OPEN-SOURCE SCRIPT

[-_-] Level Breakout, Auto Backtesting Strategy

Description:

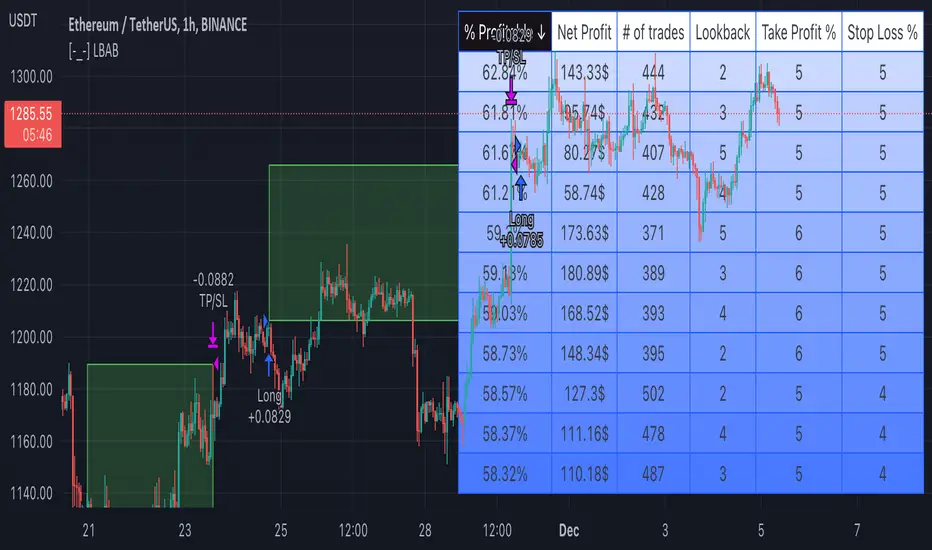

A Long only strategy based on breakout from a certain level formed by High price. It has auto-backtesting capabilities (you set ranges for the three main parameters: Lookback, TP and SL; the strategy then goes through different combinations of those parameters and displays a table with results that you can sort by Percentage of profitable trades AND/OR Net profit AND/OR Number of trades). So you can, for example, sort only by Net profit to find combination of parameters that gives highest net profit, or sort by Net profit and Percentage profitable to find a combination of parameters that gives the best balance between profitability and profit. The auto-backtesting also takes into account the commission which is set in % in the inputs (make sure to set the same value in properties of the strategy so that auto-backtesting and real backtesting results match).

NOTE: auto-backtesting only find the best combinations and displays them in a table, you will then need to manually set the Lookback, TP and SL inputs for real backtesting to match.

Parameters:

- Lookback -> # of bars for filtering signals; recommended range from 2 to 5

- TP (%) -> take profit; recommended range from 5 to 10

- SL (%) -> stop loss; recommended range from 1 to 5

- Commission (%) -> commission per trade

- Min/Max Lookback -> lookback range for auto-backtesting

- Min/Max TP -> take profit range for auto-backtesting

- Min/Max SL -> stop loss range for auto-backtesting

- Percentage profitable -> sort by percentage of profitable trades

- Net profit -> sort by net profit

- Number of trades -> sort by number of trades

A Long only strategy based on breakout from a certain level formed by High price. It has auto-backtesting capabilities (you set ranges for the three main parameters: Lookback, TP and SL; the strategy then goes through different combinations of those parameters and displays a table with results that you can sort by Percentage of profitable trades AND/OR Net profit AND/OR Number of trades). So you can, for example, sort only by Net profit to find combination of parameters that gives highest net profit, or sort by Net profit and Percentage profitable to find a combination of parameters that gives the best balance between profitability and profit. The auto-backtesting also takes into account the commission which is set in % in the inputs (make sure to set the same value in properties of the strategy so that auto-backtesting and real backtesting results match).

NOTE: auto-backtesting only find the best combinations and displays them in a table, you will then need to manually set the Lookback, TP and SL inputs for real backtesting to match.

Parameters:

- Lookback -> # of bars for filtering signals; recommended range from 2 to 5

- TP (%) -> take profit; recommended range from 5 to 10

- SL (%) -> stop loss; recommended range from 1 to 5

- Commission (%) -> commission per trade

- Min/Max Lookback -> lookback range for auto-backtesting

- Min/Max TP -> take profit range for auto-backtesting

- Min/Max SL -> stop loss range for auto-backtesting

- Percentage profitable -> sort by percentage of profitable trades

- Net profit -> sort by net profit

- Number of trades -> sort by number of trades

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。