Displacement [QuantVue]Displacement refers to a significant and forceful price movement that indicates a potential shift in market sentiment or trend. Displacement is characterized by a strong push in price action, often seen after a period of consolidation or within a trending market. It is a key concept used to identify the strength of a move and to confirm the direction of the market.

The "Displacement" indicator does this by focusing on identifying strong, directional price movements by combining candlestick analysis with volatility (ATR).

Displacement often appears as a group of candles that are all positioned in the same direction, these candles typically have large bodies and short wicks.

How the indicator works:

Body Size Requirement: Ensures that only candles with a significant body size (relative to their total range) are considered, helping to identify strong market moves.

Consecutive Candle Analysis: Identifies shifts in market sentiment by requiring a series of consecutive bullish or bearish candles to confirm a potential change in trend.

ATR-Based Analysis: Uses the Average True Range (ATR) to gauge market volatility and filter out minor price fluctuations, focusing on substantial movements.

Once all of the requirements are met a triangle is plotted above or below the bar.

真實波幅均值(ATR)

Balance of Power [Pinescriptlabs]Balance of Power Indicator ⚖️

The Balance of Power Indicator is a visual tool that illustrates the power dynamics between buyers and sellers by analyzing recent price action. Instead of providing direct buy or sell signals, this indicator shows how the tilt of a symbolic scale reflects the relative strength of both parties. The calculation is based on the difference between the current closing price and the closing price from a specific number of periods (defined by the user), adjusted for market volatility measured by the ATR (Average True Range).

Tilt Value Interpretation:

• Positive Tilt (0 to 1) 📈:

o A tilt value close to 1 indicates significant control by buyers. The current price is well above the average adjusted for recent volatility. Practically, a tilt in the range of 0.50 to 1 suggests buyers are pushing the price above the average volatility, signaling a strong bullish trend.

•

o

• Negative Tilt (-1 to 0) 📉:

o A tilt value close to -1 indicates significant control by sellers. The current price has dropped notably compared to the average adjusted for recent volatility. A tilt in the range of -0.50 to -1 suggests sellers are dominating, with the price falling below the average volatility, reflecting a strong bearish trend.

o

Neutral:

Indicator Sensitivity:

The number of periods analyzed affects the sensitivity of the indicator:

• Shorter Periods: Make the indicator respond more quickly to price changes.

• Longer Periods: Smooth out the tilt, providing a more stable view of market forces.

Visualizing Relative Power:

The balance not only shows the general direction of power between buyers and sellers but also the intensity of this pressure. By adding more small balances, the indicator visually represents greater strength in the corresponding direction. Thus, the Balance of Power provides an overview of the balance between supply and demand, and allows for a visual assessment of the magnitude of that pressure based on the scale’s tilt.

Español

Indicador de Balance de Poder ⚖️

El Indicador de Balance de Poder es una herramienta visual que ilustra la dinámica de poder entre compradores y vendedores mediante el análisis de la acción reciente del precio. En lugar de proporcionar señales directas de compra o venta, este indicador muestra cómo la inclinación de una balanza simbólica refleja la fuerza relativa de ambas partes. El cálculo se basa en la diferencia entre el precio de cierre actual y el precio de cierre de un número específico de períodos (definidos por el usuario), ajustado por la volatilidad del mercado medida por el ATR (Average True Range).

#### **Interpretación del Valor de Tilt(inclinación):**

- Tilt Positivo (0 a 1) 📈:

- Un valor de inclinación cercano a **1** indica un control significativo por parte de los compradores. El precio actual está muy por encima del promedio ajustado por la volatilidad reciente. En términos prácticos, un tilt en el rango de **0.50 a 1** sugiere que los compradores están impulsando el precio por encima de la volatilidad promedio, señalando una fuerte tendencia alcista.

- **Tilt Negativo (-1 a 0) 📉:**

- Un valor de inclinación cercano a **-1** indica un control significativo por parte de los vendedores. El precio actual ha caído notablemente en comparación con el promedio ajustado por la volatilidad reciente. Un tilt en el rango de **-0.50 a -1** sugiere que los vendedores están dominando, con el precio cayendo por debajo de la volatilidad promedio, reflejando una fuerte tendencia bajista.

- **Neutral:**

**Sensibilidad del Indicador:**

El número de períodos analizados afecta la sensibilidad del indicador:

- **Períodos más cortos:** Hacen que el indicador responda más rápidamente a los cambios en el precio.

- **Períodos más largos:** Suavizan la inclinación, proporcionando una visión más estable de las fuerzas del mercado.

#### **Visualización del Poder Relativo:**

La balanza no solo muestra la dirección general del poder entre compradores y vendedores, sino también la intensidad de esta presión. Al agregar más pequeñas balanzas, el indicador representa visualmente una mayor fuerza en la dirección correspondiente. Así, el **Balance de Poder** proporciona una visión general del equilibrio entre oferta y demanda y permite una evaluación visual de la magnitud de esa presión basada en la inclinación de la balanza.

Wedge Pop & Drop [QuantVue]A "Wedge Pop" is a trading pattern popularized by Oliver Kell, a notable trader who won the 2020 US Investing Championship with a remarkable return of 941%. This pattern, often referred to as "The Money Pattern" in his trading strategy, serves as a critical signal indicating the beginning of a new uptrend in a stock.

A Wedge Pop occurs when a stock first trades up through the moving averages after reaching a downside extension. Conversely, a Wedge Drop refers to the first time a stock trades down through the moving averages after reaching an upside extension.

How the Indicator Works:

The indicator uses the Average True Range (ATR) and the 10-period Exponential Moving Average (10 EMA) to identify upside and downside extensions. An upside extension occurs when the low of the current bar is greater than 1.5 (default) times the ATR above the moving average. A downside extension occurs when the high of the current bar is less than 1.5 times the ATR below the moving average.

Once an extension has been reached, the first time the security trades back through the moving averages, it triggers a Wedge Pop/Drop.

Give this indicator a BOOST and COMMENT your thoughts below!

We hope you enjoy.

Cheers!

Volumetric Volatility Blocks [UAlgo]The Volumetric Volatility Blocks indicator is designed to identify significant volatility blocks based on price and volume data. It utilizes a combination of the Average True Range (ATR) and Simple Moving Average (SMA) to determine the volatility level and identify periods of heightened market activity. The indicator highlights these volatility blocks, providing traders with visual cues for potential trading opportunities. It differentiates between bullish and bearish volatility by analyzing price movement and volume, offering a nuanced view of market sentiment. This tool is particularly useful for traders looking to capitalize on periods of high volatility and momentum shifts.

🔶 Key Features

Volatility Measurement Length: Controls the period used to calculate the ATR.

Smooth Length of Volatility: Defines the period for the SMA used to smooth the ATR.

Multiplier of SMA: Sets the minimum threshold for the ATR to be considered a "high volatility" block.

Show Last X Volatility Blocks: Determines how many of the most recent volatility blocks are displayed on the chart.

Mitigation Method: Choose between "Close" or "Wick" price to filter volatility blocks based on price action. This helps avoid highlighting blocks broken by the chosen price level.

Volume Info: Displaying the volume associated with each block.

Up/Down Block Color: Sets the color for bullish and bearish volatility blocks.

🔶 Usage

The Volumetric Volatility Blocks indicator visually represents periods of high volatility with blocks on the chart. Green blocks indicate bullish volatility, while red blocks indicate bearish volatility.

Bullish Volatility Blocks: When the ATR surpasses the smoothed ATR multiplied by the set multiplier, and the price closes higher than it opened, a bullish block is formed. These blocks are generally used to identify potential buying opportunities as they indicate upward momentum.

Bearish Volatility Blocks: Conversely, bearish blocks form under the same conditions, but when the price closes lower than it opened. These blocks can signal potential selling opportunities as they highlight downward momentum.

Volume Information: Each block can display volume data, providing insight into the strength of the market movement. The percentage shown on the block indicates the relative volume contribution of that block, helping traders assess the significance of the volatility.

The volume percentages in the Volumetric Volatility Blocks indicator are calculated based on the total volume of the most recent volatility blocks. For each of the most recent volatility blocks, the percentage of the total volume is calculated by dividing the block's volume by the total volume:

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

ATR X-PowerATR X-Power is a simple graphical representation of Average True Range.

The ATR is calculated on a daily basis and averaged over the "Length" specified in settings (default is 14 days).

At the start of the day, the starting price is recorded and five horizontal lines are drawn which illustrate possible ranges for the day:

Starting price

Starting price + ATR (+100%)

Starting price - ATR (-100%)

Starting price + ATR/2 (+50%)

Starting price - ATR/2 (-50%)

The final two lines are drawn using the ATR half values in such a way that a X is formed. The X represents possible motion of the price back to starting price (also known as reversion to mean). The two lines are drawn as follows:

Beginning at (Starting Price + ATR/2) and ending at (Starting Price - ATR/2)

Beginning at (Starting Price - ATR/2) and ending at (Starting Price + ATR/2)

Use cases:

ATR presents us with the average amount of price fluctuation we can expect to see in a single day on a specific instrument

If price is near the extremes (+/-100% ATR) for the day, then probability of it moving outside that range is low, which increases odds of a reversal

Bugs?

Kindly report any issues you run into and I'll try to fix them promptly.

Thank you!

Chieu - Bollinger Bands SMA 50 StrategyOverview

The Custom Bollinger Bands Indicator is a versatile tool designed to help traders identify potential market reversals and optimize their trading strategies. This indicator combines Bollinger Bands with an ATR-based stop-loss mechanism, configurable take-profit levels, and dynamic position sizing to manage risk effectively. By highlighting key market conditions and providing clear visual cues, it enables traders to make informed decisions and execute trades with precision.

Key Features

Bollinger Bands Calculation:

The indicator calculates Bollinger Bands based on a configurable Simple Moving Average (SMA) length.

Standard deviation multiplier is adjustable, allowing traders to fine-tune the width of the bands.

Candlestick Highlighting:

Candles that touch the upper or lower Bollinger Bands are highlighted, indicating potential overbought or oversold conditions.

Reversal candles are identified and highlighted based on specific criteria:

The candle must touch the Bollinger Bands for two consecutive periods.

The reversal candle must have a body at least twice the size of the previous candle's body.

The reversal candle must close in the opposite direction to the previous candle (e.g., a bullish candle following a bearish one).

Stop-Loss and Take-Profit Levels:

Stop-loss levels are calculated using the ATR (Average True Range) indicator, ensuring they are dynamically adjusted based on market volatility.

Two configurable take-profit levels (1R and 2R) are plotted based on the initial risk (distance between entry and stop-loss).

Take-profit and stop-loss lines are visually represented on the chart for easy reference.

Position Sizing and Risk Management:

The indicator includes configurable inputs for account balance, leverage, and risk percentage.

It calculates the nominal value (position size without leverage) and cost value (position size with leverage) based on the specified risk parameters.

Combined labels display SL, TP, nominal value, and cost value, replacing the default "Reversal" text for clear, concise information.

Customization Options:

Users can configure the length of the take-profit lines.

The option to toggle the highlighting of candles touching the Bollinger Bands on or off, while always highlighting the identified reversal candles.

How to Use

Configuration:

Set the desired SMA length and Bollinger Bands multiplier in the input settings.

Configure the ATR length for accurate stop-loss calculations.

Adjust the risk-reward ratio and take-profit line length according to your trading strategy.

Specify your account balance, leverage, and risk percentage for precise position sizing.

Chart Analysis:

Monitor the chart for candles touching the upper or lower Bollinger Bands. These highlights indicate potential overbought or oversold conditions.

Look for highlighted reversal candles, which meet the specified criteria and suggest a potential market reversal.

Use the plotted stop-loss and take-profit lines to manage your trades effectively. The combined labels provide all necessary information (SL, TP, nominal value, and cost value) for quick decision-making.

Execution and Risk Management:

Enter trades based on the reversal candle signals.

Set your stop-loss at the indicated level using the ATR calculation.

Take partial profits at the first take-profit level (1R) and adjust your stop-loss to the entry point to secure the remaining position.

Exit the trade entirely at the second take-profit level (2R) or if the price returns to the adjusted stop-loss level.

Harmonic Trading Tachometer [Pinescriptlabs]Key Features:

Visual Tachometer:

Represents market harmony through a speedometer on the chart.

The tachometer displays a range of harmony from "Highly Bearish" to "Highly Bullish."

Harmony Calculation:

Harmony Score: Based on ATR (Average True Range) range calculations for short, medium, and long periods. The harmony score is a weighted combination of these scores.

Interpretation: Harmony is translated into an interpretive category that can be "Highly Bearish," "Bearish," "Neutral," "Bullish," or "Highly Bullish."

Price Projection:

Estimates future price movement considering the current trend and the weight of each trend period (short, medium, and long).

Harmonic Change Detection:

Identifies significant changes in market harmony and adjusts sensitivity with predefined thresholds.

Confirmation and Divergence Signals:

Detects bullish or bearish confirmation signals as well as divergences, based on market harmony and price projection.

Additional Visualization:

Includes an optional market pentagram chart to visualize harmony on a broader scale.

Provides detailed information in a table about harmony, price projection, and harmonic changes.

How the Script Works:

Initial Calculations:

Ranges and Scores: Calculates ATR ranges for different periods (short, medium, and long). Then, evaluates the harmony score using the given formula.

Harmony: Obtained through the weighted combination of short, medium, and long-term scores.

Price Projection:

The projection is adjusted based on the difference between the current closing price and the exponential moving averages (EMAs) for different periods, weighted by the defined factors.

How to Use :

Tachometer Interpretation:

Observe the needle's position on the tachometer to assess the current market harmony.

Use the colors and labels to quickly interpret the market's state.

Projection and Changes:

Use the price projection to identify potential support or resistance levels.

Monitor harmonic changes and their strengths to adjust your trading strategies.

Confirmations and Divergences:

Pay attention to confirmation and divergence signals to decide on potential entries or exits.

Customization:

Adjust the indicator parameters, such as base length, harmony factor, change detection period, and trend weights, to fit your trading style and timeframe.

Español:

**Tacómetro Visual:

- Representa la armonía del mercado mediante un velocímetro en el gráfico.

- El tacómetro muestra un rango de armonía desde "Altamente Bajista" hasta "Altamente Alcista."

Cálculo de Armonía:

- Puntuación de Armonía:** Basada en los cálculos del rango ATR (Average True Range) para períodos cortos, medios y largos. La puntuación de armonía es una combinación ponderada de estas puntuaciones.

- Interpretación: La armonía se traduce en una categoría interpretativa que puede ser "Altamente Bajista," "Bajista," "Neutral," "Alcista," o "Altamente Alcista."

**Proyección de Precios:

- Estima el movimiento futuro de los precios considerando la tendencia actual y el peso de cada período de tendencia (corto, medio y largo).

**Detección de Cambios Armonicos:

- Identifica cambios significativos en la armonía del mercado y ajusta la sensibilidad con umbrales predefinidos.

**Señales de Confirmación y Divergencia:

- Detecta señales de confirmación alcista o bajista, así como divergencias, basadas en la armonía del mercado y la proyección de precios.

**Visualización Adicional:**

- Incluye un gráfico opcional de un pentagrama de mercado para visualizar la armonía en una escala más amplia.

- Proporciona información detallada en una tabla sobre la armonía, la proyección de precios y los cambios armónicos.

**Cómo Funciona el Script:**

Cálculos Iniciales:

- **Rangos y Puntuaciones:** Calcula los rangos del ATR para diferentes períodos (corto, medio y largo). Luego, evalúa la puntuación de armonía utilizando la fórmula dada.

- **Armonía:** Se obtiene a través de la combinación ponderada de las puntuaciones de corto, medio y largo plazo.

**Proyección de Precios:**

- La proyección se ajusta según la diferencia entre el precio de cierre actual y las medias móviles exponenciales (EMA) para diferentes períodos, ponderadas por los factores definidos.

**Cómo Usar:**

**Interpretación del Tacómetro:**

- Observa la posición de la aguja en el tacómetro para evaluar la armonía actual del mercado.

- Usa los colores y las etiquetas para interpretar rápidamente el estado del mercado.

**Proyección y Cambios:**

- Usa la proyección de precios para identificar posibles niveles de soporte o resistencia.

- Monitorea los cambios armónicos y sus fortalezas para ajustar tus estrategias de trading.

**Confirmaciones y Divergencias:**

- Presta atención a las señales de confirmación y divergencia para decidir posibles entradas o salidas.

**Personalización:**

- Ajusta los parámetros del indicador, como la longitud base, el factor de armonía, el período de detección de cambios y los pesos de tendencia, para adaptarlo a tu estilo de trading y marco de tiempo.

No Lag SupertrendNo Lag Supertrend indicator improves upon the original supertrend by incorporating calculation methods that enhance responsiveness and accuracy. Traditional supertrend indicators often suffer from lag, which can delay signals and affect trading decisions. No Lag Supertrend addresses this issue through the use of KAMA (Kaufman’s Adaptive Moving Average) and Hull ATR (Average True Range) calculations.

Goals of No Lag Supertrend:

- Lag reduction: one of the main issues with traditional supertrend indicators is their lag, which can result in delayed entry and exit signals. By integrating KAMA and Hull ATR, the no lag supertrend minimizes this delay, providing more timely signals.

- Market Noise Filtering: The combined use of KAMA and Hull ATR effectively filters out market noise, ensuring that signals are based on significant price movements rather than minor fluctuations.

- Consistency Across Different Market Conditions: The adaptive nature of KAMA and the smooth responsiveness of Hull ATR ensure that the No Lag Supertrend performs consistently across various market conditions, from trending to volatile markets.

Credits: This code is based on the TradingView supertrend but improved the ATR calculations.

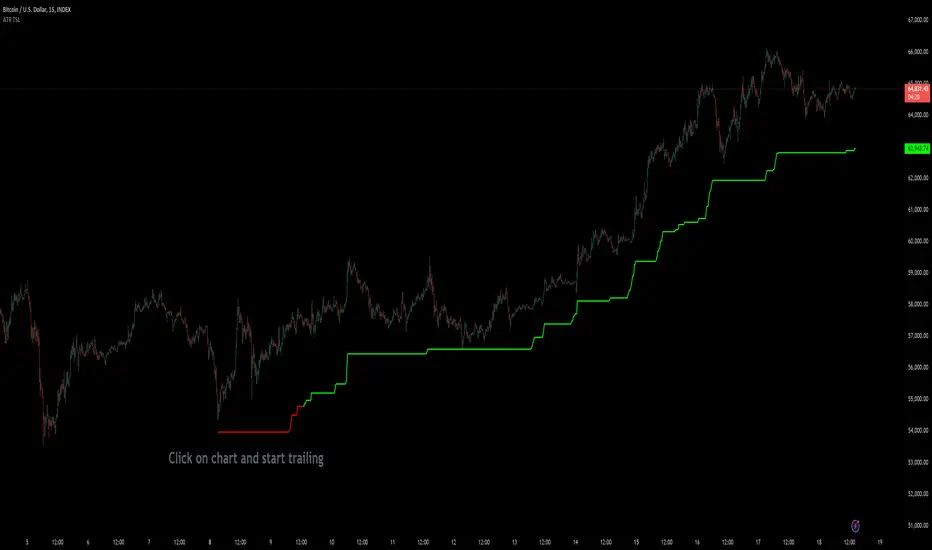

Custom ATR Trailing StopThis Script creates a custom ATR (Average True Range) trailing stop. It allows traders to set up automated stop-loss levels based on the ATR, which adjusts dynamically to market volatility. The script is designed to support both long and short trades, offering flexibility and precision in trade management.

When loading the indicator to your chart, simply click to set the trade begining time, confirm various settings and you are set.

Check tooltips for more details in the input settigns menu.

User Inputs

Trade Setup: Allows users to set the trade direction (Long or Short), the signal source for entries, and the specific bar time for the trade setup.

ATR Settings: Configurable ATR lookback period, ATR smoothing period, initial ATR multiplier for setting the stop-loss, breakeven ATR multiplier, and a manual breakeven level.

ATR Calculations

Computes the ATR and its moving average.

Determines initial and breakeven stop levels based on the ATR.

Signal Validation

Validates long or short trade signals based on the specified bar time and trade direction.

Triggers alerts when a valid trade signal is detected.

Trailing Stop Logic

For long trades, adjusts the stop-loss level dynamically based on the ATR.

For short trades, performs similar adjustments in the opposite direction.

Updates the trailing stop level to ensure it follows the price, moving closer as the price moves favorably.

Resets the trade state when the stop-loss is hit, triggering an alert.

Plotting

Plots the trailing stop levels on the chart.

Uses green for stop levels indicating profit and red for stop levels indicating a loss.

Consistent ATR Trailing Stop (ATR, 1m based) [nn1]This indicator implements a Consistent ATR (Average True Range) Trailing Stop that maintains uniform behavior across various chart timeframes. It's designed to provide traders with a reliable tool for setting dynamic stop-loss levels that adapt to market volatility while remaining consistent regardless of the chosen chart interval.

Key Features:

1. Consistent ATR Calculation: The indicator calculates the ATR based on 1-minute data, regardless of the current chart timeframe. This ensures that the ATR value remains consistent across different intervals (e.g., 10s, 15s, 30s, 60s), providing a stable base for the trailing stop.

2. Dynamic Trailing Stop: The trailing stop adjusts based on the ATR, moving up in uptrends and down in downtrends to protect profits while allowing room for price fluctuations.

3. Trend Detection: The indicator determines the trend based on the price's relationship to the trailing stop, switching between long and short modes as the trend changes.

4. Visual Cues: The trailing stop line changes color to indicate the current trend (green for uptrends, red for downtrends) and briefly turns yellow during trend changes. Small circles below or above the price action further highlight the current trend direction.

5. Information Display: A label shows the current ATR value and trend direction, providing at-a-glance information to the trader.

6. Trend Change Highlights: The background briefly changes color when a trend change occurs, drawing attention to potential trading opportunities or exit points.

Usage:

- ATR Length: Set the number of periods for the ATR calculation. This is based on 1-minute data, so a value of 14 represents 14 minutes of data.

- ATR Multiplier: Adjust how far the trailing stop is placed from the price. Higher values create a wider stop, allowing for more price movement before triggering.

This indicator is particularly useful for traders who:

- Use multiple timeframes in their analysis and want consistent signals across charts.

- Seek a dynamic stop-loss method that adapts to market volatility.

- Want clear visual cues for trend direction and changes.

By providing a consistent ATR-based trailing stop across different timeframes, this indicator helps traders maintain a unified approach to their trading strategy, regardless of the chart interval they are viewing.

Fair Value Gap (FVG) Oscillator [UAlgo]The "Fair Value Gap (FVG) Oscillator " is designed to identify and visualize Fair Value Gaps (FVG) within a given lookback period on a trading chart. This indicator helps traders by highlighting areas where price gaps may signify potential trading opportunities, specifically bullish and bearish patterns. By leveraging volume and Average True Range (ATR) data, the FVG Oscillator aims to enhance the accuracy of pattern recognition and provide more reliable signals for trading decisions.

🔶 Identification of Fair Value Gap (FVG)

Fair Value Gaps (FVG) are specific price areas where gaps occur, and they are often considered significant in technical analysis. These gaps can indicate potential future price movements as the market may return to fill these gaps. This indicator identifies two types of FVGs:

Bullish FVG: Occurs when the current low price is higher than the high price two periods ago. This condition suggests a potential upward price movement.

Obtains with:

low > high

Bearish FVG: Occurs when the current high price is lower than the low price two periods ago. This condition suggests a potential downward price movement.

Obtains with:

high < low

The FVG Oscillator not only identifies these gaps but also verifies them using volume and ATR conditions to ensure more reliable trading signals.

🔶 Key Features

Lookback Period: Users can set the lookback period to determine how far back the indicator should search for FVG patterns.

ATR Multiplier: The ATR Multiplier is used to adjust the sensitivity of the ATR-based conditions for verifying FVG patterns.

Volume SMA Period: This setting determines the period for the Simple Moving Average (SMA) of the volume, which helps in identifying high volume conditions.

Why ATR and Volume are Used?

ATR (Average True Range) and volume are integrated into the Fair Value Gap (FVG) Oscillator to enhance the accuracy and reliability of the identified patterns. ATR measures market volatility, helping to filter out insignificant price gaps and focus on impactful ones, ensuring that the signals are relevant and strong. Volume, on the other hand, confirms the strength of price movements. High volume often indicates the sustainability of these movements, reducing the likelihood of false signals. Together, ATR and volume ensure that the detected FVGs are both significant and supported by market activity, providing more trustworthy trading signals.

Normalized Values: The FVG counts are normalized to enhance the visual representation and interpretation of the patterns on the chart.

Visual Customization and Plotting: Users can customize the colors for positive (bullish) and negative (bearish) areas, and choose whether to display these areas on the chart, also plots the bullish and bearish FVG counts, a zero line, and the net value of FVG counts. Additionally, it uses histograms to display the width of verified bullish and bearish patterns.

🔶 Disclaimer:

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Candle Range Detector [UAlgo]The "Candle Range Detector " is a Pine Script™ indicator designed to identify trading opportunities based on the concept of price consolidation and breakout. It analyzes the price range of a specified number of previous candles and detects when subsequent candles stay within that range (consolidation). The indicator then highlights potential breakouts above or below the range and provides calculated Take Profit (TP) and Stop Loss (SL) levels based on your chosen method (percentage or Average True Range - ATR).

🔶 Key Features

Configurable Range: Define the minimum number of candles required to establish a valid price range.

Breakout Detection: Identify potential breakouts above or below the established range based on your selection (close price or wick).

Take Profit & Stop Loss Levels: The indicator calculates TP and SL levels based on your chosen method (percentage or ATR) and user-defined multipliers. The calculated TP and SL levels are visualized as horizontal lines with corresponding labels ("Take Profit" and "Stop Loss").

Optional Count Display: You can choose to display the number of candles currently within the range.

🔶 Disclaimer:

Not Financial Advice: This indicator is intended for educational and informational purposes only. It does not constitute financial advice or recommendations to buy, sell, or hold any financial instruments.

Use at Own Risk: Trading involves substantial risk of loss and is not suitable for all investors. Users of this indicator should exercise caution and conduct their own research and analysis before making any trading decisions.

Performance Not Guaranteed: Past performance is not indicative of future results. While the indicator aims to assist traders in analyzing market trends, there is no guarantee of accuracy or success in trading operations.

🔷 Related Scripts

Range Finder

ATR Gerchik LightAverage True Range ( ATR ) is a technical analysis indicator that measures volatility in the market. ATR is a moving average of the true range over a period of time.

ATR calculation procedure:

1. Determine the true maximum - this is the highest of the current maximum and yesterday's closing price of the day.

2. Determine the true minimum - this is the smallest of the current minimum and yesterday's closing price.

3. Determine the true range - this is the distance between the true maximum and minimum.

4. We exclude extremely large candles (> x2 ATR) and extremely small ones (< 0.5 ATR) from the obtained true ranges.

5. We calculate the average for the selected period based on the remaining range.

6. We calculate the percentage of the current True Range relative to the average ATR value for the previous period.

Description:

If you analyze it yourself, you will see that 75-80% of the time, the instrument moves only 1 ATR per day. You must understand that if an instrument has, for example, moved 80% of its daily range, it is not advisable to purchase it. This is comparable to a car's fuel tank: if the tank is almost empty, the car won't go far. Most indicators that calculate ATR include anomalous candles, which give unreliable results and lead to incorrect decisions. Because of this, many traders prefer to calculate ATR on their own.

However, the Gerchik ATR indicator accounts for anomalous candles and filters out extremely large candles (> 2x ATR) and extremely small ones (< 0.5x ATR). Additionally, this indicator immediately shows the consumed “fuel” of the instrument as a percentage, so you don't have to calculate the distance traveled yourself. This allows you to make quick, informed decisions. If we see that the tank is almost empty, it is logical not to get into that car today. When building any strategy, you must rely on the average movement.

Key Features:

Anomalous Candle Filtering: Excludes extremely large and small candles to provide more reliable ATR values.

Consumed Fuel Indicator: Shows the percentage of the ATR consumed, helping traders quickly assess the remaining potential movement.

Daily Timeframe Focus: Designed specifically for use on daily charts for accurate long-term analysis.

Practical Applications:

Entry and Exit Points: Use the ATR to determine optimal entry and exit points by assessing market volatility and potential price movement.

Stop-Loss Placement: Calculate stop-loss levels based on ATR to ensure they are placed at appropriate distances, accounting for current market volatility.

Trend Confirmation: Use the percentage of ATR consumed to confirm the strength of a trend and decide whether to enter or exit trades.

Examples of Use:

Trend Following: During strong trends, ATR helps identify periods of increased volatility, signaling potential breakouts or reversals.

Range Trading: In ranging markets, ATR can highlight periods of low volatility, indicating consolidation and potential breakout zones.

Note: The indicator is displayed and works only on the daily timeframe!

The indicator was created according to the instructions, description of the functionality, and strategy of Mr. Gerchik. Thank you so much, Chief!

________________________

Average True Range ( ATR , средний истинный диапазон) – это индикатор технического анализа, который измеряет волатильность на рынке. ATR представляет собой скользящее среднее истинного диапазона за определенный период времени.

Порядок расчета ATR:

1. Определяем истинный максимум – это наивысшее из текущего максимума и вчерашней цены закрытия дня.

2. Определяем истинный минимум – это наименьшее из текущего минимума и вчерашней цены закрытия.

3. Определяем истинный диапазон – это расстояние между истинным максимумом и минимумом.

4. Исключаем из полученных истинных диапазонов экстремально большие свечи (> x2 ATR) и экстремально маленькие (< 0.5 ATR).

5. Рассчитываем среднее за выбранный период исходя из оставшегося диапазона.

6 . Рассчитываем процент текущего истинного диапазона (True Range) относительно среднего значения ATR за предыдущий период.

Описание:

Если вы сами проанализируете, то увидите, что 75-80% времени инструмент ходит только 1 ATR. И вы должны понимать, что если инструмент внутри дня прошел, к примеру, 80% своего движения, то этот инструмент больше нельзя покупать. Это можно сравнить с баком машины: если бак почти пустой, машина далеко не уедет. Большинство индикаторов, которые рассчитывают ATR, производят расчет с паранормальными свечами. Это дает недостоверный результат и приводит к неверным решениям. Многие трейдеры из-за этого не используют готовые индикаторы и предпочитают считать ATR самостоятельно. Но индикатор ATR Gerchik учитывает паранормальные свечи и фильтрует экстремально большие свечи (> x2 ATR) и экстремально маленькие (< 0.5 ATR). Также этот индикатор сразу показывает израсходованный "бензин" инструмента в процентах. И вам не надо самостоятельно высчитывать пройденный путь. Вы можете быстро принимать правильные решения. Если мы видим, что бак почти пустой, логично не садиться в эту машину сегодня. Когда вы строите какую-то стратегию, вы должны обязательно полагаться на среднестатистическое движение.

Существует много стратегий, завязанных на ATR, которые учитывают волатильность инструмента, запас хода, точки разворота, места выставления стоп-лоссов (SL) и тейк-профитов (TP) и другие факторы. Я не буду останавливаться на них, так как каждый может найти описание этих стратегий и использовать их на свой выбор.

Индикатор отображается и работает только на дневном таймфрейме!

Индикатор создан по наставлениям, описанию функционала и стратегии господина Герчика. Огромное спасибо, Шеф!

ICT Single Candle Order Block (SCOB) [UAlgo]The "ICT Single Candle Order Block (SCOB) " designed for traders who utilize the concept of Order Blocks in their trading strategy. Order Blocks are significant price levels where institutions or smart money have placed their trades, leading to potential future price reactions when these levels are revisited. This indicator focuses on identifying and highlighting Single Candle Order Blocks (SCOBs), allowing traders to visually analyze key price levels on their charts.

🔶 What is Single Candle Order Block (SCOB) ?

A Single Candle Order Block (SCOB) is a specific type of Order Block that is identified based on a single candlestick pattern. These patterns indicate potential areas where significant buying or selling interest has occurred, often leading to a notable price reaction when revisited. In the context of this indicator, a bullish SCOB is identified when a specific bullish candlestick pattern is met, and a bearish SCOB is identified based on a bearish candlestick pattern.

Bullish SCOB: Detected when the open price of two bars ago is higher than its close, the close price of the previous bar is higher than its open, the current close price is higher than the open, the low of the previous bar is lower than the low of two bars ago, and the current close is higher than the high of the previous bar.

Bearish SCOB: Detected when the open price of two bars ago is lower than its close, the close price of the previous bar is lower than its open, the current close price is lower than the open, the high of the previous bar is higher than the high of two bars ago, and the current close is lower than the low of the previous bar.

🔶 Key Features

Show Single Candle Order Block (SCOB): Toggle the visibility of the Single Candle Order Blocks on the chart.

Mitigation Method: Choose between "Close" and "Wick" methods for determining whether a SCOB has been mitigated (price has interacted with the block).

Show Last X SCOBs: Control the number of most recent SCOBs displayed on the chart, allowing you to focus on the most relevant price levels.

Volatility Filter: Enable or disable the volatility filter, which uses the Average True Range (ATR) to filter out less significant SCOBs. When enabled, only SCOBs with an ATR above the mean value of the ATR are displayed.

Customizable Colors: Configure the colors for bullish and bearish SCOBs to enhance visual clarity. The indicator uses cooler RGB values to ensure the blocks are distinct and easily noticeable.

🔶 Disclaimer

The "ICT Single Candle Order Block (SCOB) " indicator is provided for educational and informational purposes only. Trading involves significant risk and may not be suitable for all investors.

Past performance is not indicative of future results. Users should use this indicator in conjunction with their own research and trading strategy.

Supports & Resistances [UAlgo]The "Supports & Resistances " indicator is designed to identify and visualize key support and resistance levels on the price chart. It utilizes the Average True Range (ATR) and Pivot Points to define the boundaries of S & R zones and considers historical price action to assess the strength of these zones.

🔶 How to Obtain Zones

The script continuously analyzes the price action and identifies potential support and resistance zones based on the following criteria:

Zone Creation: For swing highs, a zone is created with the high price at the zone length as the top and the top minus the Average True Range (ATR) as the bottom. Conversely, for swing lows, the zone is created with the low price at the zone length as the bottom and the low plus the ATR as the top.

Zone Strength Calculation: The script iterates through historical bars within the zone and counts how many times the price (low for support, high for resistance) touched but failed to break entirely through the zone. This count is assigned as the zone's "strength".

Zone Display and Removal: It identifying zones by assigning a "strength" value based on how many times the price has approached but failed to break the zone. This helps prioritize stronger potential support/resistance levels. Only zones exceeding the defined "strength threshold" are visually displayed on the chart. Weaker zones or those broken by price are automatically removed.

🔶 Parameters

Zone Length: Traders can adjust S & R detection sensitivity, length to be used to find pivot points.

Strength Threshold: Set the minimum number of times the price needs to touch but fail to break a zone for it to be considered "strong" and displayed.

Visual Settings: Tailor the appearance of the support/resistance zones by defining separate colors and text size for borders, backgrounds, and zone text.

🔶 Disclaimer

The "Supports & Resistances " indicator is provided for educational and informational purposes only.

It should not be considered as financial advice or a recommendation to buy or sell any financial instrument.

The use of this indicator involves inherent risks, and users should employ their own judgment and conduct their own research before making any trading decisions. Past performance is not indicative of future results.

🔷 Related Scripts

Support and Resistance with Signals

ATR Based Support and Resistance Zones

Scalping System by Machine# Custom Trading System Indicator

This Pine Script indicator is designed to identify potential trading setups based on a specific set of rules. It's intended for use on lower timeframes (M1-M5) in the forex market, particularly during the New York-London overlap period.

## Key Features

1. **EMA Condition**: Uses a 20-period Exponential Moving Average (EMA) to determine trend direction.

2. **Candle Analysis**: Identifies strong bars and candle color changes.

3. **Volume Confirmation**: Checks for increasing volume.

4. **Volatility Filter**: Utilizes the Average True Range (ATR) to gauge market volatility.

5. **Time-based Filter**: Highlights the New York-London overlap period.

6. **Visual Aids**: Plots potential entry points, stop losses, and take profit levels.

## Trading Rules

1. **Buy Signal**:

- Price is above the 20 EMA

- Candle color changes from red to green

- Current candle is a strong bar (closing within 75% of its range)

- Volume is higher than the previous bar

- ATR(14) is above 4 pips OR it's during the NY-London overlap

2. **Sell Signal**:

- Price is below the 20 EMA

- Candle color changes from green to red

- Current candle is a strong bar (closing within 75% of its range)

- Volume is higher than the previous bar

- ATR(14) is above 4 pips OR it's during the NY-London overlap

3. **Stop Loss**: Placed near the low of the setup candle for buys, or near the high for sells.

4. **Take Profit**: Aimed at 1R (one times the range of the setup candle).

## Visual Elements

- **20 EMA**: Plotted as a blue line on the chart.

- **Buy Signals**: Green triangles below the candles.

- **Sell Signals**: Red triangles above the candles.

- **Stop Loss Levels**: Small red dots at the calculated stop loss prices.

- **Take Profit Levels**: Small green dots at the calculated take profit prices.

- **Information Table**: Displays current values for ATR, strong bar condition and volume condition.

## Usage Notes

1. This indicator is designed for manual trading, not automated execution.

2. It works best when combined with analysis of major trend lines, support, and resistance levels.

3. Exercise caution with very large setup candles.

4. Consider additional filters or money management rules for enhanced performance.

5. For higher timeframe bias validation, consider incorporating a 100-period break of structure (BOS) analysis.

## Customization

The indicator includes several input parameters that can be adjusted:

- EMA Length

- ATR Length and Threshold

- Volume Multiplier

- Strong Bar Percentage

Users can also toggle the visibility of stop loss and take profit markers.

Remember, while this indicator can identify potential setups, it should be used in conjunction with other forms of analysis and risk management strategies. Always consider the overall market context and your personal risk tolerance when making trading decisions.

ATR (Average True Range) mit relative/absolute Zahlen GERMAN:

Schnelle Zusammenfassung:

Dieses Skript basiert auf dem ATR-Indikator und wurde so angepasst, dass sowohl relative (%) als auch absolute Zahlen angezeigt werden. Es bietet eine Darstellung des ATR in absoluten und prozentualen Werten sowie multipliziert mit den Faktoren x2, x2.5 und x3. Diese Darstellung erleichtert die Festlegung von Stop-Kursen, insbesondere für Trailing Stops und Trailing Abstände.

Periode:

Die Periode ist einstellbar und definiert die Länge der Berechnung des ATR (Standardwert: 14).

Glättung: Es stehen verschiedene Methoden zur Auswahl, um die Daten zu glätten (RMA, SMA, EMA, WMA).

Berechnungen:

ATR (Absolute Zahl): Berechnung der durchschnittlichen wahren Reichweite (ATR) unter Verwendung der ausgewählten Glättungsmethode und Periode.

ATR (Prozentualer Wert): Berechnung des ATR als Prozentsatz des aktuellen Schlusskurses.

Multiplikation des ATR: Berechnung des ATR multipliziert mit den Faktoren 2, 2.5 und 3 zur Einschätzung verschiedener Handelsszenarien.

Darstellung:

Absoluter ATR-Wert: Darstellung der absoluten ATR-Werte in Blau.

Relative ATR-Werte (%): Darstellung der prozentualen ATR-Werte, ohne Linie in der Grafik (transparent).

Multiplizierte ATR-Werte (x2, x2.5, x3): Darstellung der multiplizierten ATR-Werte in den Farben Grün (x2), Orange (x2.5) und Lila (x3).

Textbeschriftungen: Für jeden absoluten ATR-Wert und seine Multiplikationen werden Textbeschriftungen links im Chart angezeigt.

Verwendung des Indikators:

Dieser Indikator unterstützt Trader und Analysten dabei, die durchschnittliche wahre Reichweite (ATR) eines Finanzinstruments zu verstehen und zu visualisieren. Die verschiedenen Multiplikationen des ATR ermöglichen es, potenzielle Preisbewegungen zu analysieren und Handelsstrategien zu entwickeln, die auf der Volatilität basieren.

Hinweis:

Dies ist meine persönliche Meinung und Einstellung. Dieses Skript stellt keine Bankberatung oder Anlageempfehlung dar. Die Nutzung erfolgt auf eigenes Risiko und Verantwortung des Nutzers.

----------------------------------------------------------------------

ENGLISH:

Quick Summary:

This script is based on the ATR (Average True Range) indicator and has been modified to display both relative (%) and absolute values. It provides a representation of ATR in absolute and percentage terms, as well as multiplied by factors x2, x2.5, and x3. This visualization aids in setting stop-loss levels, especially for trailing stops and trailing distances.

Period:

The period is adjustable and defines the length of the ATR calculation (default: 14).

Smoothing: Various methods are available to smooth the data (RMA, SMA, EMA, WMA).

Calculations:

ATR (Absolute Value): Computes the Average True Range using the selected smoothing method and period.

ATR (Percentage Value): Calculates the ATR as a percentage of the current closing price.

Multiplication of ATR: Computes the ATR multiplied by factors 2, 2.5, and 3 to assess different trading scenarios.

Visualization:

Absolute ATR Value: Displays the absolute ATR values in blue.

Relative ATR Values (%): Shows the ATR values as percentages, without lines in the chart (transparent).

Multiplied ATR Values (x2, x2.5, x3): Presents the multiplied ATR values in green (x2), orange (x2.5), and purple (x3).

Text Labels: Text labels are shown on the left side of the chart for each absolute ATR value and its multiples.

Use of the Indicator:

This indicator helps traders and analysts understand and visualize the Average True Range (ATR) of a financial instrument. The different multipliers of ATR allow for the analysis of potential price movements and the development of trading strategies based on volatility.

Disclaimer:

This represents my personal opinion and viewpoint. This script does not constitute bank advice or investment recommendations. Use it at your own risk and responsibility.

[KVA] KATRThe KATR indicator enhances the traditional ATR by leveraging the most common candle body percentage range, tailoring volatility measurement to specific market contexts. This advanced tool provides more relevant insights tailored to current market conditions.

Key Features:

Configurable ATR Length : Allows users to set the period for the ATR calculation, providing flexibility to adapt to different trading strategies and timeframes.

Multiple Smoothing Options : Offers a choice of RMA, SMA, EMA, and WMA for smoothing the ATR, enabling traders to select the method that best suits their analysis style.

Histogram Visualization for ATR Differences: The histogram visually represents the difference between the ATR and its moving average. This difference, or "dif," is calculated and smoothed, then multiplied by a user-defined factor. The histogram color indicates market conditions:

Light Red: Increasing but below zero, signaling potential weakening.

Light Green: Increasing and above zero, indicating strengthening.

Dark Green: Decreasing but above zero, showing potential weakening.

Dark Red: Decreasing and below zero, indicating strong weakening.

Ideal for Traders:

This indicator is perfect for traders seeking precise, context-sensitive volatility assessments to optimize trade timing and risk management strategies. Integrated seamlessly with other technical indicators, the KATR enhances your trading dashboard by adding depth to volatility analysis.

Detailed Explanation:

ATR Calculation: The ATR is derived by taking the average true range over a specified period, multiplied by the most common body percentage found in historical data.

Smoothing: Users can smooth the ATR using different methods, adding flexibility and customization to suit various trading styles.

Histogram: The histogram's primary function is to visualize the difference between the current ATR and its smoothed average. This provides clear, visual signals for potential volatility expansions or contractions, aiding in better decision-making.

Whether you're a day trader or a long-term investor, the KATR helps you stay ahead of market trends with reliable and easy-to-interpret insights. Elevate your trading strategy with the KATR's innovative approach to volatility measurement.

ATR by Time [QuantVue]"ATR by Time" incorporates time-specific volatility patterns by calculating the Average True Range (ATR) over a customizable period and comparing it to historical ATR values

at specific times of the day.

The Average True Range (ATR) is a popular technical indicator that measures market volatility by decomposing the entire range of an asset price for that period.

By taking the ATR at certain times of the day and comparing it to the current bar's ATR, traders can gain several potential advantages:

Volatility Pattern Recognition: Different times of the trading day often exhibit different levels of volatility. For instance, markets might be more volatile at the open and close compared to midday. By tracking ATR at specific times, traders can recognize these patterns and better predict periods of high or low volatility.

Risk Management: Understanding volatility trends throughout the day helps in better risk management. During periods of high expected volatility (indicated by higher ATR compared to the historical average), traders can adjust their stop-loss levels and position sizes accordingly to protect their capital.

Trend Confirmation and Divergence: This indicator can help confirm trends or identify potential reversals. For example, if the current ATR consistently exceeds the average ATR at specific times, it may confirm a strong trend. Conversely, if the current ATR falls below the historical average, it could signal a potential slowdown or reversal.

This indicator will work on all markets on all time frames. User can customize ATR length as well as the lookback period.

This script utilizes TradingView's RelativeValue library and averageAtTime function, which is used to compare a current data point in a time interval to an average of data points with corresponding time offsets across historical periods. Its purpose is to assess the significance of a value by considering the historical context within past time intervals.

Give this indicator a BOOST and COMMENT your thoughts!

We hope you enjoy.

Cheers!

Supertrend Alert with Arrows and Time FilterOverview

This script is designed to generate trading signals based on the Supertrend indicator, a popular technical analysis tool. The Supertrend indicator is used to identify the direction of the market trend and potential reversal points.

Supertrend Settings

The script uses two sets of Supertrend settings:

Small Supertrend

Factor: 3.0

ATR Period: 10

Big Supertrend

Factor: 10.0

ATR Period: 30

These settings are fixed and should not be altered to maintain the integrity of the signal generation process.

Configurable Parameters

startHour: The hour at which signal generation begins.

endHour: The hour at which signal generation ends.

These parameters allow users to focus on specific trading hours, optimizing the signal relevance to their trading strategy.

Signal Types

The script generates two types of signals:

Type 1: Reversal Signal

Long Signal: Triggered when the big Supertrend is in an uptrend, and the small Supertrend transitions from a downtrend to an uptrend.

Short Signal: Triggered when the big Supertrend is in a downtrend, and the small Supertrend transitions from an uptrend to a downtrend.

Type 2: Trend Change Signal

Long Signal: Triggered when the big Supertrend changes from a downtrend to an uptrend.

Short Signal: Triggered when the big Supertrend changes from an uptrend to a downtrend.

How the Script Works

Initialization: The script initializes with predefined Supertrend settings.

Data Input: Market data (e.g., price data) is fed into the script.

Supertrend Calculation: The script calculates the Supertrend values using the predefined factors and ATR periods.

Signal Detection: The script monitors the Supertrend values and detects the defined signals based on the conditions mentioned above.

Time Filtering: Signals are filtered based on the specified startHour and endHour, ensuring only relevant signals are displayed within the desired timeframe.

Usage

Set Parameters: Define startHour and endHour according to your trading schedule.

Run Script: Execute the script with market data input.

Interpret Signals: Monitor the generated signals and use them to inform your trading decisions.

Originality

Dual Supertrend Usage: The use of both a small and a big Supertrend to generate signals adds a layer of complexity and reliability to the signals.

Time-Based Filtering: Allows traders to focus on specific trading hours, enhancing the relevance and accuracy of signals.

Two Signal Types: The combination of reversal signals and trend change signals provides comprehensive market insights.

Conclusion

This Supertrend Signal Generator is a robust tool for traders seeking to leverage the Supertrend indicator for more informed trading decisions. By combining dual Supertrend settings and configurable trading hours, the script offers unique and flexible signal generation capabilities.

ATR Price Range Prediction V.2### ATR Price Range Prediction V.2

This script calculates the expected high and low prices for the current day based on the Average True Range (ATR) and displays the proportion of days where the daily range (high - low) is greater than or equal to the ATR. Additionally, the script provides an option to adjust the size of the text displayed in the top-right corner of the chart.

#### How It Works

1. **ATR Calculation**: The script calculates the ATR for a specified period (`atrPeriod`). ATR is a measure of volatility that represents the average range between the high and low prices over a specified number of periods.

2. **Expected High and Low Calculation**:

- **Expected High**: Calculated by adding the ATR value to the low price of the current day.

- **Expected Low**: Calculated by subtracting the ATR value from the high price of the current day.

3. **Proportion Calculation**: The script calculates the proportion of days where the daily range (high - low) is greater than or equal to the ATR value. This proportion is updated in real-time as new data comes in.

4. **Table Display**: Instead of displaying labels on each candle, the script shows the expected high, expected low, and the calculated proportion in a table located at the top-right corner of the chart. The size of the text in this table can be adjusted using the `Table Size` input.

5. **Color Coding**: The script changes the color of the bars to yellow if the daily range is greater than or equal to the ATR value, making it easy to identify these bars visually.

#### How to Use

- **ATR Period (`atrPeriod`)**: Adjust the period for the ATR calculation using the input parameter. The default value is 14.

- **Table Size (`tableSizeOption`)**: Choose the size of the text displayed in the table. Options include `tiny`, `small`, `normal`, `large`, and `huge`.

- **Expected High and Low**: Use the green and red lines to identify potential target prices or stop-loss levels for your trades. The green line represents the expected high, and the red line represents the expected low.

- **Proportion**: The table in the top-right corner of the chart shows the proportion of days where the daily range is greater than or equal to the ATR value. This can provide insight into the volatility of the asset.

- **Color Coding**: Yellow bars indicate days where the daily range is greater than or equal to the ATR value.

---

### ภาษาไทย

### ATR คาดการณ์ราคาสูงสุดและต่ำสุด พร้อมสัดส่วน

สคริปต์นี้คำนวณราคาสูงสุดและต่ำสุดที่คาดการณ์สำหรับวันปัจจุบันโดยอิงจากค่าเฉลี่ยช่วงที่แท้จริง (ATR) และแสดงสัดส่วนของวันที่ช่วงราคาต่อวัน (สูง - ต่ำ) มากกว่าหรือเท่ากับค่า ATR นอกจากนี้ยังมีตัวเลือกในการปรับขนาดข้อความที่แสดงในกล่องข้อความมุมขวาบนของกราฟ

#### วิธีการทำงาน

1. **การคำนวณ ATR**: สคริปต์คำนวณค่า ATR สำหรับช่วงเวลาที่กำหนด (`atrPeriod`) ATR เป็นมาตรวัดความผันผวนที่แสดงช่วงเฉลี่ยระหว่างราคาสูงสุดและต่ำสุดในช่วงเวลาที่กำหนด

2. **การคำนวณราคาสูงสุดและต่ำสุดที่คาดการณ์**:

- **ราคาสูงสุดที่คาดการณ์**: คำนวณโดยการบวกค่า ATR กับราคาต่ำสุดของวันปัจจุบัน

- **ราคาต่ำสุดที่คาดการณ์**: คำนวณโดยการลบค่า ATR จากราคาสูงสุดของวันปัจจุบัน

3. **การคำนวณสัดส่วน**: สคริปต์คำนวณสัดส่วนของวันที่ช่วงราคาต่อวัน (สูง - ต่ำ) มากกว่าหรือเท่ากับค่า ATR สัดส่วนนี้จะอัปเดตแบบเรียลไทม์เมื่อมีข้อมูลใหม่เข้ามา

4. **การแสดงผลในตาราง**: แทนที่จะแสดงป้ายกำกับบนแท่งเทียนแต่ละแท่ง สคริปต์จะแสดงราคาสูงสุดที่คาดการณ์ ราคาต่ำสุดที่คาดการณ์ และสัดส่วนที่คำนวณในตารางที่มุมขวาบนของกราฟ โดยสามารถปรับขนาดข้อความในตารางได้

5. **การใช้สี**: สคริปต์จะเปลี่ยนสีของแท่งเทียนเป็นสีเหลืองหากช่วงราคาต่อวันมากกว่าหรือเท่ากับค่า ATR ทำให้สามารถระบุแท่งเทียนเหล่านี้ได้ง่ายขึ้น

#### วิธีการใช้งาน

- **ATR Period (`atrPeriod`)**: ปรับช่วงเวลาสำหรับการคำนวณ ATR โดยใช้พารามิเตอร์การป้อนค่า ค่าเริ่มต้นคือ 14

- **Table Size (`tableSizeOption`)**: เลือกขนาดข้อความที่แสดงในตาราง ตัวเลือกได้แก่ `tiny`, `small`, `normal`, `large`, และ `huge`

- **ราคาสูงสุดและต่ำสุดที่คาดการณ์**: ใช้เส้นสีเขียวและสีแดงเพื่อระบุราคาที่เป็นเป้าหมายหรือระดับการหยุดขาดทุนสำหรับการซื้อขายของคุณ เส้นสีเขียวแสดงถึงราคาสูงสุดที่คาดการณ์และเส้นสีแดงแสดงถึงราคาต่ำสุดที่คาดการณ์

- **สัดส่วน**: ตารางที่มุมขวาบนของกราฟแสดงสัดส่วนของวันที่ช่วงราคาต่อวันมากกว่าหรือเท่ากับค่า ATR ซึ่งสามารถให้ข้อมูลเชิงลึกเกี่ยวกับความผันผวนของสินทรัพย์

- **การใช้สี**: แท่งเทียนสีเหลืองบ่งบอกถึงวันที่ช่วงราคาต่อวันมากกว่าหรือเท่ากับค่า ATR

_____

Volume True Range (VTR) and Volume Average True Range (VATR)This indicator uses lower-timeframe cumulative volume delta (CVD) candles to calculate the Volume True Range (VTR) of your instrument. The VTR is calculated similarly to the traditional true range, but uses volume instead (no price is involved in the calculation other than in the lower timeframe bar delta assignments). I haven't seen this concept developed before on TradingView or frankly the Internet, but I thought it seemed fairly intuitive; we can calculate the lower timeframe volume delta candles, so it makes sense to calculate a volume true range, which could show divergences in volume and price.

The VTR is calculated by the following code which uses the lower-timeframe CVD candles:

volumeTR = math.max(cvd_high - cvd_low, math.abs(cvd_high - nz(cvd_close )), math.abs(cvd_low - nz(cvd_close )))

The Volume Average True Range (VATR) is calculated by taking the RMA of the VTR, similarly to the ATR.

I would like to thank TradingView for the calculation of up/down intrabar volumes, which I referenced from their 'CVD - Cumulative Volume Delta Candles' indicator.

How to Use

The VTR and VATR can be used to identify price-volume trends and volatility divergences. A strong VTR (above the VATR of your specified length) can indicate the start or continuation of a trend, which you can identify via the VTR color (determined via price candle colors). Similarly, a rising VATR with most VTR bars of a specific color (green or red) will show that volume is moving in a specific price direction.

Additionally, the VATR plotted next to the ATR of the same length will show you volume volatility divergences. A strong VATR next to a muted/flat ATR indicates strong volume movement, which price might follow in the upcoming bars. Or, for trend reversals, a decreasing ATR after a strong trend combined with a rising VATR of the opposite trend may show a possible reversal.

Hope you all enjoy this.

-wbburgin

* Quick note: lower timeframe analysis returns only so much data. If you are on a high timeframe and the indicator is showing only a limited amount of bars, raise the lower timeframe (but still keep it below your current timeframe) so that the arrays can return more bars for you.

Trade Exit Calculator [MarketSignalsPro]█ OVERVIEW

This Pine Script calculates a Stop Loss and Take Profit order suggestion based on the Average True Range (ATR). This provides a market generated visual reference for the user to better gauge risk and profit potential for their trades. This is not a trade signal system, it is a tool best used in conjunction with an existing system.

█ FEATURES

Inputs:

stopLossMultiplier and takeProfitMultiplier : These are input parameters that allow the user to adjust the multiplier for calculating stop loss and take profit levels.

longIndicator : This input parameter determines whether the script is calculating levels for a long setup (buy) or a short setup (sell).

Variable Initialization:

Various variables are initialized to manage labels, lines, and calculated stop loss and take profit levels.

ATR (Average True Range) is calculated using a period of 14.

Calculation of Stop Loss and Take Profit:

Depending on the value of longIndicator stop loss and take profit levels are not calculated the same way.

For long setups, stop loss is calculated below the closing price and take profit above, while for short setups, it's the opposite.

The calculation involves multiplying the ATR value by the user-defined multipliers and adding or subtracting from the closing price accordingly.

Plotting Lines:

Lines representing the calculated stop loss, take profit, and entry price are plotted on the chart.

Displaying Labels:

Labels displaying the calculated stop loss, take profit, and entry price are shown on the chart alongside the respective lines.

Updating and Deleting Objects:

Existing lines and labels are updated or deleted to ensure only the most recent levels are displayed on the chart.

Final Output:

The script outputs visual representations of stop loss, take profit, and entry price levels on the chart, providing traders with guidance for risk management and profit-taking strategies based on the volatility of the market.

█ CONCLUSION

In summary, this Pine Script enhances trading strategies by calculating and illustrating stop loss and take profit levels based on the Average True Range indicator, offering traders a structured way to manage risk and profit potential.

█ THANKS

Special thanks to Cryptosnagger for taking the time to build this Pine Script and share it freely with the community.