Number: The recent session's price range (high - low).

Orange Number: The recent session's range ÷ the average (outputs a relative % of the average).

Forex/Crypto/Custom Market SessionsCredit goes to TradeMasterSavis for providing the original code

I merge the 2 sessions together allowing you to toggle between the two. I also add a 3rd custom session type and the ability to change the duration of each trading session. This would solve any problems ran into the case of Daylight savings time switch or if you just want different session duration.