Reversal Scalping Ribbon - Adib NooraniThe Reversal Scalping Ribbon is a trend-following overlay tool designed to visually identify potential reversal zones based on price extremes and dynamic volatility bands. It calculates adaptive upper and lower bands using price action and custom ATR logic, helping traders quickly assess market direction and possible turning points

🔹 Volatility-adjusted bands based on price highs/lows

🔹 Color-coded ribbons to indicate trend bias and potential reversal shifts

🔹 No repainting, works on all timeframes and assets

🔹 Visual-only display, no trade signals — supports discretion-based entries

This ribbon is designed for scalpers and intraday traders to spot reversal setups with clarity. It enhances your trading by showing real-time market bias without unnecessary distractions. By focusing on probabilities, it helps to improve decision-making in fast-paced environments

How to use the indicator efficiently

For Reversal Trading:

Buy: When price closes below the green ribbon with a red candle, then re-enters with a green candle. Enter above the high of the green candle with a stop loss below the lowest low of the recent green/red candles

Sell: When price closes above the red ribbon with a green candle, then re-enters with a red candle. Enter below the low of the red candle with a stop loss above the highest high of the recent red/green candles

Risk Management:

Limit risk to 0.5% of your capital per trade

Take 50% profit at a 1:1 risk-reward ratio

For the remaining 50%, trail using the lower edge of the green band for buys and the upper edge of the red band for sells

Educational

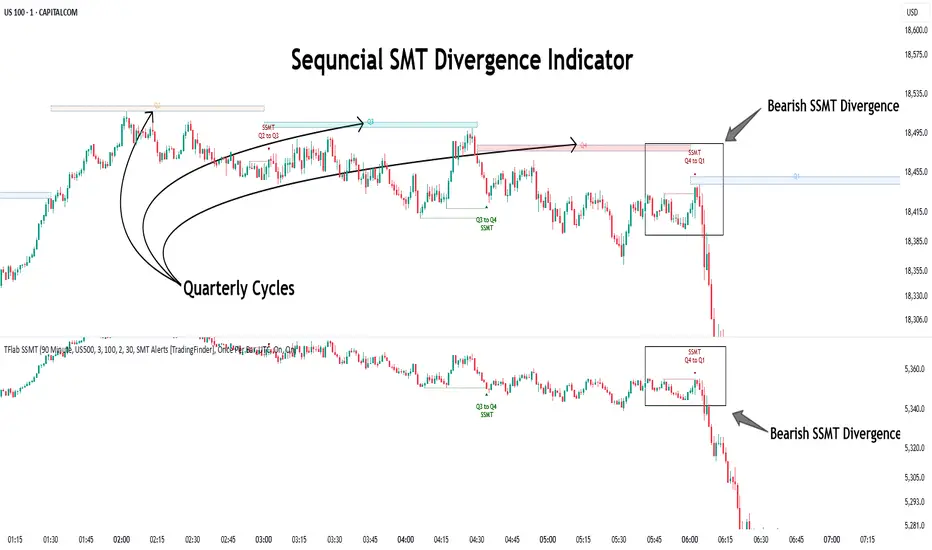

Quarterly Theory ICT 04 [TradingFinder] SSMT 4Quarter Divergence🔵 Introduction

Sequential SMT Divergence is an advanced price-action-based analytical technique rooted in the ICT (Inner Circle Trader) methodology. Its primary objective is to identify early-stage divergences between correlated assets within precise time structures. This tool not only breaks down market structure but also enables traders to detect engineered liquidity traps before the market reacts.

In simple terms, SMT (Smart Money Technique) occurs when two correlated assets—such as indices (ES and NQ), currency pairs (EURUSD and GBPUSD), or commodities (Gold and Silver)—exhibit different reactions at key price levels (swing highs or lows). This lack of alignment is often a sign of smart money manipulation and signals a lack of confirmation in the ongoing trend—hinting at an imminent reversal or at least a pause in momentum.

In its Sequential form, SMT divergences are examined through a more granular temporal lens—between intraday quarters (Q1 through Q4). When SMT appears at the transition from one quarter to another (e.g., Q1 to Q2 or Q3 to Q4), the signal becomes significantly more powerful, often aligning with a critical phase in the Quarterly Theory—a framework that segments market behavior into four distinct phases: Accumulation, Manipulation, Distribution, and Reversal/Continuation.

For instance, a Bullish SMT forms when one asset prints a new low while its correlated counterpart fails to break the corresponding low from the previous quarter. This usually indicates absorption of selling pressure and the beginning of accumulation by smart money. Conversely, a Bearish SMT arises when one asset makes a higher high, but the second asset fails to confirm, signaling distribution or a fake-out before a decline.

However, SMT alone is not enough. To confirm a true Market Structure Break (MSB), the appearance of a Precision Swing Point (PSP) is essential—a specific candlestick formation on a lower timeframe (typically 5 to 15 minutes) that reveals the entry of institutional participants. The combination of SMT and PSP provides a more accurate entry point and better understanding of premium and discount zones.

The Sequential SMT Indicator, introduced in this article, dynamically scans charts for such divergence patterns across multiple sessions. It is applicable to various markets including Forex, crypto, commodities, and indices, and shows particularly strong performance during mid-week sessions (Wednesdays and Thursdays)—when most weekly highs and lows tend to form.

Bullish Sequential SMT :

Bearish Sequential SMT :

🔵 How to Use

The Sequential SMT (SSMT) indicator is designed to detect time and structure-based divergences between two correlated assets. This divergence occurs when both assets print a similar swing (high or low) in the previous quarter (e.g., Q3), but in the current quarter (e.g., Q4), only one asset manages to break that swing level—while the other fails to reach it.

This temporal mismatch is precisely identified by the SSMT indicator and often signals smart money activity, a market phase transition, or even the presence of an engineered liquidity trap. The signal becomes especially powerful when paired with a Precision Swing Point (PSP)—a confirming candle on lower timeframes (5m–15m) that typically indicates a market structure break (MSB) and the entry of smart liquidity.

🟣 Bullish Sequential SMT

In the previous quarter, both assets form a similar swing low.

In the current quarter, one asset (e.g., EURUSD) breaks that low and trades below it.

The other asset (e.g., GBPUSD) fails to reach the same low, preserving the structure.

This time-based divergence reflects declining selling pressure, potential absorption, and often marks the end of a manipulation phase and the start of accumulation. If confirmed by a bullish PSP candle, it offers a strong long opportunity, with stop-losses defined just below the swing low.

🟣 Bearish Sequential SMT

In the previous quarter, both assets form a similar swing high.

In the current quarter, one asset (e.g., NQ) breaks above that high.

The other asset (e.g., ES) fails to reach that high, remaining below it.

This type of divergence signals weakening bullish momentum and the likelihood of distribution or a fake-out before a price drop. When followed by a bearish PSP candle, it sets up a strong shorting opportunity with targets in the discount zone and protective stops placed above the swing high.

🔵 Settings

⚙️ Logical Settings

Quarterly Cycles Type : Select the time segmentation method for SMT analysis.

Available modes include: Yearly, Monthly, Weekly, Daily, 90 Minute, and Micro.

These define how the indicator divides market time into Q1–Q4 cycles.

Symbol : Choose the secondary asset to compare with the main chart asset (e.g., XAUUSD, US100, GBPUSD).

Pivot Period : Sets the sensitivity of the pivot detection algorithm. A smaller value increases responsiveness to price swings.

Activate Max Pivot Back : When enabled, limits the maximum number of past pivots to be considered for divergence detection.

Max Pivot Back Length : Defines how many past pivots can be used (if the above toggle is active).

Pivot Sync Threshold : The maximum allowed difference (in bars) between pivots of the two assets for them to be compared.

Validity Pivot Length : Defines the time window (in bars) during which a divergence remains valid before it's considered outdated.

🎨 Display Settings

Show Cycle :Toggles the visual display of the current Quarter (Q1 to Q4) based on the selected time segmentation

Show Cycle Label : Shows the name (e.g., "Q2") of each detected Quarter on the chart.

Show Bullish SMT Line : Draws a line connecting the bullish divergence points.

Show Bullish SMT Label : Displays a label on the chart when a bullish divergence is detected.

Bullish Color : Sets the color for bullish SMT markers (label, shape, and line).

Show Bearish SMT Line : Draws a line for bearish divergence.

Show Bearish SMT Label : Displays a label when a bearish SMT divergence is found.

Bearish Color : Sets the color for bearish SMT visual elements.

🔔 Alert Settings

Alert Name : Custom name for the alert messages (used in TradingView’s alert system).

Message Frequency :

All: Every signal triggers an alert.

Once Per Bar: Alerts once per bar regardless of how many signals occur.

Per Bar Close: Only triggers when the bar closes and the signal still exists.

Time Zone Display : Choose the time zone in which alert timestamps are displayed (e.g., UTC).

Bullish SMT Divergence Alert : Enable/disable alerts specifically for bullish signals.

Bearish SMT Divergence Alert : Enable/disable alerts specifically for bearish signals

🔵 Conclusion

The Sequential SMT (SSMT) indicator is a powerful and precise tool for identifying structural divergences between correlated assets within a time-based framework. Unlike traditional divergence models that rely solely on sequential pivot comparisons, SSMT leverages Quarterly Theory, in combination with concepts like liquidity sweeps, market structure breaks (MSB) and precision swing points (PSP), to provide a deeper and more actionable view of market dynamics.

By using SSMT, traders gain not only the ability to identify where divergence occurs, but also when it matters most within the market cycle. This empowers them to anticipate major moves or traps before they fully materialize, and position themselves accordingly in high-probability trade zones.

Whether you're trading Forex, crypto, indices, or commodities, the true strength of this indicator is revealed when used in sync with the Accumulation, Manipulation, Distribution, and Reversal phases of the market. Integrated with other confluence tools and market models, SSMT can serve as a core component in a professional, rule-based, and highly personalized trading strategy.

GranDoc - Week, Day, Month, and Session Separator5Indicator Name: GranDoc's - Week, Day, Month, and Session Separator

Version: Pine Script v5

Author: Jonpaul Nnamdi Opara (GranDoc )

Description

The "GranDoc - Week, Day, Month, and Session Separator" is a highly customizable TradingView indicator designed to enhance chart analysis by visually marking critical time-based transitions. Developed by Jonpaul Nnamdi Opara, this tool plots vertical lines with labels or background highlights to denote the start and end of weeks, days, months, and major trading sessions (Frankfurt, London, NY Morning, NY Afternoon, Sydney, and Tokyo). Traders can tailor colors, line styles, widths, transparency, and session times to align with their strategies and timezones.

Ideal for forex, stocks, futures, and crypto traders, this indicator simplifies the identification of key market periods—such as session openings/closings or new weeks—that often signal increased volatility or trend shifts. It’s optimized for intraday timeframes for session separators but supports all timeframes for week, day, and month markers, making it a versatile addition to any trader’s toolkit.

Features

Week Separators: Marks Monday starts with customizable lines and "Week Start" labels.

Day Separators: Highlights daily openings with lines and "Day Start" labels.

Month Separators: Indicates new months with lines and "Month Start" labels.

Session Separators: Plots lines and labels for major trading sessions’ start and end:

Frankfurt (default: 07:00–15:00 UTC)

London (default: 08:00–16:00 UTC)

NY Morning (default: 13:00–16:00 UTC)

NY Afternoon (default: 16:00–21:00 UTC)

Sydney (default: 22:00–06:00 UTC)

Tokyo (default: 00:00–08:00 UTC)

Timezone Support: Adjusts session times with a UTC offset (±12 hours).

Display Flexibility : Toggle between labeled vertical lines or background highlights.

Customization: Fine-tune colors, line styles (solid, dashed, dotted), widths, and transparency.

Background Mode: Highlights periods with translucent backgrounds for cleaner charts.

[ i]Labeled Lines: Each line includes descriptive labels (e.g., "London Open", "Tokyo Closed") when not in background mode.

How to Use

Add to Chart:

Copy the script into TradingView’s Pine Editor.

Click "Add to Chart" to apply the indicator.

Customize Settings:

Open settings via double-click or the "Settings" gear icon.

Timezone Offset: Set your UTC offset (e.g., -5 for EST) to align sessions.

Toggles: Enable/disable week, day, month, or session separators.

Appearance: Adjust colors, line styles, widths, and transparency for each separator.

Session Times: Modify start/end hours and minutes if defaults don’t suit your market.

Background Mode: Enable "Show as Background" for colored backgrounds instead of lines, and tweak "Session Background Transparency."

Labels: Labeled lines (e.g., "Sydney Open") appear automatically unless background mode is active.

Chart Compatibility:

Session separators require intraday timeframes (e.g., 1-minute to 4-hour).

Week, day, and month separators work across all timeframes.

Confirm your chart’s timezone aligns with your analysis.

Analyze:

Use separators to pinpoint session transitions, daily openings, or weekly shifts for trade planning.

Labels make it easy to spot key periods on busy charts.

Pair with indicators like RSI, volume, or support/resistance for deeper insights.

Example Use Cases

Forex Trading: Highlight London and NY session opens/closes for high-liquidity entries.

Day Trading: Reset strategies at daily separators and monitor intraday volatility.

Swing Trading: Use week/month separators to track longer-term trends.

Session Focus: Isolate sessions like Tokyo for regional market analysis.

Chart Clarity: Background mode declutters charts while marking key times.

Notes

Session separators are disabled on daily+ timeframes to prevent clutter.

Verify timezone offset for accurate session alignment.

Background mode suits lower timeframes for readability.

Labels are visible only when background mode is disabled.

Feedback

Share your thoughts or suggestions to make this indicator even better! Reach out via TradingView or connect with the author for insights. Happy trading!

About the Author

Dr. Jonpaul Nnamdi Opara, a PhD graduate from Ehime University, Japan, is a researcher and developer specializing in AI and machine learning. His work on automated landslide mapping and defect detection, published in journals like GEOMATE, showcases his precision-driven approach. With the "GranDoc" indicator, Jonpaul brings intuitive, data-driven clarity to financial markets, reflecting his expertise in creating impactful tools.

Average Entry Price Calculator# Average Entry Price Calculator

This powerful indicator helps you track your average entry price across multiple positions, displaying it clearly on your chart with customizable lines and labels.

## Features:

• Calculate average entry price for up to 5 different positions

• Display current price and profit/loss calculations

• Show percentage and absolute change from your average entry

• Customizable line styles, colors, and label positions

• Track your entry prices with clear visual references

## How It Works:

Enter your position details (entry price and amount in USDT), and the indicator will calculate your average entry price, displaying it as a horizontal line on your chart. The indicator also shows your individual entry prices as separate lines, making it easy to visualize your overall position.

## Perfect For:

• DCA (Dollar-Cost Averaging) strategies

• Position tracking across multiple entries

• Risk management and profit taking

• Visualizing entry zones on your chart

## Instructions:

1. Add the indicator to your chart

2. Enter your position details (price and amount)

3. Customize the visual appearance as needed

4. Use the displayed average entry line for decision making

All calculations are done locally in your browser - no sensitive data is transmitted or stored.

Enjoy more informed trading decisions with this essential position tracking tool!

Quarters Theory Levels (Yotov Style)John Alex Sagwe's Quarters Theory Levels Script

This Pine Script, developed by John Alex Sagwe, is based on the concept of the "Quarters Theory" popularized by Illan Yotov. It aims to help traders identify key levels in the market using whole, half, and quarter-level calculations. The script plots major whole levels, half levels, and quarter levels above and below the current price, allowing traders to visualize potential price points where significant market action might occur.

The customizable parameters allow you to:

Set the base level and step size (for quarter levels),

Adjust the number of levels above and below the current price to be displayed,

Toggle between showing whole, half, or quarter levels,

Use price alerts when the market price nears these levels.

Whether you’re a novice or an experienced trader, this script can help you integrate the Quarters Theory into your trading strategy. It’s designed to be flexible and user-friendly, helping you visualize key market levels with ease.

Developed by: John Alex Sagwe, an avid trader and Pine Script enthusiast.

Win-Loss Streak PlotterWin-Loss Streak Plotter

This indicator tracks the win/loss streaks of moving average crossovers (using simple moving averages for illustration purposes). It calculates the price change after each crossover, marking each as a win (green) or loss (red). The win rate is shown separately.

Inputs:

Source: Price series (default: open)

Fast MA: Fast moving average (default: open)

Slow MA: Slow moving average (default: open)

Total Crosses to Analyze: Number of crossovers to track

Crosses per Row: Number of crossovers per row in the table

Output:

A table displays each crossover’s result (win/loss).

A separate win rate table shows the percentage of wins.

Suggestions are always welcomed!

Candle Trend PowerThe Candle Trend Power is a custom technical indicator designed for advanced trend analysis and entry signal generation. It combines multiple smoothing methods, candle transformations, and volatility bands to visually and analytically enhance your trading decisions.

🔧 Main Features:

📉 Custom Candle Types

It transforms standard OHLC candles into one of several advanced types:

Normal Candles, Heikin-Ashi, Linear Regression, Rational Quadratic (via kernel filtering), McGinley Dynamic Candles

These transformations help traders better see trend continuations and reversals by smoothing out market noise.

🧮 Smoothing Method for Candle Data

Each OHLC value can be optionally smoothed using:

EMA, SMA, SMMA (RMA), WMA, VWMA, HMA, Mode (Statistical mode) Or no smoothing at all.

This flexibility is useful for customizing to different market conditions.

📊 Volatility Bands

Volatility-based upper and lower bands are calculated using:

Band = price ± (price% + ATR * multiplier)

They help identify overbought/oversold zones and potential reversal points.

📍 Candle Color Logic

Each candle is colored:

Cyan (#00ffff) if it's bullish and stronger than the previous candle

Red (#fd0000) if it's bearish and weaker

Alternating bar index coloring improves visual clarity.

📈 Trend Momentum Labels

The script includes a trend strength estimation using a smoothed RSI:

If the candle is bullish, it shows a BUY label with the overbought offset.

If bearish, it shows a SELL label with the oversold offset.

These labels are dynamic and placed next to the bar.

📍 Signal Markers

It also plots triangles when the price crosses the volatility bands:

Triangle up for potential long

Triangle down for potential short

✅ Use Case Summary

This script is mainly used for:

Visual trend confirmation with enhanced candles

Volatility-based entry signals

RSI-based trend momentum suggestions

Integrating different smoothing & transformation methods to fine-tune your strategy

It’s a flexible tool for both manual traders and automated system developers who want clear, adaptive signals across different market conditions.

💡 What's Different

🔄 Candle Type Transformations

⚙️ Custom Candle Smoothing

📉 Candle's Multi-level Volatility Bands

🔺 Dynamic Entry Signals (Buy/Sell Labels)

❗Important Note:

This script is provided for educational purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

Webby's Market OrderThis is visual representation of Webby's Market Order.

When three consecutive lows are above 21 EMA, Uptrend expectation is natural.

When three highs are below 21 EMA, Downtrend expectation is natural.

Alert Conditions can be set when uptrend and down trend are expected.

Use this indicator with IXIC or SPY or major indices.

This is set at three lows/Highs above 21 EMA as looked by Mike Webster.

Weekly Open (Current Week Only)📘 Indicator Name: Weekly Open (Current Week Only)

📝 Description:

This indicator plots a horizontal line representing the weekly open price, visible only during the current trading week. At the beginning of each new week (based on TradingView’s weekly time segmentation), the indicator captures the open price of the first candle and draws a constant line across the chart until the week ends. Once the new week begins, the line resets and updates with the new weekly open.

🎯 How to Use – ICT Concepts Integration (Weekly Profile):

This tool is designed to complement ICT (Inner Circle Trader) trading strategies, particularly within the weekly profile framework, by offering a clear and persistent visual of the weekly open, which is a critical reference point in ICT’s market structure theory.

✅ Use Cases:

Directional Bias:

According to ICT concepts, price trading above the weekly open suggests a bullish bias for the week, while trading below it implies bearish conditions.

Traders can use the weekly open line to align their intraweek trades with higher timeframe directional bias.

Dealing Ranges:

Weekly open helps frame the weekly dealing range, especially when combined with other levels like weekly high/low or previous week’s range.

It allows traders to identify potential liquidity pools or areas where price may seek to rebalance.

Mean Reversion Entries:

Price often reverts to or reacts from the weekly open. Traders may use this as a target or entry level, particularly during Monday/Tuesday setups.

Works well in conjunction with concepts like OTE (Optimal Trade Entry) and Judas Swings.

Risk Management:

Acts as a clean and visual anchor to structure stop losses or take-profits based on weekly bias shifts.

Relative Strength MatrixThe Relative Strength Matrix (RSPS M) is a powerful comparison tool that analyzes and ranks up to 10 selected assets based on their relative performance. It does this by calculating price ratios between all asset pairs and applying a consistent strength criterion across each comparison. The results are displayed in a live-updating matrix, showing how each asset performs relative to the rest of the group.

By default, the indicator uses a momentum-based approach (via RSI) to evaluate strength, but it’s fully customizable. Users can modify the valuation logic by replacing the built-in ta.rsi function under the “Inputs your criterion below” section in the code. This makes the tool highly flexible—allowing for different styles of comparison such as trend-following, volatility-adjusted, or custom factor-based ranking methods.

Each asset’s total dominance score is color-coded and ranked, making it easy to spot outperformers and underperformers within any chosen basket. Whether you're tracking crypto pairs, sectors, or other groups, RSPS M provides a clear, objective framework for relative strength monitoring and rotation strategies—perfect for spotting leaders, laggards, and shifts in momentum across markets.

Multi Candle Body MapperMulti Candle Body Mapper

Visualize higher-timeframe candle structure within lower timeframes — without switching charts.

This tool maps grouped candle bodies and wicks (e.g., 15min candles on a 5min chart) using precise boxes and lines. Ideal for intraday traders who want to analyze market intent, body bias, and wick rejection in a compressed, organized view.

Features:

Visualize 3, 6, or 12 candle groups (e.g., 15min / 30min / 1H views)

Body box shows bullish/bearish color with adjustable transparency

Wick box shows high-low range with adjustable thickness and color

Dashed line at group close level for market direction hint

Full color customization

Toggle individual elements ON/OFF

Clean overlay – doesn’t interfere with price candles

Great for spotting:

Hidden support/resistance

Momentum buildup

Reversal traps and continuation setups

Keep your chart simple but smarter — all without changing your timeframe.

Percent from And To All Time High,Indicator: Percent from All Time High - Raised Label

Overview:

This indicator shows the percentage difference between the current price of an asset and its all-time high (ATH). It displays these percentages in a raised label at the top of the chart. Additionally, the last price and the percentage difference to ATH are displayed in a table.

Features:

Displays the percentage difference from ATH (From ATH) and the percentage difference to ATH (To ATH) in a table.

The Last Price is shown along with the percentage difference.

The data is dynamically updated with the current price, and it will always show the latest information.

Visualizes price movements with colored bars to indicate price direction.

Vwap Vision #WhiteRabbitVWAP Vision #WhiteRabbit

This Pine Script (version 5) script implements a comprehensive trading indicator called "VWAP Vision #WhiteRabbit," designed for analyzing price movements using the Volume-Weighted Average Price (VWAP) along with multiple customizable features, including adjustable color themes for better visual appeal.

Features:

Customizable Color Themes:

Choose from four distinct themes: Classic, Dark Mode, Fluo, and Phil, enhancing the visual layout to match user preferences.

VWAP Calculation:

Uses standard VWAP calculations based on selected anchor periods (Session, Week, Month, etc.) to help identify price trends.

Band Settings:

Multiple bands are calculated based on standard deviations or percentages, with customization options to configure buy/sell zones and liquidity levels.

Buy/Sell Signals:

Generates clear buy and sell signals based on price interactions with the calculated bands and the exponential moving average (EMA).

Real-time Data Display:

Displays real-time signals and VWAP values for selected trading instruments, including XAUUSD, NAS100, and BTCUSDT, along with related alerts for trading opportunities.

Volatility Analysis:

Incorporates volatility metrics using the Average True Range (ATR) to assess market conditions and inform trading decisions.

Enhanced Table Displays:

Provides tables for clear visualization of trading signals, real-time data, and performance metrics.

This script is perfect for traders looking to enhance their analysis and gain insights for making informed trading decisions across various market conditions.

Hamid Double RSIRSI with Moving Average and Another RSI

This script combines two Relative Strength Index (RSI) indicators with configurable moving averages. It allows traders to track momentum and market strength with adjustable periods for both the RSI and moving averages. The script also allows you to choose different data sources for each RSI, offering flexibility in analysis.

Features:

Two RSIs: One with a shorter period and another with a longer period .

Moving Averages: Each RSI has its own configurable moving average . The moving averages help smooth out the RSI and provide clearer trends.

Customizable Inputs: Adjust the RSI period and the length of the moving averages. You can also choose different sources for each RSI (e.g., close, open, high, low).

Mid Line: A horizontal line at 50, which is commonly used as the neutral level for the RSI. It helps identify whether the RSI is above or below neutral, indicating bullish or bearish conditions.

Overbought and Oversold Levels: Horizontal lines at 70 (overbought) and 30 (oversold) to highlight when the asset might be overbought or oversold according to the RSI.

How it works:

RSI Calculation: The script calculates two RSIs using different lengths

Moving Averages: A Simple Moving Average (SMA) is applied to both RSIs to smooth their values and help identify trends.

Overbought/Oversold Indicators: The script includes horizontal lines at 70 and 30 to show overbought and oversold conditions. The mid line is plotted at 50 to highlight neutral levels.

This indicator is useful for traders who want to compare the behavior of two RSIs over different time periods and use the moving averages to filter out noise. The ability to customize the source data for each RSI makes this script adaptable to different trading strategies.

Intraday LevelsWhat it shows:

This indicator is useful for day trading, where it will track and display you important price levels which includes:

Premarket Low (PML)

Premarket High (PMH)

Previous Day Low (PDL)

Previous Day High (PDH)

Previous Day Close (PDC)

After Hours Low (AHL)

After Hours High (AHH)

Day Low (DL)

Day High (DH)

The price level lines and labels will automatically adjust itself as the price moves, eliminating the need of manually having to adjusting these levels.

How to use it:

At these levels it can act as important support resistance points during the day and can often serve as a important pivot point for any ticker. You can expect price rejection or bounce when the price approaches these levels.

Key settings:

For each of the levels, user can adjust in the settings menu:

Line Colour

Line Thickness

Line Style

Label Text

Price Labelling on Label

Label Location (Offset from current bar)

Ability to turn on/off the price level and label

Display levels for either all days or on the day

Mercury Venus Conjunction Sextiles 2019-2026How to Use It and What It Means Astrologically

How to Use the Script in TradingView

This Pine Script, called "Mercury Venus Aspects 2019–2026," is made to highlight the dates of Mercury-Venus conjunctions (0°) and sextiles (60°) from 2019 to 2026 on TradingView charts. Here's how to use it:

click “Add to Chart.” It will apply to any chart you have open—stocks, forex, crypto, etc.

Customize the Display

You can turn on/off the visibility of conjunctions and sextiles using checkboxes under "Inputs" in the settings.

You can also adjust the label size (small, normal, large, or huge) for better readability on your chart.

What You’ll See on the Chart

Conjunctions appear as blue shaded zones with labels like “C1,” “C2,” etc. These mark dates when Mercury and Venus are at the same degree.

Sextiles show up in orange with labels like “S1,” “S2,” marking when they’re about 60° apart.

Each event spans a 2-day window (one day before and after the exact aspect).

How to Use It Practically

You can overlay the script on market charts to look for any patterns between these planetary aspects and price movements.

You can also use it to plan personal or financial activities, since these aspects often affect communication, money, and relationships.

What to Keep in Mind

Dates are approximate and based on average planetary cycles (Mercury: ~88 days, Venus: ~225 days). For exact timing, use an ephemeris.

Only conjunctions and sextiles are shown. Oppositions, squares, and trines aren’t included because Mercury and Venus never get far enough apart (more than 75°).

This script is great for astrologers, traders, and enthusiasts who want to see Mercury-Venus aspects directly on their charts and explore their possible effects.

Astrological Meaning of Mercury-Venus Aspects

What Mercury and Venus Represent

Mercury rules communication, thinking, technology, travel, and trade. In global events (mundane astrology), it affects media, markets, and movement of information.

Venus is about love, beauty, money, and pleasure. It influences relationships, aesthetics, and finance. In the world stage, it’s linked to luxury, art, fashion, and economic balance.

When Mercury and Venus form aspects (like conjunctions or sextiles), their energies mix in helpful ways that can affect people and events.

Conjunction (0°) – Mercury and Venus Together

These two planets are in the same sign and degree, so their qualities merge.

For people:

Positive: Smooth communication, charm, creativity, and better relationships. Great for romance, art, and social interaction.

Negative: Too much focus on appearances, sweet talk, or pleasure can cloud judgment. Decisions may lack depth.

For the economy:

Positive: Boosts in media, entertainment, fashion, and tech. Good for trade, deals, and optimism in financial markets.

Negative: Risk of overspending or unrealistic expectations. May cause small market bubbles or misleading hype.

Sextile (60°) – Mercury and Venus in Harmony

These two planets are two signs apart, creating a smooth, supportive energy.

For people:

Positive: Easy conversations, creative teamwork, small financial wins, and pleasant social experiences.

Negative: Energy is mild, so opportunities might be missed if not acted on. People may avoid hard decisions.

For the economy:

Positive: Gradual improvements in areas like marketing, social media, hospitality, and design. Good for diplomacy.

Negative: Lack of strong initiative could limit bigger gains. Minor missteps are possible due to a laid-back attitude.

General Effects

These aspects are mostly beneficial. They support creativity, financial thinking, and social harmony.

Downsides: Conjunctions may lead to overindulgence or shallow choices, while sextiles may cause missed chances due to low energy.

These aspects rarely cause major economic shifts on their own but can amplify trends depending on other planetary influences (like Saturn or Uranus).

Zodiac Sign Influence

Fire signs (Aries, Leo, Sagittarius): Bold communication, energetic spending, gains in media or entertainment.

Earth signs (Taurus, Virgo, Capricorn): Practical results, stable finances, growth in real-world assets like property or food.

Air signs (Gemini, Libra, Aquarius): Intellectual growth, tech innovation, and social ideas flourish.

Water signs (Cancer, Scorpio, Pisces): Emotional depth in conversations, artistic growth, and financial sensitivity.

Mercury-Venus aspects are gentle but helpful. They combine logic (Mercury) with emotion and value (Venus). They’re good times for love, communication, and money—but their benefits depend on how we use the energy. This script lets you easily track these moments on a chart and explore how they might align with real-life trends or decisions.

Disclaimer: This script and its interpretations are for informational and educational purposes only. They do not constitute financial, trading, or professional astrological advice. Always conduct your own research and consult qualified professionals before making any financial or personal decisions. Use at your own discretion.

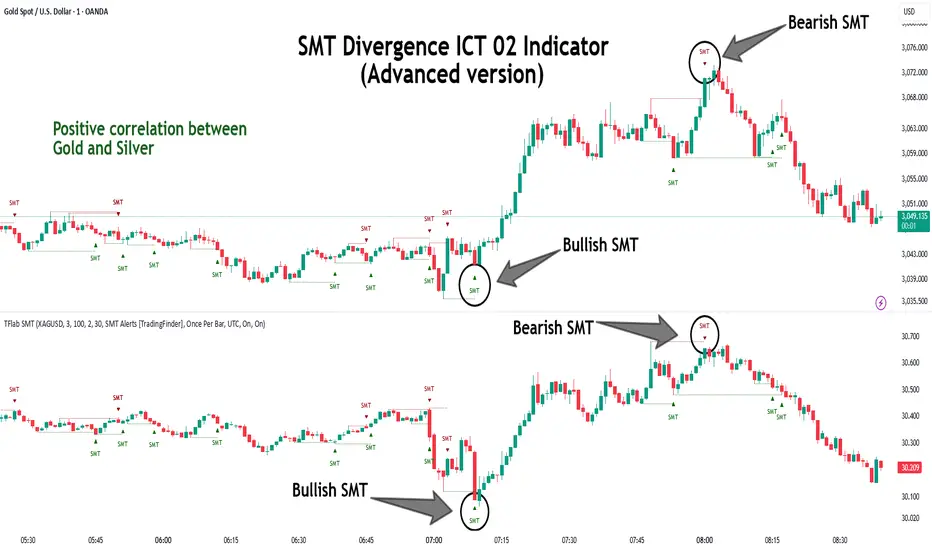

SMT Divergence ICT 02 [TradingFinder] Smart Money Technique SMC🔵 Introduction

SMT Divergence (Smart Money Technique Divergence) is a price action-based trading concept that detects discrepancies in market behavior between two assets that are generally expected to move in the same direction. Rooted in ICT (Inner Circle Trader) methodology, this approach helps traders recognize subtle signs of market manipulation or imbalance, often ahead of traditional indicators.

The core idea behind SMT divergence is simple: when two correlated instruments—such as currency pairs, indices, or assets from the same sector—start forming different swing points (highs or lows), this can reveal a lack of confirmation in the trend. Such divergence is often a precursor to a price reversal or pause in momentum.

This technique works effectively across various markets including Forex, stocks, and cryptocurrencies. It’s particularly valuable when used alongside concepts like liquidity sweeps, market structure breaks (MSBs), or order block identification.

In advanced use cases, Sequential SMT helps uncover patterns of alternating divergences across sessions, often signaling engineered liquidity traps before price reacts.

When combined with the Quarterly Theory—which segments market behavior into Accumulation, Manipulation, Distribution, and Continuation/Reversal phases—traders gain insight not only into where divergence happens, but when it's most likely to be significant within the market cycle.

Bullish SMT :

Bullish SMT Divergence occurs when one asset prints a higher low while the correlated asset forms a lower low. This asymmetry often suggests that the downside move is losing strength, hinting at a potential bullish shift.

Bearish SMT :

Bearish SMT Divergence is formed when one asset creates a higher high, while the second asset fails to confirm by printing a lower high. This typically signals weakening bullish pressure and the possibility of a reversal to the downside.

🔵 How to Use

The SMT Divergence indicator is designed to detect imbalances between two positively correlated assets—such as major currency pairs, indices, or commodities. These divergences often indicate early signs of market inefficiency or smart money manipulation and can help traders anticipate trend shifts with higher precision.

Unlike traditional divergence indicators or earlier versions of this script, this upgraded version does not rely solely on consecutive pivot comparisons. Instead, it dynamically scans all available pivots within the chart to identify divergences at any structural level—major or minor—across the price action. This broader detection method increases the reliability and frequency of meaningful SMT signals.

Moreover, when integrated with Sequential SMT logic, the indicator is capable of identifying multiple divergence sequences across sessions. These sequences often signal engineered liquidity traps and can be mapped within the Quarterly Theory framework, allowing traders to pinpoint not just the presence of divergence but also the phase of the market cycle it appears in (Accumulation, Manipulation, Distribution, or Continuation).

🟣 Bullish SMT Divergence

This signal occurs when the primary asset forms a higher low, while the correlated asset forms a lower low. This pattern implies weakening bearish momentum and a potential shift to the upside.

If the correlated asset breaks its previous low but the primary asset does not, this divergence suggests absorption of selling pressure and possible accumulation by smart money—making it a strong bullish signal, especially when aligned with a favorable market phase (e.g., the end of a manipulation phase in Q2).

🟣 Bearish SMT Divergence

This signal occurs when the primary asset creates a higher high, while the correlated asset forms a lower high. This mismatch indicates fading bullish momentum and a potential reversal to the downside.

If the correlated asset fails to confirm a breakout made by the main asset, the divergence may point to distribution or exhaustion. When seen within Q3 or Q4 phases of the Quarterly Theory, this pattern often precedes sharp declines or fake-outs engineered by smart money

🔵 Settings

⚙️ Logical Settings

Symbol : Choose the secondary asset to compare with the main chart asset (e.g., XAUUSD, US100, GBPUSD).

Pivot Period : Sets the sensitivity of the pivot detection algorithm. A smaller value increases responsiveness to price swings.

Activate Max Pivot Back : When enabled, limits the maximum number of past pivots to be considered for divergence detection.

Max Pivot Back Length : Defines how many past pivots can be used (if the above toggle is active).

Pivot Sync Threshold : The maximum allowed difference (in bars) between pivots of the two assets for them to be compared.

Validity Pivot Length : Defines the time window (in bars) during which a divergence remains valid before it's considered outdated.

🎨 Display Settings

Show Bullish SMT Line : Draws a line connecting the bullish divergence points.

Show Bullish SMT Label : Displays a label on the chart when a bullish divergence is detected.

Bullish Color : Sets the color for bullish SMT markers (label, shape, and line).

Show Bearish SMT Line : Draws a line for bearish divergence.

Show Bearish SMT Label : Displays a label when a bearish SMT divergence is found.

Bearish Color : Sets the color for bearish SMT visual elements.

🔔 Alert Settings

Alert Name : Custom name for the alert messages (used in TradingView’s alert system).

Message Frequency :

All : Every signal triggers an alert.

Once Per Bar : Alerts once per bar regardless of how many signals occur.

Per Bar Close : Only triggers when the bar closes and the signal still exists.

Time Zone Display : Choose the time zone in which alert timestamps are displayed (e.g., UTC).

Bullish SMT Divergence Alert : Enable/disable alerts specifically for bullish signals.

Bearish SMT Divergence Alert : Enable/disable alerts specifically for bearish signals

🔵Conclusion

The SMT Plus indicator offers a refined and powerful approach to detecting smart money behavior through divergence analysis between correlated assets. By removing the limitations of consecutive pivot comparisons and allowing for broader structural detection, it captures more accurate and timely signals that often precede major market moves.

When paired with frameworks like Sequential SMT and the Quarterly Theory, the indicator not only highlights where divergence occurs, but also when in the market cycle it's most likely to matter. Its flexible settings, customizable visuals, and integrated alert system make it suitable for intraday scalpers, swing traders, and even long-term macro analysts.

Whether you're using it as a standalone decision-making tool or combining it with other ICT concepts, SMT Plus gives you an edge in recognizing manipulation, timing reversals, and staying in sync with the real market narrative—not just the chart.

Ross Cameron-Inspired Day Trading StrategyExplanation for Community Members:

Title: Ross Cameron-Inspired Day Trading Strategy

Description:

This script is designed to help you identify potential buy and sell opportunities during the trading day. It combines several popular trading strategies to provide clear signals.

Key Features:

Gap and Go: Identifies stocks that have gapped up or down at the open.

Momentum Trading: Uses RSI and EMA to identify momentum-based entry points.

Mean Reversion: Uses RSI and SMA to identify potential reversals.

How to Use:

Apply to Chart: Add this script to your TradingView chart.

Set Timeframe: Works best on 5-minute and 10-minute timeframes.

Watch for Signals: Look for green "BUY" labels for entry points and red "SELL" labels for exit points.

Parameters:

Gap Percentage: Adjust to identify larger or smaller gaps.

RSI Settings: Customize the RSI length and overbought/oversold levels.

EMA and SMA Lengths: Adjust the lengths of the moving averages.

Confirmation Period: Set how many bars to wait for confirmation.

Visual Elements:

BUY Signals: Green labels below the price bars.

SELL Signals: Red labels above the price bars.

Indicators: Displays EMA (blue) and SMA (orange) for additional context.

This script is a powerful tool for day trading on NSE and BSE indices, combining multiple strategies to provide robust trading signals. Adjust the parameters to suit your trading style and always combine with your own analysis for best results.

Gann Percentage of High & Low Prices for Options - Keanu_RiTzThis Indicator is based on the text from Chapter 4 "Percentage of High & Low Prices" page number "30" from the book "WD Gann 45 years in Wall Street".

This Indicator is to be used on Intraday Timeframes and only on Options Charts (CALL & PUT) and not on any other chart.

The following is the text from that page :-

One of the greatest discoveries I ever made was how to figure the percentage of high and low prices on the averages and individual stocks.

The percentages of extreme high and low levels indicate future resistance levels.

There is a relation between every low price to some future high price and a percentage of the low price indicates what levels to expect the next high price.

At this price you can sell out long stocks and sell short with a limited risk.

The extreme high price or any minor tops are related to future bottoms er low levels.

The percentage of the high price tells where to expect low prices in the future and gives you resistance levels where you can buy with a limited risk.

The most important resistance level is 50% of any high or low price.

Second in importance is 100% on the lowest selling price on the averages or individual stocks.

You must also use 200%, 300%, 400%, 500%, 600% or more, depending upon the price and the Time Periods from High and Low.

Third in importance is 25% of the Lowest price or the Highest price.

Fourth in importance is 121/2% of the extreme Low or extreme High price.

Fifth in importance is 61/4% of the Highest price, but this is only to be used when the averages or individual stocks are selling at very high levels.

Sixth in importance is 33 1/3 and 66 2/3%. These percentages should be calculated and watched for resistance next after 25% and after 50%.

You should always have percentage tables made up on the Industrial Averages and on the individual stocks you trade in in order to know where these important resistance levels are located.

Description :

It plots the Intraday % levels from the highest high and lowest low of that day.

The calculation of these levels is based on the text from Chapter 4 "Percentage of High & Low Prices" page number "30" from the book "WD Gann 45 years in Wall Street".

I developed this indicator to see if those percentages work on Options prices or not,

and from my observation I found that it works wonderfully in Options as well.

These % levels work like magic and act as great Dynamic Support and Resistance levels.

Don't trust my words blindly and see for yourself.

This indicator is for educational and research purpose only.

It does not provide any BUY/SELL signals.

Intrinsic Event (Multi DC OS)Overview

This indicator implements an event-based approach to analyze price movements in the foreign exchange market, inspired by the intrinsic time framework introduced in Fractals and Intrinsic Time - A Challenge to Econometricians by U. A. Müller et al. (1995). It identifies significant price events using an intrinsic time perspective and supports multi-agent analysis to reflect the heterogeneous nature of financial markets. The script plots these events as lines and labels on the chart, offering a visual tool for traders to understand market dynamics at different scales.

Key Features

Intrinsic Events : The indicator detects directional change (DC) and overshoot (OS) events based on user-defined thresholds (delta), aligning with the paper’s concept of intrinsic time (Section 6). Intrinsic time redefines time based on market activity, expanding during volatile periods and contracting during inactive ones, rather than relying on a physical clock.

Multi-Agent Analysis : Supports up to five agents, each with its own threshold and color settings, reflecting the heterogeneous market hypothesis (Section 5). This allows the indicator to capture the perspectives of market participants with different time horizons, such as short-term FX dealers and long-term central banks.

How It Works

Intrinsic Events Detection : The script identifies two types of events using intrinsic time principles:

Directional Change (DC) : Triggered when the price reverses by the threshold (delta) against the current trend (e.g., a drop by delta in an uptrend signals a "Down DC").

Overshoot (OS) : Occurs when the price continues in the trend direction by the threshold (e.g., a rise by delta in an uptrend signals an "Up OS").

DC events are plotted as solid lines, and OS events as dashed lines, with labels like "Up DC" or "OS Down" for clarity. The label style adjusts based on the trend to ensure visibility.

Multi-Agent Setup : Each agent operates independently with its own threshold, mimicking market participants with varying time horizons (Section 5). Smaller thresholds detect frequent, short-term events, while larger thresholds capture broader, long-term movements.

Settings

Each agent can be configured with:

Enable Agent : Toggle the agent on or off.

Threshold (%) : The percentage threshold (delta) for detecting DC and OS events (default values: 0.1%, 0.2%, 0.5%, 1%, 2% for agents 1–5).

Up Mode Color : Color for lines and labels in up mode (DC events).

Down Mode Color : Color for lines and labels in down mode (OS events).

Usage Notes

This indicator is designed for the foreign exchange market, leveraging its high liquidity, as noted in the paper (Section 1). Adjust the threshold values based on the instrument’s volatility—higher volatility leads to more intrinsic events (Section 4). It can be adapted to other markets where event-based analysis applies.

Reference

The methodology is based on:

Fractals and Intrinsic Time - A Challenge to Econometricians by U. A. Müller, M. M. Dacorogna, R. D. Davé, O. V. Pictet, R. B. Olsen, and J. R. Ward (June 28, 1995). Olsen & Associates Preprint.

YY Price LimitsThis Pine Script indicator is designed to visualize potential price limits (e.g., daily price limits used in some markets like commodities) on a TradingView chart. It calculates and plots lines representing percentage-based price limits above and below a reference price (typically the previous day's close). The indicator allows you to customize the displayed price limits, their appearance, and how they extend across the chart. It's particularly useful for intraday traders who need to be aware of potential price ceilings and floors.

Key Features:

Percentage-Based Limits:

Calculates price limits based on percentages (3%, 5%, and 7%) of a reference price.

Customizable Display:

Toggle visibility of reference price and each percentage limit (3%, 5%, 7%).

Customize the color, style (solid, dashed, dotted), and width of the price limit lines.

Extends Lines: Allows you to extend the price limit lines to the left, right, both directions, or not at all.

CME Reference Price: It is designed to plot price limits based on the CME (Chicago Mercantile Exchange) methodology, which uses the last close as the reference price. The tooltip reminds users to verify the actual reference price on the CME Group website.

Intraday Focus: The indicator is specifically designed for intraday timeframes, as it uses the previous day's close as the reference point.

Clear Visuals: Plots horizontal lines with labels indicating the price level and percentage.

Deadzone Pro @DaviddTechDeadzone Pro by @DaviddTech – Adaptive Multi-Strategy NNFX Trading System

Deadzone Pro by @DaviddTech is a meticulously engineered trading indicator that strictly adheres to the No-Nonsense Forex (NNFX) methodology. It integrates adaptive trend detection, dual confirmation indicators, advanced volatility filtering, and dynamic risk management into one powerful, visually intuitive system. Ideal for traders seeking precision and clarity, this indicator consistently delivers high-probability trade setups across all market conditions.

🔥 Key Features:

The Setup:

Adaptive Hull Moving Average Baseline: Clearly identifies trend direction using an advanced, gradient-colored Hull MA that intensifies based on trend strength, providing immediate visual clarity.

Dual Confirmation Indicators: Combines Waddah Attar Explosion (momentum detector) and Bull/Bear Power (strength gauge) for robust validation, significantly reducing false entries.

Volatility Filter (ADX): Ensures entries are only made during strong trending markets, filtering out weak, range-bound scenarios for enhanced trade accuracy.

Dynamic Trailing Stop Loss: Implements a SuperTrend-based trailing stop using adaptive ATR calculations, managing risk effectively while optimizing exits.

Dashboard:

💎 Gradient Visualization & User Interface:

Dynamic gradient colors enhance readability, clearly indicating bullish/bearish strength.

Comprehensive dashboard summarizes component statuses, real-time market sentiment, and entry conditions at a glance.

Distinct and clear buy/sell entry and exit signals, with adaptive stop-loss levels visually plotted.

Candlestick coloring based on momentum signals (Waddah Attar) for intuitive market reading.

📈 How to Interpret Signals:

Bullish Signal: Enter when Hull MA baseline trends upward, both confirmation indicators align bullish, ADX indicates strong trend (>25), and price breaks above the previous trailing stop.

Bearish Signal: Enter short or exit long when Hull MA baseline trends downward, confirmations indicate bearish momentum, ADX confirms trend strength, and price breaks below previous trailing stop.

📊 Recommended Usage:

Timeframes: Ideal on 1H, 4H, and Daily charts for swing trading; effective on shorter (5M, 15M) charts for day trading.

Markets: Compatible with Forex, Crypto, Indices, Stocks, and Commodities.

The Entry & Exit:

🎯 Trading Styles:

Choose from three distinct trading modes:

Conservative: Requires full alignment of all indicators for maximum accuracy.

Balanced (Default): Optimized balance between signal frequency and reliability.

Aggressive: Fewer confirmations needed for more frequent trading signals.

📝 Credits & Originality:

Deadzone Pro incorporates advanced concepts inspired by:

Hull Moving Average by @Julien_Eche

Waddah Attar Explosion by @LazyBear

Bull Bear Power by @Pinecoders

ADX methodology by @BeikabuOyaji

This system has been significantly refactored and enhanced by @DaviddTech to maximize synergy, clarity, and usability, standing apart distinctly from its original components.

Deadzone Pro exemplifies precision and discipline, aligning fully with NNFX principles to provide traders with a comprehensive yet intuitive trading advantage.

Circuit Breaker - MFFUThis Indicator Is Used To Protect User From Over Trading After Market Hit The Circuit Breakers.

The CME Exchange Usually Halts Trading If Market Hit + or - 7%.

To Protect Users From Extreme Volatile Condition MFFU, Halts Trading If Market Hits + or - 5%.

This Indicator helps us to plot the circuit breaking lines helping us to when to stop trading.