OPEN-SOURCE SCRIPT

已更新 Fractal Regression Bands [DW]

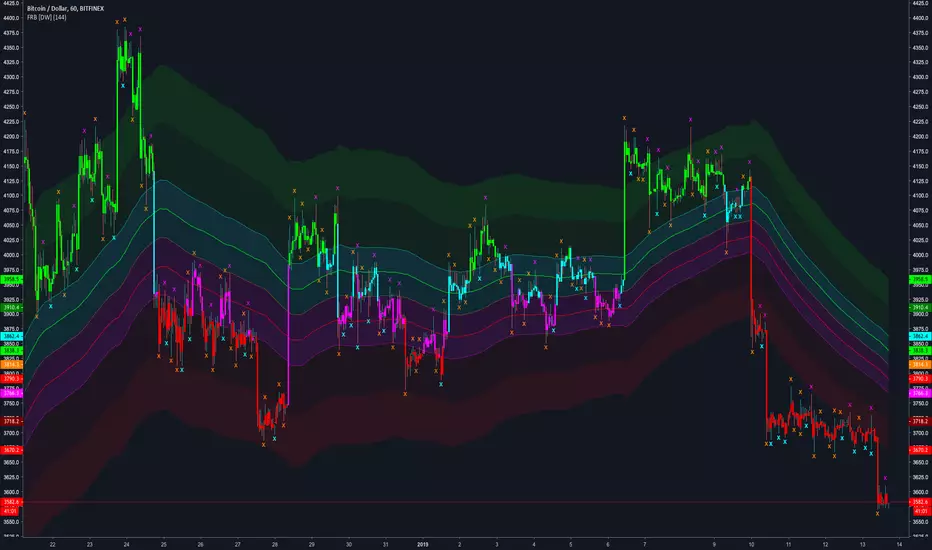

This study is an experimental regression curve built around fractal and ATR calculations.

First, Williams Fractals are calculated, and used as anchoring points.

Next, high anchor points are connected to negative sloping lines, and low anchor points to positive sloping lines. The slope is a specified percentage of the current ATR over the sampling period.

The median between the positive and negative sloping lines is then calculated, then the best fit line (linear regression) of the median is calculated to generate the basis line.

Lastly, a Golden Mean ATR is taken of price over the sampling period and multiplied by 1/2, 1, 2, and 3. The results are added and subtracted from the basis line to generate the bands.

Williams Fractals are included in the plots. The color scheme indicated whether each fractal is engulfing or non-engulfing.

Custom bar color scheme is included.

First, Williams Fractals are calculated, and used as anchoring points.

Next, high anchor points are connected to negative sloping lines, and low anchor points to positive sloping lines. The slope is a specified percentage of the current ATR over the sampling period.

The median between the positive and negative sloping lines is then calculated, then the best fit line (linear regression) of the median is calculated to generate the basis line.

Lastly, a Golden Mean ATR is taken of price over the sampling period and multiplied by 1/2, 1, 2, and 3. The results are added and subtracted from the basis line to generate the bands.

Williams Fractals are included in the plots. The color scheme indicated whether each fractal is engulfing or non-engulfing.

Custom bar color scheme is included.

發行說明

Updates:Due to inefficiencies and its arbitrary nature, the slope factor calculation has been removed from the script.

Due to the linear regression's significant amount of overshoot, especially at greater sampling lengths, the basis line is now calculated using exponential smoothing, which fits the price series much better with minimal overshoot.

Changed the size of the fractal signals.

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

For my full list of premium tools, check the blog:

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

For my full list of premium tools, check the blog:

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。