OPEN-SOURCE SCRIPT

已更新 Project Synth

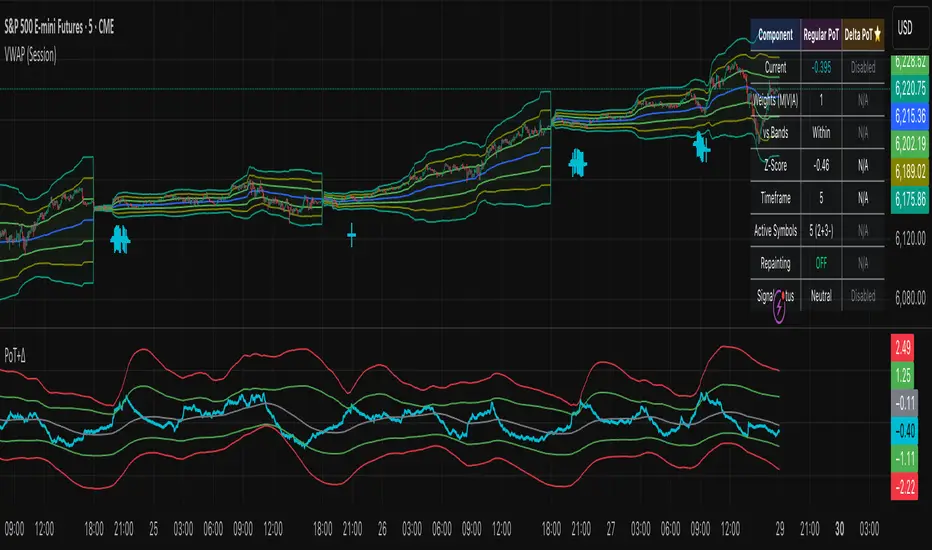

Introducing Project Synth!

Inspired by Pace of Tape and Cumulative Delta I created Project Synth in order to aggregate volume flow data across multiple marketsfor two primary reasions:

Some more detailed explanations (using QQQ and SQQQ as an example):

Inverse Market Dynamics (QQQ vs SQQQ):

Why Utilizing Both Markets Provides A More Accurate Delta:

Multiple Markets = Authentic Pressure:

My Suggestions For Usage:

Notes For Moderators, Authors and Users:

Inspired by Pace of Tape and Cumulative Delta I created Project Synth in order to aggregate volume flow data across multiple marketsfor two primary reasions:

- Traditional orderflow tools are not available on Tradingview. My script attempts to bring an original; calculus-based approach to creating not only an alternative for traditional orderflow tools, but also a more accurate one.

- In order to detect genuine buying and selling pressure that cannot be easily manipulated. I did this because while I've always enjoyed concept behind both of those tools, I did not think they captured enough data to be useful. By analyzing assets that move together (positive correlation) and assets that move inversely (negative correlation), my system aims to fix the fundamental problems with those indicators and create an objective view of market sentiment based on aggregate orderflow.

Some more detailed explanations (using QQQ and SQQQ as an example):

Inverse Market Dynamics (QQQ vs SQQQ):

- In an inverse market like SQQQ, aggressive buyers hit the ask when they expect the underlying (QQQ) to fall, while passive buyers wait on the bid hoping for cheaper inverse exposure. When QQQ rallies, SQQQ sees aggressive selling (people dumping their bearish bets) hitting bids, while passive sellers sit on the ask hoping to exit at better prices. The aggression flows opposite to the underlying market direction.

Why Utilizing Both Markets Provides A More Accurate Delta:

- Watching both QQQ and SQQQ gives cross-validation - real buying pressure in QQQ should coincide with selling pressure in SQQQ. If you see buying in QQQ but also buying in SQQQ, that's a conflicting signal suggesting the move might be artificial or driven by other factors. The inverse relationship acts as a confirmation filter, making false signals much harder to generate.

Multiple Markets = Authentic Pressure:

- The more unique, important markets you track, the harder it becomes to create fake delta moves. Real institutional buying/selling pressure affects multiple correlated assets simultaneously in predictable patterns - you can't easily manipulate tech stocks, treasury bonds, VIX, and currency pairs all at once to create a false signal. Each additional market acts as a fraud detection layer, ensuring the delta measurement reflects genuine ecosystem-wide buying and selling pressure rather than isolated manipulation or noise.

My Suggestions For Usage:

- In order to keep the explanation simple and short for now, I suggest using it just like a cumulative delta indicator. For example: let's say you were watching

ES1!, and you had a resistance level at 6000. When the price reaches your resistance level, you would be looking for a significant divergence between price and Delta. Price : rising, Delta : falling. This means that even though the price was going up, strong and aggressive sellers are jumping in more and more, this can be used as a confirmation tool for a resistance level.

ES1!, and you had a resistance level at 6000. When the price reaches your resistance level, you would be looking for a significant divergence between price and Delta. Price : rising, Delta : falling. This means that even though the price was going up, strong and aggressive sellers are jumping in more and more, this can be used as a confirmation tool for a resistance level.

Notes For Moderators, Authors and Users:

- Firstly, to the best of my knowledge, I have not been able to find many tools built around the concept of cumulative delta or pace of tape. While I know there are a couple projects, none to the magnitude of synthetically recreating these tools via an algorithm designed around basic calculus principles. While tools like Volume Delta are built in, they do not attempt to capture an accurate picture of aggregated orderflow from what I understand.

- Secondly, it needs to be noted that tool aims to create an approximation of buying and selling pressure. To my knowledge it is not possible to create an accurate full picture, at least not within the limitations of Tradingview.

發行說明

Just fixing some typos on the settings menu, no changes in functionality. 發行說明

IMPORTANT! Huge update for project synth: the pace of tape setting was not setup properly. I pretty much just reused the delta settings for it, it's been given a complete overhaul on how its calculations and settings work, giving you a proper guage of the current pace of the market. Even if you don't use it for signals, just knowing what the current pace is gives you a clear picture on if the market is active or not. You can pull it up for yourself and see that when the pace is low, the market is almost always consolidating. - Pace of tape is now measured by momentum (magnitude of volume * velocity, where velocity is the rate of change of volume).

- Signals are better adjusted so that you're able to get more valuable information from pace of tape.

- Added a 'halt signals' mode, instead of misrepresenting low volume as being "bearish", you can enable halt mode to show you when volume has dried up.

- Removed references of volume serving as a vector for price's direction, instead it'll now give you the literal pace of the market.

發行說明

- Not a major update, just setting it so it defaults to pace of tape instead of delta.We are finding pace of tape is pretty interesting, the debate of delta is better versus pace of tape is better seems to depend on the market and the weights of the correlations.

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。