Customizable Non-Repainting HTF MACD MFI Scalper Bot StrategyThis script was originally shared by Wunderbit as a free open source script for the community to work with.

WHAT THIS SCRIPT DOES:

It is intended for use on an algorithmic bot trading platform but can be used for scalping and manual trading.

This strategy is based on the trend-following momentum indicator . It includes the Money Flow index as an additional point for entry.

HOW IT DOES IT:

It uses a combination of MACD and MFI indicators to create entry signals. Parameters for each indicator have been surfaced for user configurability.

Take profits are fixed, but stop loss uses ATR configuration to minimize losses and close profitably.

HOW IS MY VERSION ORIGINAL:

I started trying to deploy this script myself in my algorithmic trading but ran into some issues which I have tried to address in this version.

Delayed Signals : The script has been refactored to use a time frame drop down. The higher time frame can be run on a faster chart (recommended on one minute chart for fastest signal confirmation and relay to algotrading platform.)

Repainting Issues : All indicators have been recoded to use the security function that checks to see if the current calculation is in realtime, if it is, then it uses the previous bar for calculation. If you are still experiencing repainting issues based on intended (or non intended use), please provide a report with screenshot and explanation so I can try to address.

Filtering : I have added to additional filters an ABOVE EMA Filter and a BELOW RSI Filter (both can be turned on and off)

Customizable Long and Close Messages : This allows someone to use the script for algorithmic trading without having to alter code. It also means you can use one indicator for all of your different alterts required for your bots.

HOW TO USE IT:

It is intended to be used in the 5-30 minute time frames, but you might be able to get a good configuration for higher time frames. I welcome feedback from other users on what they have found.

Find a pair with high volatility (example KUCOIN:ETH3LUSDT ) - I have found it works particularly well with 3L and 3S tokens for crypto. although it the limitation is that confrigurations I have found to work typically have low R/R ratio, but very high win rate and profit factor.

Ideally set one minute chart for bots, but you can use other charts for manual trading. The signal will be delayed by one bar but I have found configurations that still test well.

Select a time frame in configuration for your indicator calculations.

Select the strategy config for time frame. I like to use 5 and 15 minutes for scalping scenarios, but I am interested in hearing back from other community memebers.

Optimize your indicator without filters (trendFilter and RSI Filter)

Use the TrendFilter and RSI Filter to further refine your signals for entry. You will get less entries but you can increase your win ratio.

I will add screenshots and possibly a video provided that it passes community standards.

Limitations: this works rather well for short term, and does some good forward testing but back testing large data sets is a problem when switching from very small time frame to large time frame. For instance, finding a configuration that works on a one minute chart but then changing to a 1 hour chart means you lose some of your intra bar calclulations. There are some new features in pine script which might be able to address, this, but I have not had a chance to work on that issue.

真實波幅均值(ATR)

Supertrend with TP by Furkan SancuSimple Supertrend strategy with Take Profit levels.

Note: Make sure TP amounts add up to 100.

Opens a position with Supertrends strategy then adds Take Profit points with certain amounts of current position.

Long Term Heat/Volatility - Accumulation/Distribution v1This is a strategy specifically made for 1D BTC/USD with the aim of capturing cycle tops and bottoms. It's mainly based on two indicators: 21d average of ATR (volatility) and (BTC.price - 180d sma)/BTC.price (heat). The strategy only signals buys or sells after occurrences of high volatility, followed by extremely high or low heat values. It's optimized for utilizing accumulation and distribution at lower and higher prices respectively with respect to last 14 days. 2nd version will include dynamic dollar cost averaging during the accumulation and distribution periods.

Chandelier Exit - StrategyI created a strategy version for the Chandelier Exit indicator, originally owned by @everget . With the strategy I prepared, you can try both short-long and stop loss - trailing stop and take profit rates. I have also added a date filter feature so that you can test the strategy in the date range you want.

Orjinali @everget 'e ait olan Chandelier Exit indicator için strateji versiyonu oluşturdum. Hazırladığım strateji ile hem short-long deneyebilir hem de zarar durdur - takip eden stop ve kar al oranları denemeleri yapabilirsiniz. İstediğiniz tarih aralığında strateji testi yapabilmeniz için tarih filtre özelliği de ekledim.

Hourly Bias on BTC in Bullish USA Session “Green Eagle”Name: Hourly Bias on BTC in Bullish USA Session

Category: Hourly Bias

Operating mode: Spot, only long

Trades duration: Intraday, 11 bars

Timeframe: 1H

Suggested usage: When the market is compressed, USA session has a bullish bias.

Entry: enter Long at 15:00 on specific days of the week. There is a volatility filter based on ATR which identifies compression.

Exit: exit at a pre-defined time at 01:00

Usage:

⁃ It can be useful to use alerts or webhooks to automate this strategy.

⁃ This is a core system that can be improved in different ways (e.g. Stop-loss, take-profit, position sizing) or studying more the behaviour in the specific days of the week or short when is red.

Configuration:

- N/A

Backtesting

⁃ Exchange: BINANCE

⁃ Pair: BTCUSDT

⁃ Timeframe: 1H

⁃ Fee 0.075%

⁃ Slippage 2

- Start : 2019-01-06

We decided to release this free BTC strategy.

How you or we can improve? Source code is open so share your ideas!

Configurable Multi MA Crossover Voting SystemThis strategy goes long when all fast moving averages that you have defined are above their counterpart slow moving averages.

Long position is closed when profit or loss target is hit and at least one of the fast moving averages is below its counterpart slow moving average.

The format of the config is simple. The format is : FASTxSLOW,FASTxSLOW,...

Example : If you want 2 moving averages fast=9,slow=14 and fast=20,slow=50 you define it like this : 9x14,20x50

Another example : 5x10,10x15,15x20 => means 3 moving average setups : first wih fast=5/slow=10, second with fast=10/slow=15, last with fast=15/slow=20

You can chose the type of moving average : SMA, WMA, VWMA (i got issues with EMA/RMA so i removed them)

You can chose the source of the moving average : high, close, hl2 etc.

You can chose the period on which ATR is calculated and ATR profit/loss factors.

Profit is calculated like : buy_price + atr_factor*atr

Loss is calculated like : buy_price - atr_factor*atr

Performance in backtest is variable depending on the timeframe, the options and the market.

Performance in backtest suggests it works better for higher timeframes like 1d, 4h etc.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

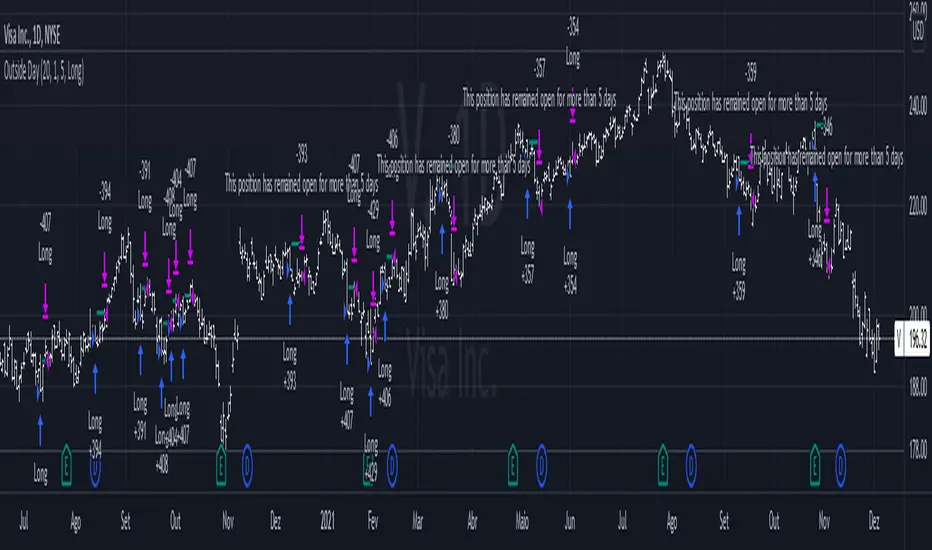

Outside DayThis strategy is taken from Perry Kaufman's book "Trading System and Methods".

You can enter on the direction of the candle, or opposite to it. I find that the opposite tends to yield better results in volatile assets, allowing a better reward to risk ratio. There is no stop loss in this strategy, only a fixed take profit and a time limitation.

Hull MA TimeFrame CrossOverHello traders,

Although this strategy is configured on BTCUSDT , with a changing of settings, it can be used on any trading instrument.

Here it is seen, on the 2 hour chart. With Trading Fees included in result (adjust to suit your exchange fees).

The candle crossover is set to Daily timeframe.

That means that the Candle crossover is going to see if todays price is higher than yesterdays price.

If user sets this to 4 hour timeframe, the candle crossover would be when price is higher than the the price 4 hours ago...

The rest is simple, a moving average to detect direction, and an ATR StopLoss (if activated).

There is StopLoss and Take Profit settings which work by percentage.

The periods of the moving average and the ATR can be adjusted, as can the TP % and SL %.

The price is taken from the CLOSE or the OPEN or OHLC4 etc... which can be changed in the settings. OPEN is recommended to avoid repainting.

The moving average also has selectable types (ALMA,SMA,EMA,WMA,HMA)

So if the Price is above the Moving average, and the moving average is above the alternate timeframe value, then a buy is activated

if the Price is below the Moving average, and the moving average is below the alternate timeframe value, then a sell is activated

if OPEN is selected as Price source, then the alternate timeframe value would be the OPEN of the alternate timeframes candle.

the values are all plotted on chart so user can see what is happening when what crosses over what, and then what changes when settings are adjusted.

Have FuN!

if this strategy brings you the epik win......

.... dont forget about me

seaside420 ❤️

Double SupertrendThis strategy is based on a custom indicator that was created based on the Supertrend indicator. At its core, there are always 2 super trend indicators with different factors to reduce market noise (false signals).

The strategy/indicator has some parameters to improve the signals and filters.

TECHNICAL ANALYSIS

☑ Show Indicators

This option will enable/disable the Supertrend indicators on the chart.

☑ Length

The length will be used on the Supertrend Indicator to calculate its values.

☑ Dev Fast

The fast deviation or factor from one of the super trend indicators. This will be the leading indicator for entry signals, as well as for the exit signals.

☑ Dev Slow

The slow deviation or factor from one of the super trend indicators. This will be the confirmation indicator for entry and exit signals.

☑ Exit Type

It's possible to select from 4 options for the exit signals. Exit signals always take profit target.

☑ ⥹ Reversals

This option will make the strategy/indicator calculate the exit signals based on the difference between the given period's highest and lowest candle value (see Period on this list). It's displayed on the chart with the cross. As it's possible to verify in the image below, there are multiple exit spots for every entry.

☑ ⥹ ATR

Using ATR as a base indicator for exit signals will make the strategy/indicator place limit/stop orders. Candle High + ATR for longs, Candle Low - ATR for shorts. The strategy will show the ATR level for take profit and stick with it until the next signal. This way, the take profit value remains based on the candle of the entry signal.

☑ ⥹ Fast Supertrend

With this option selected, the exit signals will be based on the Fast Supertsignal value, mirrored to make a profit.

☑ ⥹ Slow Supertrend

With this option selected, the exit signals will be based on the Slow Supertsignal value, which is mirrored to take profit.

☑ Period

This will represent the number of candles used on the exit signals when Reversals is selected as Exit Type. It's also used to calculate the gradient used on the Fills and Supertrend signals.

☑ Multiplier

It's used on the take profit when the ATR option is selected on the Exit Type.

STRATEGY

☑ Use The Strategy

This will enable/disable the strategy to show the trades calculations.

☑ Show Use Long/Short Entries

Option to make the strategy show/use Long or Short signals. Available only if Use The Strategy is enabled

☑ Show Use Exit Long/Short

Option to make the strategy show/use Exit Long or Short signals (valid when Reversals option is selected on the Exit Type). Available only if Use The Strategy is enabled

☑ Show Use Add Long/Short

Option to make the strategy show/use Add Long or Short signals. With this option enabled, the strategy will place multiple trades in the same direction, almost the same concept as a pyramiding parameter. It's based on the Fast Supersignal when the candle fails to cross and reverses. Available only if Use The Strategy is enabled

☑ Trades Date Start/End

The date range that the strategy will check the market data and make the trades

HOW TO USE

It's very straightforward. A long signal will appear as a green arrow with a text Long below it. A short signal will appear as a red arrow with a text Short above it. It's ideal to wait for the candle to finish to validate the signal.

The exit signals are optional but give a good idea of the configuration used when backtesting. Each market and timeframe will have its own configuration for the best results. On average, sticking to ATR as an exit signal will have less risk than the other options.

☑ Entry Signals

Follow the arrows with Long/Short texts on them. Wait for the signal candle to close to validate the entry.

☑ Exit Signals

Use them to close your position or to trail stop your orders and maximize profits. Select the exit type suitable for each timeframe and market

☑ Add Entries

It's possible to increase the position following the add margin/contracts based on the Add signals. Not mandatory, but may work as reentries or late entries using the same signal.

☑ What about Stop Loss?

The stop-loss levels were not included as a separated signal because it's already in the chart. There are some possible ideas for the stop loss:

☑⥹ Candle High/Low (2nd recommend option)

When it's a Long signal from the entry signal candle, the stop loss can be the Low value of the same candle. Very tight stop loss in some cases, depending on the candle range

☑⥹ Local Top/Bottom

Selecting the local top/bottom as stop loss will give the strategy more room for false breakouts or reversals, keeping the trade open and minimizing noises. Increases the risk

☑⥹ Fast Supertrend (1st recommend option)

The fast supertrend can be used as stop-loss as well. making it a moving level and working close to trail stop management

☑⥹ Fixed Percentage

It's possible to use a fixed risk percentage for the trades, making the risk easier to control and project. Since the market volatility is not fixed, this may affect the accuracy of the trades

☑⥹ Based on the ATR (3rd recommend option)

When the exit type option ATR is selected, it will display the take profit level for that entry. Just mirror that value and put it as stop-loss, or multiply that amount by 1.5 to have more room for market noise.

EXAMPLE CONFIGURATIONS

Here are some configuration ideas for some markets (all of them are from crypto, especially futures markets)

BTCUSDT 15min - Default configuration

BTCUSDT 1h - Length 10 | Dev Fast 3 | Dev Slow 4 | Exit Type ATR | Period 50 | Multiplier 1

BTCUSDT 4h - Length 10 | Dev Fast 2 | Dev Slow 4 | Exit Type ATR | Period 50 | Multiplier 1

ETHUSDT 15min - Length 20 | Dev Fast 1 | Dev Slow 3 | Exit Type Fast Supertrend | Period 50 | Multiplier 1

IOTAUSDT 15min - Length 10 | Dev Fast 1 | Dev Slow 2 | Exit Type Slow Supertrend | Period 50 | Multiplier 1

OMGUSDT 15min - Length 10 | Dev Fast 1 | Dev Slow 4 | Exit Type Slow Supertrend | Period 50 | Multiplier 1

VETUSDT 15min - Length 10 | Dev Fast 3 | Dev Slow 4 | Exit Type Slow Supertrend | Period 50 | Multiplier 1

HOW TO FIND OTHER CONFIGURATIONS

Here are some steps to find suitable configurations

select a market and time frame

enable the Use This Strategy option on the strategy

open the strategy tester panel and select the performance summary

open the strategy configuration and go to properties

change the balance to the same price of the symbol (example: BTCUSDT 60.000, use 60.000 as balance)

go back to the inputs tab and keep changing the parameters until you see the net profit be positive and bigger than the absolute value of the drawdown

in case you can't find a suitable configuration, try other timeframes

Since the tester reflects what happened in the past candles, it's not guaranteed to give the same results. However, this indicator/Strategy can be used with other indicators as a leading signal or confirmation signal.

Fractal Breakout Strategy [KL]Fractal Breakout Strategy

This strategy will enter into a Long position when (a) bullish fractal is formed, combined with (b) ATR is relatively low. Trailing stop loss is set based on ATR.

Bullish fractal pattern :

A bullish fractal pattern looks like this:

It is formed when lower-low has reached a local minimum followed by higher-lows.

By default, this script plots the pivot point (the local minimum) using green crosses. This line will extend to the right until the next bullish fractal is formed. The local minimum pivot point is considered as key level of support. For long position entry, entry price must be higher or equal to it.

On the other hand, a bearish fractal pattern looks like the exact opposite. Reversing the logic, it is a local maximum indicated by higher-highs followed by lower-highs. This is shown by red crosses.

Why use ATR to confirm entry :

Two reasons to enter when ATR is low:

1) Since trailing stop loss is based on ATR, entering the market when ATR is low means risking less for potentially high reward.

2) Low ATR often signals price consolidation. There are two favorable scenarios, either: (i) period of accumulation, or (ii) bull flag, ideally followed by breakout.

Determining whether ATR is low :

Relative lows are quantified out by using the method in my other script: Modified ATR Indicator

The method involves applying two-tailed hypothesis testing to assess whether ATR (ie. by default lookback period of 5) has greatly deviated from a larger sample size (ie. lookback period of 50). Assuming ATR is normally distributed and variance is known, then test statistic (z) can be used to determine whether ATR5 is within the critical area under Null Hypothesis: ATR5 == ATR50. If z falls below/above the left/right critical values (ie. 1.645 for a 90% confidence interval), then ATR is determined to the relatively low/high respectively. For the purpose of assessing whether ATR is low, the left-tail is the main focus.

Profit taking :

Profits by default are taken over 3 levels based on risk to reward ratio (ie. 1R, 2R, 3R). When a target is met at each level, strategy will close out one third of current position size. Remainders (ie. already taken once at 1R, but not yet reaching 2R or 3R) will eventually be closed at the trailing stop loss price.

UT Bot v5This is an update by request, on someone elses strategy! well more of an edit, but also update from pine v4 to pine v5.

//CREDITS to HPotter for the orginal code. The guy trying to sell this as his own is a scammer lol.

//Edited and converted to @version=5 by SeaSide420 for Paperina

The UT Bot v5 is Movinging average (the MA) vs ATR (the ATR is in the form intended for use as trailing stop loss (ATR_TSL))

Entry logic:

buy = the MA > ATR_TSL and Price > ATR_TSL

sell = the MA < ATR_TSL and Price < ATR_TSL

The Moving average type can be changed in the settings:

options = "SMA", "EMA", "WMA", "HMA"]

the edits i made were:

convert to v5

Add TP and SL

Add Buy only or Sell only option

Add MA type option

Add price source option

Draw MA and ATR_TSL on-chart

Mean Reversion Strategy v2 [KL]Description :

This strategy will enter a position when the following conditions are met:

a) Main signal: When source data (ATR) diverts from its moving average value, and

b) Confirmation: If predicted direction of trend is favorable.

Assumptions :

During periods of high price volatility, ATR diverts from its moving average value. Eventually, ATR should revert. But since just knowing the magnitude of increase/decrease of ATR does not indicate a trend signal, we need to introduce a model to predict the current trend.

In short:

• Trend Prediction : This strategy calculates the expected logarithmic return of the security (the "Drift") and considers prices to be moving in uptrend if the drift curve is upward sloping.

• Assessment of ATR diversion : To determine "yes/no" regarding whether ATR at a given point in time has diverted, this script conducts a two-tailed hypothesis test at each candlestick period. The null hypothesis (H0) is that the fast moving average value should equal the slow moving average value (say, denoted as H0: atr14 == atr28; it is assumed that atr28 is more meaningful for the purpose of describing the current trend because it has a larger sample size). Investopedia has an article summarizing this topic .

Exit Condition :

When trailing stop loss hits.

Previous version :

This strategy is based on Version 1 published back in September . This older version considers +/- one standard deviation to be the critical values relative to average ATR when testing whether ATR has diverted from the mean. This does not take Standard Error ("SE") into account. As a result, the threshold is often too wide and it generates too many entry signals.

Trend Strategy by zdmreThis Strategy is a trend following indicator. It is plotted on price and the current trend can be determined by its placement vis-a-vis price. It is constructed with just three parameters: Period, Multiplier and Entry/Exit Point with Superformula.

The default parameters are 14 for Average True Range (ATR) and 4 for its multiplier. The average true range (ATR) plays a key role in ‘Trend’ as the indicator uses ATR to compute its value and it signals the degree of price volatility. You should note that any changes to these numbers can affect the use of the Trend indicator.

While you using this indicator, you should not avoid putting your stop loss.

For a long position, you can put stop loss right at the red indicator line. For a short position, you can put it at the green indicator line. You can insert your own settings as well.

Using Trend Strategy along with a stop loss pattern is the best way for earning the best wealth in trading.

There is no best setting for any trading indicator.

Kaufman's Efficiency Ratio Strategy [KL]I recently published an indicator called "Kaufman's Efficiency Ratio Indicator". In the description of that script, I hypothesized about how the Efficiency Ratio could be applied to identify bullish moves in instances where price had already gone up steeply, but rests for a while, allowing for entry in expectation that price will continually rise. I decided to test out this idea with Pinescript.

About Kaufman's Efficiency Ratio ("ER")

ER was developed by a systematic trader by the name of Perry J. Kaufman.

Formula

The formula is:

= A divided by B,

where:

A = Current closing price minus the closing price at the start of the lookback period

B = Sum of differences between closing prices (in absolute terms) of consecutive bars over the lookback period

How this strategy enters a trade (Long):

- code: entry_signal_long = ER > 0 and ER_is_mid

- meaning: when ER is positive, strategy assumes price has risen. Usually ER value begins high (red), and unless it is a false move, then it should stay positive. This strategy will patiently wait until ER drops to medium (yellow), and then place a trade.

- how low/medium/high is dynamically determined: Refer to the description of my other script("Kaufman's Efficiency Ratio Indicator") for details. Trying to keep this as short as possible.

How this strategy exits a trade (Long):

- when price hits stop limit; stop limit is based on low of bars, trails upward based on ATR

- included a feature called "tightening TSL", which tries to reduce the stop-buffer during periods of high volatility implied by ER (very experimental, opening the floor for suggestions on how this can be improved)

%-[Guz] Vortex Indicator Custom// Custom Vortex Strategy (backtester)

// Custom version of the Vortex indicators that adds many features:

// -Triggers trades after a threshold is reached instead of the normal vortex lines cross (once the difference between the 2 lines is important enough)

// -Smooths the Vortex lines with an EMA

// -Adds Take Profit and Stop Loss selection

// -Adds the possibility to go Long only, Short only or both of them

// ! notice that it uses 10% position size and 0.04% trade fee, found on some crypto exchanges futures contracts

// Allows testing leverage with position size modification (values above 100% position size, to be done with caution)

// Not an investment advice

[KL] Mean Reversion (ATR) StrategyThis strategy will enter into a position when price volatility is relative high, betting that price will subsequently trend in a favourable direction.

Hypothesis : During periods of high price volatility, ATR will divert from its moving average by at least +/- one standard deviation. Eventually, ATR will revert back to the mean. However, just knowing the magnitude of increase/decrease of ATR does not give a trend signal, so we need to introduce a model in this script to predict whether the next bars will be up/down.

Trend Prediction : This strategy calculates the expected logarithmic return of the security (the "Drift") and considers prices to be moving in uptrend if the drift curve is upward sloping or if the drift value is positive.

Entry Conditions : Long position is entered when:

(a) ATR has diverted from mean by one standard deviation, and

(b) trend is predicted to move in our favor.

Exit Condition : When trailing stop loss is hit.

Results from backtesting against VOO (1H timeframe):

- approx 46% win rate over 491 trades, on average holding for 20 hours per trade

- price at the beginning of backtest (Jan. 2015) was $187.52, giving holding period return of ~120% had we not sold in between ("HPR of HODL'ing")

- this strategy gained ~159%, exceeding ~120% HPR of HODL'ing

Strategy Template - V2This is an educational script created to demonstrate few basic building blocks of a trend based strategy and how to achieve different entry and exit types. My initial intention was to create a comprehensive strategy template which covers all the aspects of strategy. But, ended up creating fully fledged strategy based on trend following.

This is an enhancement on Strategy-Template But this script is comparitively more complex. Hence I decided to create new version instead of updating the existing one.

Lets dive deep.

SIMPLE COMPONENTS OF TREND FOLLOWING STRATEGY

TREND BIAS - This defines the direction of trend. Idea is not to trade against the trend direction. If the bias is bullish, look for long opportunities and if bias is bearish, look for short opportunities. Stay out of the market when the bias is neutral.

Often, trend bias is determined based on longer timeframe conditions. Example - 200 Moving Average, Higher timeframe moving averages, Higher timeframe high-lows etc. can be used for determining the trend bias.

In this script, I am using Weekly donchian channels combined with daily donchian channels to define trend bias.

Long Bias - 40 Day donchian channel sits completely in upper portion of 40 Week dochnial channel.

Short Bias - 40 Day donchian channel sits completely in lower portion of 40 Week donchian channel.

ENTRY CONDITION - Entry signals are generated only in the direction of bias. Hence, when in LongBias, we only get Long signals and when in short bias, we only get short signals.

In our case, when in Long Bias - if price hits 40 day high for the first time, this creates our long entry signal. Similarly when in Short Bias , price hitting 40 day low will create signal for going short. Since we do not take trades opposite to trend, no entry conditions are formed when price hits 40 day high in Short Bias or 40 day low in Long Bias.

EXIT CONDITION - Exit conditions are formed when we get signals of trend failure.

In our case, when in long trade, price hitting 40 day low creates exit signal. Similarly when in short trade price hitting 40 day high creates exit signal for short trade.

DIFFERENT TYPES OF ENTRY AND EXIT

In this script, I have tried to demonstrate different entry and exit types.

Entry types

Market - Enter immediately when entry signal is received. That is, in this case when price crossover over high in long bias and crosses under low in short bias

Stop - This method includes estimating at what level new highs are made and creating a stop buy order at that level. This way, we do not miss if the break out is stronger. But, susciptible to fail during fakeouts.

Limit - This method includes executing a limit order to buy at lower price or sell at higher price. In trend following methods, downside of limit order is when there is genuine breakout, these limit orders may not hit and during trend failures the limit orders are likely to hit and go straight to stop.

Stop-Limit - this is same as stop order but will also place a limit condition to avoid buying on overextended breakout or with lots of slippage.

Exit types

Market - whether to keep the existing trade running or whether to close it is determined after close of each bar and exit orders are executed manually upon receiving exit signal.

Stop - We place stop loss orders beforehand when there is a trade in place. This can help in avoiding big movements against trade within bar. But, this may also stop on false signals or fakeouts.

Take profit

Stop - No take profits are configured.

Target - 30% of the positions are closed when take profit levels are hit. Take profit levels are defined by risk reward.

USING THE CODE AS TEMPLATE

As mentioned earlier, I intended to create a fully fledged strategy template. But, ended up creating a fully fledged stratgy. However, you can take some part of this code and use it to start your own strategy. Will explain what all things can be adopted without worrying about the strategy implementation within

Strategy definition : This can be copied as is and just change the title of strategy. This defines some of the commonly used parameters of strategy which can help with close to realistic backtesting results for your coded strategy and comparison with buy and hold.

Generic Strategy Parameters : The parameter which defines controlling alllowed trade direction and trading window are present here. This again can be copied as is and variable inDateRange can be directly used in entry conditions.

Generic Methods : f_getMovingAverage and f_secureSecurity are handy and can be used as is. atr method provideded by pine gives you ATR based on RMA. If you want SMA or any other moving average based ATR, you can use the method f_getCustomAtr

Trade Statements : This section has all types of trading instructions which includes market/stop/limit/stop-limit type of entries and exits and take profit statements. You can adopt the type of entry you are interested in and change when condition to suit your strategy.

Trade conditions and levels : This section is required. But, cannot be copied. All the trade logic goes here which also sets parameters which are used in when of Trade Statements.

Hope this helps.

[KL] Relative Volume + ATR StrategyThis strategy will enter into long position when (a) current volume is above the average volume, and when (b) volatility of prices (based on ATR) is relatively low.

Backtested on hourly timeframes, win rates range between 35% to 50% on stocks with positive drifts (i.e. tendency to move upwards). Default setups are as follows:

- Average volume is computed using simple moving average (sma) of 14 periods. By default, 1.4x ratio seems to work well on most large cap stocks. If it's too high, then amount of potential points for entry will decrease. But if it's too low, then this indicator becomes meaningless.

- ATR (for determining volatility), look back period is 14 (following conventions). I have noticed that the profits could change drastically when changed to different values for each individually security. Feel free to experiment around with this parameter.

Other information: This strategy is based off of one of my previous scripts; a script called "Relatively Volume Strategy". The objective of this new script is to simplify the process of determining periods of low volatility. In this new script, we assume prices are consolidating when current ATR is within its moving average value by +/- one standard deviation.

Av3Based on the ANNE EA v3 for MT4. For use on FOREX.

if ATR is greater than ATR average taken from last 5 candles, then market considered as trending, and so Open(0)>Close(1)=buy Open(0)Close(1)=sell Open(0)

Strategy TemplateTrying to include few basic things which is needed for strategy which can be used as template.

Few important components

Strategy parameters

Few important parameters include - initial_capital, default_qty_type, default_qty_value, commission_type, pyramiding and commission_value. All my strategies will have similar settings with initial captial set to 20000 to 100000. 100% of equity per trade with no pyramiding (set to 1) and minimal commission.

margin_long and margin_short can be used for leveraged trading. But, since we are not using pyramiding, it will make no effect.

Trade Limiting parameters

Two types of limiting is available in the scripts

Limiting trading direction : this is done through method strategy.risk.allow_entry_in and input parameter tradeDirection

Limiting trades to particular time window : This is achieved through adding start time and end time parameters of type input.time and check whether time is within this window

Custom Methods

customized security method to get higher timeframe data

customized moving average method to get moving average of any type

Custom Parameters

Moving average Type option list which I use quite often. Any strategy where there is need to use moving average, I try to scan through different moving average types and lengths to see which one is more appropriate for the given strategy. Hence, keeping this parameter in template to make it readily available when I start with new strategy

waitForCloseBeforeExit - this is used if trailing stop need to activated as soon as price hits the stop or only on close price. This is again something I switch quite often based on strategy. Hence, keeping this as part of the template.

Entry and Exit statements for long and short

These statements from line (57 to 62) can remain as is even with new strategy. Only thing to be set are variables - buyCondition, sellCondition, closeBuyCondition and closeSellCondition

Last but not the least

In pinescript, a long and short position cannot coexist in a strategy at any point of time. Any short positions created will automatically stop long positions and vice versa. Hence, it is important make short and long trades mutually exclusive. In this example, I have used 200 weekly moving average as trend bias. No short positions are taken when price is trading above 200 weekly moving average low/close and no long positions are taken when price is less than 200 weekly moving average high/close. Any rule built on top of this (In this case a simple supertrend rules) ensures that there are no conflicting signals and hence avoids confusing trades on the stratgy.

Kifier's MFI/STOCH Hidden Divergence/Trend BeaterMFI/STOCH Hidden Divergence/Trend Beater

General Idea:

My premise around this strategy was to make a general strategy for crypto that would help out with finding entry positions for when you’re bullish on a crypto and want to hold on for a while, and at the same time avoiding massive drops. Essentially a way to mix long term/ swing trading; I somewhat achieved my goal however it still requires a lot of logic tuning of the trend averages.

I’m a huge proponent of volume indicators and coupled with average closing price, I think this gives a really good idea of what is happening with the market. It gives an idea on the market and retail investor sentiment. This generally gives you logical entry positions (Although I don’t know how amazing that will work with all cryptos, there’s a fine line between a good strategy and one that just rides bubble market conditions, some would argue that’s still a success and others not)

How it works:

There are many components to the strategy that try to do different things:

First of all there are two types of entries, a MFI hidden divergence with a STOCH check, essentially it will only fire when a divergence is detected while STOCH is above 50%, however this might be changed in the future as due to the volatile nature of cryptos, the STOCH is not too effective. The second entry is a simple MFI/STOCH trend, if STOCH is above 50% and the trend is detected to be in a trending long, once a MFI crossover over the 50% line is detected an entry is placed, this is designed to get out profit where the divergence would otherwise be less accurate during strongly trending conditions.

-MFI is a great indicator, as a volume weighted momentum indicator I find it the most accurate of all, the STOCH however is a great indicator to get a general picture of simple market conditions and can filter out the emotional noise of retail investors.

-VWMA and an SMA (The bottom oscillator) gives an idea of the trend tacking into account of the volume, this serves as a more short term filter of the trend for filters.

-OBV checks are done between the OBV and an EMA of the OBV, to get the idea of a volume weighted long trend, which is important for crypto as there are massive rallies to go up due to retail greed, it’s great to jump onto it at the beginning, and get off before the stack of cards fall apart.

-ATR is used to detect when the market is relatively just ranging or moving sideways, which is where the hidden divergence entries are done, during predictable and profitable market conditions.

- Stop loss is based on the closest support of the entry, this is a nice medium of room to breath but also an actual stop loss.

Future plans and improvements:

Currently there’s a lot I want to improve, mostly the divergence detection and the overall sharpe ratio could be much better, but the current value of 0.5 gives me hope that the strategy is onto something. I also want to change TP from a percentage stop to something more dynamic but that might be too optimistic. The current plan is to paper trade test this either by manual or by a python bot, to see how it performs with some user input as well.

Chaikin Money Flow + MACD + ATRHere I present you on of Trade Pro's Trading Idea: Chaikin Money Flow + MACD + ATR.

This strategy is not as profitable as it can be seen in one of his videos. In the forex market, the strategy could reach a maximum of 35% profitability.

I have, as some of my followers have requested, created an overview of the current position, risk and leverage settings in the form of a table.

Furthermore, one can again swap between short and long positions.

It is now possible to select or deselect individual indicators.

I have chosen the ATR alone as a take profit stop loss, as in his strategy.

A position is only triggered as soon as all prerequisites have been fulfilled and a command is executed. This prevents false triggering by bots and repainting.

-----------------------------------------------------------------------------------

How does the strategy work?

ENTRY

Long

The MACD indicator must be above the zero line.

Then the K line must cross the D line.

Finally, when this happens, the Money Flow Index must be above the zero line.

Short

Contrary to the premise of long positions.

EXIT

ATR Exit

The value of ATR at the time of buying is multiplied by the value entered in "Profit factor ATR" and "Stop factor ATR". As soon as the price reaches this value, it is closed.

Important

The script must be optimized for each coin or currency pair.

I will publish a guide to the strategy shortly. There I will explain how the table works and how to set the strategy correctly.

The results of the strategy are without commissions and leverage.

If you have any questions or feedback, please let me know in the comments.

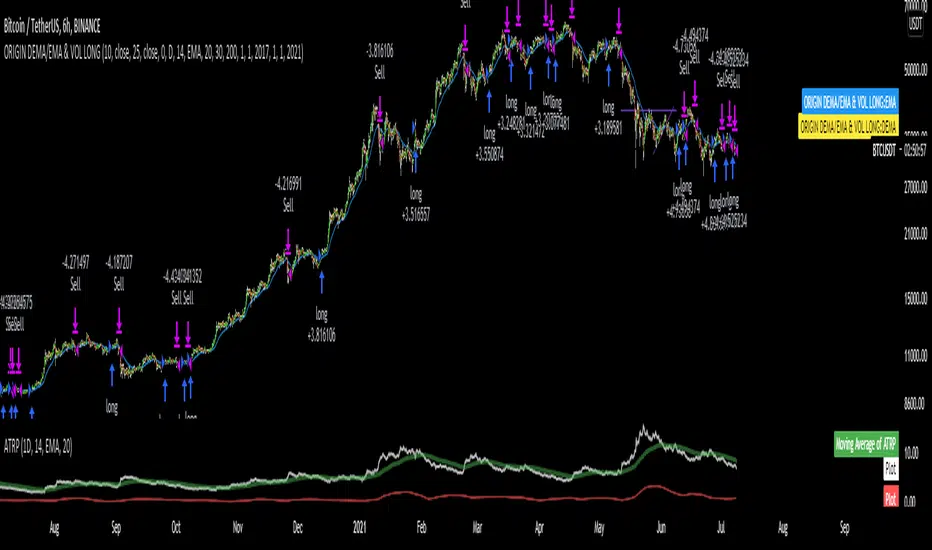

DEMA/EMA & VOLATILITY (VAMS)The biggest issue with momentum following strategies is over signaling during whipsaw periods. I created this strategy that measure momentum with DEMA (Fast Moving) and EMA (Slow moving). In order to mitigate over signaling during whipsaw periods I implemented the average true range percentage (ATRP) to measure realized volatility. If momentum is picking up while volatility is under a certain threshold it purchases the security. If momentum slows while volatility picks up it sells the security. Additionally, if momentum picks up, but volatility is high, it stays out of the security. This follows the theory that during sustained uptrends volatility will decrease, and during market corrections the volatility picks up. Following the old adage that markets climb up the stairs, and fall out the window. Note that this strategy does repaint due to it entering and closing positions at the close of the bars. I forgot to mention how volatility is measured high vs low. If the ATRP is above the EMA of the ATRP the strategy interprets the volatility is increasing and does not enter the security & Vice Versa for selling (with momentum signal of MAs)

This is just my first strategy, any feedback would be much appreciated.