Smoothed RSI Backtest This is new version of RSI oscillator indicator, developed by John Ehlers.

The main advantage of his way of enhancing the RSI indicator is smoothing

with minimum of lag penalty.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Strategy

SMI Ergodic Oscillator Backtest ver.2 The SMI Ergodic Indicator is the same as the True Strength Index (TSI) developed by

William Blau, except the SMI includes a signal line. The SMI uses double moving averages

of price minus previous price over 2 time frames. The signal line, which is an EMA of the

SMI, is plotted to help trigger trading signals. Adjustable guides are also given to fine

tune these signals. The user may change the input (close), method (EMA), period lengths

and guide values.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

SMI Ergodic Oscillator Strategy ver.2 The SMI Ergodic Indicator is the same as the True Strength Index (TSI) developed by

William Blau, except the SMI includes a signal line. The SMI uses double moving averages

of price minus previous price over 2 time frames. The signal line, which is an EMA of the

SMI, is plotted to help trigger trading signals. Adjustable guides are also given to fine

tune these signals. The user may change the input (close), method (EMA), period lengths

and guide values.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

SMI Ergodic Oscillator Backtest The SMI Ergodic Indicator is the same as the True Strength Index (TSI) developed by

William Blau, except the SMI includes a signal line. The SMI uses double moving averages

of price minus previous price over 2 time frames. The signal line, which is an EMA of the

SMI, is plotted to help trigger trading signals. Adjustable guides are also given to fine

tune these signals. The user may change the input (close), method (EMA), period lengths

and guide values.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

RSI based on ROC Backtest This is the new-age indicator which is version of RSI calculated upon

the Rate-of-change indicator.

The name "Relative Strength Index" is slightly misleading as the RSI

does not compare the relative strength of two securities, but rather

the internal strength of a single security. A more appropriate name

might be "Internal Strength Index." Relative strength charts that compare

two market indices, which are often referred to as Comparative Relative Strength.

And in its turn, the Rate-of-Change ("ROC") indicator displays the difference

between the current price and the price x-time periods ago. The difference can

be displayed in either points or as a percentage. The Momentum indicator displays

the same information, but expresses it as a ratio.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Relative Volatility Index Backtest The RVI is a modified form of the relative strength index (RSI).

The original RSI calculation separates one-day net changes into

positive closes and negative closes, then smoothes the data and

normalizes the ratio on a scale of zero to 100 as the basis for the

formula. The RVI uses the same basic formula but substitutes the

10-day standard deviation of the closing prices for either the up

close or the down close. The goal is to create an indicator that

measures the general direction of volatility. The volatility is

being measured by the 10-days standard deviation of the closing prices.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Relative Momentum Index Backtest The Relative Momentum Index (RMI) was developed by Roger Altman. Impressed

with the Relative Strength Index's sensitivity to the number of look-back

periods, yet frustrated with it's inconsistent oscillation between defined

overbought and oversold levels, Mr. Altman added a momentum component to the RSI.

As mentioned, the RMI is a variation of the RSI indicator. Instead of counting

up and down days from close to close as the RSI does, the RMI counts up and down

days from the close relative to the close x-days ago where x is not necessarily

1 as required by the RSI). So as the name of the indicator reflects, "momentum" is

substituted for "strength".

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Range Action Verification Index (RAVI) Backtest The indicator represents the relative convergence/divergence of the moving

averages of the financial asset, increased a hundred times. It is based on

a different principle than the ADX. Chande suggests a 13-week SMA as the

basis for the indicator. It represents the quarterly (3 months = 65 working days)

sentiments of the market participants concerning prices. The short moving average

comprises 10% of the one and is rounded to seven.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Positive Volume Index Backtest The theory behind the indexes is as follows: On days of increasing volume,

you can expect prices to increase, and on days of decreasing volume, you can

expect prices to decrease. This goes with the idea of the market being in-gear

and out-of-gear. Both PVI and NVI work in similar fashions: Both are a running

cumulative of values, which means you either keep adding or subtracting price

rate of change each day to the previous day`s sum. In the case of PVI, if today`s

volume is less than yesterday`s, don`t add anything; if today`s volume is greater,

then add today`s price rate of change. For NVI, add today`s price rate of change

only if today`s volume is less than yesterday`s.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Simply Stochastic Backtest This back testing strategy generates a long trade at the Open of the following

bar when the %K line crosses up UpBand line.

It generates a short trade at the Open of the following bar when the %K line

crosses down DownBand line.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

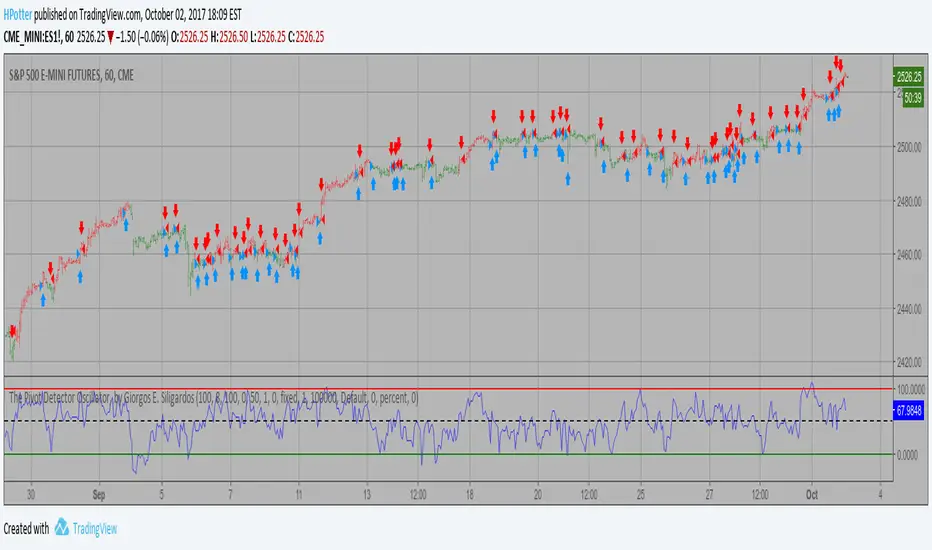

The Pivot Detector Oscillator Backtest The Pivot Detector Oscillator, by Giorgos E. Siligardos

The related article is copyrighted material from Stocks & Commodities 2009 Sep

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

PFE (Polarized Fractal Efficiency) Backtest The Polarized Fractal Efficiency (PFE) indicator measures the efficiency

of price movements by drawing on concepts from fractal geometry and chaos

theory. The more linear and efficient the price movement, the shorter the

distance the prices must travel between two points and thus the more efficient

the price movement.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Percentage Volume Oscillator (PVO) Backtest The Percentage Volume Oscillator (PVO) is a momentum oscillator for volume.

PVO measures the difference between two volume-based moving averages as a

percentage of the larger moving average. As with MACD and the Percentage Price

Oscillator (PPO), it is shown with a signal line, a histogram and a centerline.

PVO is positive when the shorter volume EMA is above the longer volume EMA and

negative when the shorter volume EMA is below. This indicator can be used to define

the ups and downs for volume, which can then be use to confirm or refute other signals.

Typically, a breakout or support break is validated when PVO is rising or positive.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Overbought/Oversold Simple Overbought/Oversold indicator

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

MovROC (KST indicator) Backtes This indicator really is the KST indicator presented by Martin Pring.

the KST indicator is a weighted summed rate of change oscillator that

is designed to identify meaningful turns. Various smoothed rate of change

indicators can be combined to form different measurements of cycles.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Money Flow Indicator (Chaikin Oscillator) Indicator plots Money Flow Indicator (Chaikin). This indicator looks

to improve on Larry William's Accumulation Distribution formula that

compared the closing price with the opening price. In the early 1970's,

opening prices for stocks stopped being transmitted by the exchanges.

This made it difficult to calculate Williams' formula. The Chaikin

Oscillator uses the average price of the bar calculated as follows

(High + Low) /2 instead of the Open.

The indicator subtracts a 10 period exponential moving average of the

AccumDist function from a 3 period exponential moving average of the

AccumDist function.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

MASS Index Backtest The Mass Index was designed to identify trend reversals by measuring

the narrowing and widening of the range between the high and low prices.

As this range widens, the Mass Index increases; as the range narrows

the Mass Index decreases.

The Mass Index was developed by Donald Dorsey.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

MACD Crossover Backtest MACD – Moving Average Convergence Divergence. The MACD is calculated

by subtracting a 26-day moving average of a security's price from a

12-day moving average of its price. The result is an indicator that

oscillates above and below zero. When the MACD is above zero, it means

the 12-day moving average is higher than the 26-day moving average.

This is bullish as it shows that current expectations (i.e., the 12-day

moving average) are more bullish than previous expectations (i.e., the

26-day average). This implies a bullish, or upward, shift in the supply/demand

lines. When the MACD falls below zero, it means that the 12-day moving average

is less than the 26-day moving average, implying a bearish shift in the

supply/demand lines.

A 9-day moving average of the MACD (not of the security's price) is usually

plotted on top of the MACD indicator. This line is referred to as the "signal"

line. The signal line anticipates the convergence of the two moving averages

(i.e., the movement of the MACD toward the zero line).

Let's consider the rational behind this technique. The MACD is the difference

between two moving averages of price. When the shorter-term moving average rises

above the longer-term moving average (i.e., the MACD rises above zero), it means

that investor expectations are becoming more bullish (i.e., there has been an

upward shift in the supply/demand lines). By plotting a 9-day moving average of

the MACD, we can see the changing of expectations (i.e., the shifting of the

supply/demand lines) as they occur.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Laguerre-based RSI Backtest This is RSI indicator which is more sesitive to price changes.

It is based upon a modern math tool - Laguerre transform filter.

With help of Laguerre filter one becomes able to create superior

indicators using very short data lengths as well. The use of shorter

data lengths means you can make the indicators more responsive to

changes in the price.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Klinger Volume Oscillator (KVO) Backtest The Klinger Oscillator (KO) was developed by Stephen J. Klinger. Learning

from prior research on volume by such well-known technicians as Joseph Granville,

Larry Williams, and Marc Chaikin, Mr. Klinger set out to develop a volume-based

indicator to help in both short- and long-term analysis.

The KO was developed with two seemingly opposite goals in mind: to be sensitive

enough to signal short-term tops and bottoms, yet accurate enough to reflect the

long-term flow of money into and out of a security.

The KO is based on the following tenets:

Price range (i.e. High - Low) is a measure of movement and volume is the force behind

the movement. The sum of High + Low + Close defines a trend. Accumulation occurs when

today's sum is greater than the previous day's. Conversely, distribution occurs when

today's sum is less than the previous day's. When the sums are equal, the existing trend

is maintained.

Volume produces continuous intra-day changes in price reflecting buying and selling pressure.

The KO quantifies the difference between the number of shares being accumulated and distributed

each day as "volume force". A strong, rising volume force should accompany an uptrend and then

gradually contract over time during the latter stages of the uptrend and the early stages of

the following downtrend. This should be followed by a rising volume force reflecting some

accumulation before a bottom develops.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading.

Kaufman Moving Average Adaptive (KAMA) Backtest Everyone wants a short-term, fast trading trend that works without large

losses. That combination does not exist. But it is possible to have fast

trading trends in which one must get in or out of the market quickly, but

these have the distinct disadvantage of being whipsawed by market noise

when the market is volatile in a sideways trending market. During these

periods, the trader is jumping in and out of positions with no profit-making

trend in sight. In an attempt to overcome the problem of noise and still be

able to get closer to the actual change of the trend, Kaufman developed an

indicator that adapts to market movement. This indicator, an adaptive moving

average (AMA), moves very slowly when markets are moving sideways but moves

swiftly when the markets also move swiftly, change directions or break out of

a trading range.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Volatility Finite Volume Elements Strategy The FVE is a pure volume indicator. Unlike most of the other indicators

(except OBV), price change doesn?t come into the equation for the FVE

(price is not multiplied by volume), but is only used to determine whether

money is flowing in or out of the stock. This is contrary to the current trend

in the design of modern money flow indicators. The author decided against a

price-volume indicator for the following reasons:

- A pure volume indicator has more power to contradict.

- The number of buyers or sellers (which is assessed by volume) will be the same,

regardless of the price fluctuation.

- Price-volume indicators tend to spike excessively at breakouts or breakdowns.

This study is an addition to FVE indicator. Indicator plots different-coloured volume

bars depending on volatility.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not

Volatility Finite Volume Elements Backtest This version has an important enhancement to the previous one that`s

especially useful with intraday minute charts.

Due to the volatility had not been taken into account to avoid the extra

complication in the formula, the previous formula has some drawbacks:

The main drawback is that the constant cutoff coefficient will overestimate

price changes in minute charts and underestimate corresponding changes in

weekly or monthly charts.

And now the indicator uses adaptive cutoff coefficient which will adjust to

all time frames automatically.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.